September Property & Finance Newsletter: Understanding the Market, Your Borrowing Power & Smart Loan Choices

A Busy Spring for Borrowers & Buyers

Spring traditionally marks a vibrant season for the property market in Australia, and this year is no exception. While much of the attention has been on the Reserve Bank’s September 30 cash rate call, several other stories are shaping the landscape for borrowers, investors, and homebuyers alike.

From record-high repayment discipline to surging offset savings, continued property price growth, and even Australians’ shifting relationship with credit cards, these trends all feed into one crucial question: how strong is your financial footing in the current market?

Let’s take a closer look at what’s happening and how it may impact your property and finance decisions this season.

Mortgage Repayments: Borrowers Are Paying on Time at Record Levels

Despite cost-of-living pressures, Australian borrowers are demonstrating remarkable resilience. According to the Australian Prudential Regulation Authority (APRA), the share of home loans running 30–89 days late dropped from 0.66% in June 2024 to 0.55% in June 2025.

That means more than 99 out of 100 borrowers are up to date with their repayments, a strong indicator that households are adapting well. Lower interest rates earlier in 2025 have helped ease repayment stress, but equally important is how Australians are budgeting more carefully to stay ahead.

Loan Behaviour Is Shifting

Interestingly, APRA’s data reveals borrowers are adopting two distinct approaches:

- Bigger deposits: In June 2025, 69.6% of new borrowers contributed deposits of at least 20%, compared to 68.1% a year earlier. This shows many households are playing it safe, prioritising equity and minimising risk.

- Higher debt-to-income ratios: On the flip side, 5.5% of borrowers took on loans worth six times or more their annual income, up from 5.0% the year before. This group is maximising borrowing capacity to buy in competitive markets.

This contrast illustrates the two mindsets in today’s lending environment: caution versus ambition.

Takeaway for you: It’s vital to tailor your loan strategy to your circumstances. Whether you prefer the safety of a larger deposit or want to stretch for a bigger property, the key is finding the right balance for your budget and long-term goals.

Offset Accounts: A Growing Tool to Ease Mortgage Pain

Another encouraging trend is that Australians are saving more in offset accounts, reducing the interest they pay on their mortgages.

In the June quarter, borrowers had $11,435 in offset for every $100,000 of loan debt, up from $10,647 a year earlier.

What Is an Offset Account?

An offset account is a bank account linked to your home loan. Every dollar in it directly reduces the loan balance used to calculate interest. For example:

- Home loan: $500,000

- Offset balance: $20,000

- Interest charged on: $480,000

On a 30-year loan at 5.68%, that translates to savings of over $100 per month.

When Offset Accounts Shine

- You maintain steady savings or cash flow.

- You want flexibility: access to funds at any time, while cutting interest.

When Offset Might Not Be Worth It

- If your balance is usually low, account fees may outweigh the benefits.

- A simpler loan with a lower rate may save you more in the long run.

Takeaway for you: Offset accounts can be powerful, but they’re not one-size-fits-all. Consider your cash flow patterns before deciding.

