Rateseeker Round-up: November Property News

The property and lending landscape remains dynamic as we approach the Reserve Bank of Australia’s (RBA) final cash rate decision for the year on December 10. Recent data indicates a modest national home value increase of 0.3% in October, marking the 21st consecutive month of growth.

However, this growth is accompanied by a rise in property listings, with Melbourne leading at 45,372 homes for sale in November, a 7.6% increase from the previous month.

The rental market is also experiencing shifts. National vacancy rates rose to 1.8%, up 0.4 percentage points from last year, indicating a slight easing in rental tightness.

As we await the RBA’s upcoming decision, these developments emphasise the importance of staying informed about the evolving property and lending environment.

Have you missed the latest news from the past month?

In this property update, we explore the federal government’s ambitious housing targets to the rising tide of property investment; the market continues to evolve in response to economic conditions and policy shifts. For borrowers and investors alike, understanding loan features such as redraw and offset accounts, as well as exploring innovative financing solutions for renovations, can provide the tools needed to make informed decisions.

Renovating Your Home? Here are 3 Ways to Finance It

Renovations are a hot trend among Australian homeowners, with an eyewatering $2.84 billion spent on alterations and additions in the June 2024 quarter alone, according to the Australian Bureau of Statistics. Whether it’s updating a bedroom, revamping a bathroom, or creating your dream kitchen, understanding the costs and financing options is crucial. Typical renovation costs range from $2,000 to $5,000 for bedrooms, $15,000 to $30,000 for bathrooms, and $25,000 to $50,000 for kitchens, according to estimates from Aussie construction experts.

If you’re planning to renovate, here are three practical ways to finance your project:

1. Take Out a Construction Loan

A construction loan is tailored for large-scale renovations and provides funds in stages as the project progresses. During the construction phase, you’ll only pay interest on the funds you’ve used, helping to manage cash flow. Once the work is complete, the loan transitions to a standard principal-and-interest home loan. This option can offer financial flexibility and structure for extensive projects.

2. Consider a Personal Loan

For smaller renovations, a personal loan might be a faster and more straightforward option. The application process is generally simpler than a construction loan, and approval rates can be higher. However, keep in mind that interest rates on personal loans are typically higher, so you’ll need to factor this into your budget.

3. Pay Cash-Money

If you’ve saved up, paying cash is the most straightforward way to fund your renovation. It avoids interest and loan repayments, giving you peace of mind and financial freedom. However, ensure you leave enough savings for emergencies or other financial needs.

A Word of Caution: Avoid Using Credit Cards for Renovations

While credit cards may seem like an easy option with no application process, their high interest rates can quickly lead to a debt spiral. This method can pose significant financial risks unless you’re confident in your ability to repay the balance in full immediately.

Renovating your home is an exciting journey, and choosing the right financing method can help ensure your project runs smoothly and stays within budget. Carefully evaluate your options and pick the one that best suits your financial situation and renovation goals.

The Rise of Property Investment: Why Australians Are Jumping In

Property investment is on the rise in Australia, with new data revealing a growing trend among investors entering the market. CoreLogic’s Head of Research, Eliza Owen, highlighted that the number of property investors is increasing, with investor-related home loan commitments surpassing the number of investor-related listings.

Inferred investor listings have been trending higher since March this year, reaching 13,000, but they remain well below the peak of 2021,

Eliza Owen- CoreLogic Head of Research

Meanwhile, new investor loan commitments stood at 18,400, significantly above the five-year monthly average of 14,516. This surge in activity reflects a renewed confidence in the property market and the enduring appeal of real estate as a wealth-building strategy.

Why Property Investment is So Attractive

Australians are drawn to property investment for several reasons, with three key benefits often making it an appealing choice:

- Capital Growth

Investing in property offers the potential for capital growth as property values increase over time. This can build significant wealth for investors who purchase in high-demand areas or during market upswings. - Ongoing Rental Income

A steady rental income stream can help cover mortgage repayments and other expenses, making it a sustainable long-term investment strategy. - Tax Benefits

Negative gearing allows investors to offset property-related losses against their taxable income, reducing the overall tax burden and enhancing the financial viability of their investment.

Thinking About Investing?

Understanding your finances is essential if you’re considering an investment property. By modelling various repayment scenarios, you can decide whether property investment aligns with your financial goals.

Reach out to Rateseeker today for expert advice and tailored insights to help you navigate the property investment journey with confidence.

Redraw vs. Offset: Which Home Loan Feature is Right for You?

When it comes to choosing a home loan, many borrowers focus solely on interest rates. However, understanding the features of your loan—such as redrawing facilities and offset accounts—can significantly impact your total mortgage costs and repayment flexibility.

Both redraw and offset accounts share a common benefit: they help reduce the interest you pay. For instance, if you owe $500,000 on your mortgage and have $40,000 in either a redraw facility or an offset account, you’ll only be charged interest on $460,000. However, the two features work differently, and understanding these differences is crucial for selecting the option that suits your needs.

What is a Redraw Facility?

A redraw facility allows you to access extra repayments you’ve made on your home loan.

- How it Works: You build up funds in your redraw account by paying more than your minimum repayment. These extra repayments reduce your loan balance and the interest charged on your loan. You can withdraw (or “redraw”) these funds when needed, subject to the lender’s conditions.