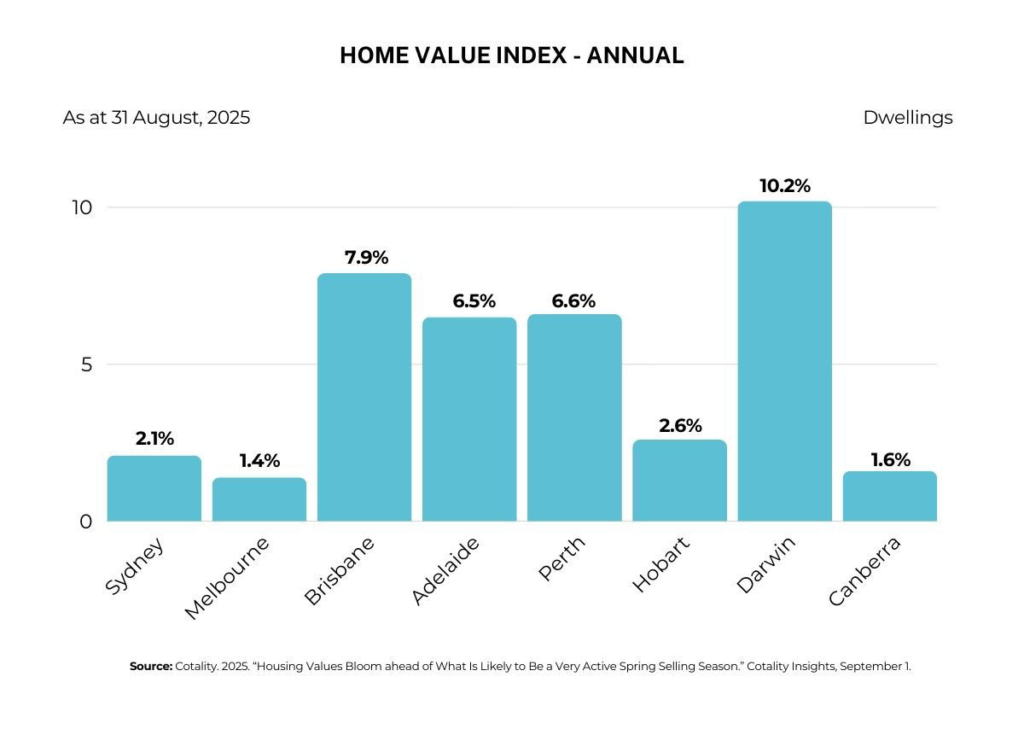

Property Prices: Seven Straight Months of Growth

The property market continues to defy gravity, with Australia’s median home price rising 0.7% in August, marking seven consecutive months of growth. According to Cotality, three major forces are driving this trend:

- Interest rate cuts in 2025 have boosted borrowing capacity.

- Wages outpacing inflation have further strengthened household budgets.

- Supply shortages remain critical while transactions are 4% above the five-year average, and listings are 20% below seasonal norms.

This imbalance between demand and supply is underpinning price resilience.

Why You Need Pre-Approval in Today’s Market

With competition high, securing loan pre-approval before house-hunting is more important than ever:

- Show you’re serious: Sellers favour buyers with finance already sorted.

- Know your limit: Avoid wasting time on homes beyond your borrowing capacity.

- Move quickly: Be ready to make a firm offer without delays.

- Stronger negotiation: Pre-approval can make your offer stand out in a competitive bidding environment.

Takeaway for you: If you’re planning to buy this spring, arrange pre-approval early to stay ahead of the pack.

Australians Are Swiping Less: Credit Card Numbers Fall 1.7%

One of the quieter but significant financial shifts is Australians’ reduced reliance on credit cards. As of July 2025:

- The number of personal credit cards in circulation dropped 1.7% year-on-year.

- The amount of debt accruing interest fell 0.4%.

This change reflects a broader movement towards financial discipline and healthier household budgets.

Why This Matters for Home Loans

Lenders scrutinise every financial detail when assessing mortgage applications. Credit cards, whether or not you use them, are seen as potential liabilities because of their available credit limits.

By reducing or eliminating cards, you can:

- Strengthen your risk profile: Less debt makes you more appealing to lenders.

- Boost borrowing power: Lower credit limits increase how much a bank may lend you.

- Simplify money management: Fewer accounts mean easier budgeting.

Takeaway for you: If you’re preparing for a home loan, trimming your credit cards could significantly improve your chances of approval and increase your borrowing power.

What Does This All Mean for You?

The September property and finance landscape reveals a mixed picture:

- Borrowers are resilient, keeping up with repayments at record levels.

- Offset savings are growing, helping households manage interest costs.

- Property prices keep rising, fuelled by demand and supply constraints.

- Credit card use is falling, strengthening borrower profiles.

Combined, these trends suggest that while challenges remain, particularly around affordability and rising prices, Australians are adapting smartly.

Final Thoughts: Your Next Move

Whether you’re a first-home buyer, investor, or considering refinancing, the key is aligning your loan strategy with your financial situation. In a market shaped by cautious borrowers, rising savings, and shifting spending habits, having the right loan structure can make all the difference.

If you’d like personalised guidance, whether it’s comparing home loans, planning a refinance, or working towards your property goals this spring, let’s talk.

** General Advice Warning

The information provided on this website is general in nature only and it does not take into account your personal needs or circumstances into consideration. Before acting on any advice, you should consider whether the information is appropriate to your needs and where appropriate, seek professional advice in relation to legal, financial, taxation, mortgage or other advice.