- Considerations: The money technically belongs to the lender, so they can alter the redraw conditions or even restrict your access to the funds, although this is rare. Additionally, some lenders charge fees for each redraw transaction.

What is an Offset Account?

An offset account is a separate transaction account linked to your home loan.

- How it Works: Money deposited into the offset account—such as your salary—reduces the balance on which interest is calculated. Unlike a redraw facility, the funds in your offset account remain fully accessible to you at all times.

- Considerations: Offset accounts often come with higher fees or slightly higher interest rates compared to standard home loans. However, the convenience and flexibility of having immediate access to your funds can outweigh these costs for many borrowers.

The Pros and Cons of Redraw and Offset

Pros:

- Both options help reduce your interest bill and allow you to pay off your loan faster.

- Offset accounts offer full access to your funds, while redraw facilities can be useful for borrowers who want to save but prefer not to access funds easily.

Cons:

- Lenders may charge higher fees or interest rates to include these features in your loan.

- If lenders adjust their policies, redraw facilities may incur transaction fees and have limited flexibility.

Making the Right Choice

Choosing between a redraw facility and an offset account depends on your financial habits and needs. If you prefer flexibility and regular access to your funds, an offset account might be the better option. On the other hand, if you want a structured way to save and don’t need frequent access to extra repayments, a redraw facility could be a good fit.

Before committing to a loan feature, carefully review the costs and conditions. If you need help deciding, contact our team at Rateseeker for tailored advice. They can guide you through the options to ensure your home loan works for you.

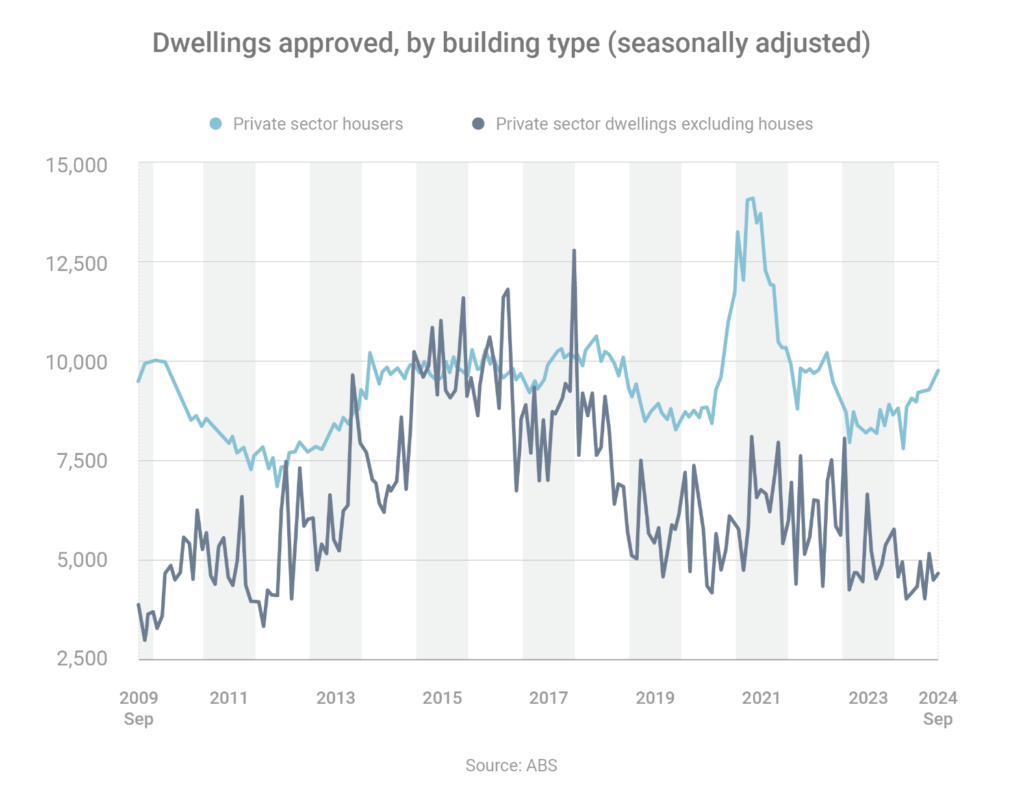

Can the Government’s Housing Affordability Plan Meet Its Ambitious Target?

Housing affordability remains a critical challenge in Australia, and the federal government has set an ambitious goal to address it. By facilitating the construction of 1.2 million homes within five years, starting from July 2024, the government aims to increase housing supply, reduce demand, and place downward pressure on prices. But is this target realistic?

Latest Data Suggests Challenges Ahead

Homebuilding approvals data raises concerns about whether the government’s goal is achievable.

- In the five years to September 2024, only 937,950 building approvals were issued, according to the Australian Bureau of Statistics.

- This is a slight decline compared to the previous five-year period, which saw 949,469 approvals.

To reach the 1.2 million home target, the government will need significantly higher approval rates, especially considering that not all approved projects proceed to completion.

Glimmers of Hope: A Market Recovery

Despite the hurdles, there are positive signs that could support increased homebuilding activity:

- Rising Demand for New Homes: Housing Industry Association economist Maurice Tapang noted that the market has moved past its trough, with more buyers choosing to build new homes.

- Stabilising Costs: The cost of homebuilding materials, which surged during the pandemic, is now growing at a more normal pace.

- Improved Build Times: Construction timelines for houses have returned to pre-pandemic levels, making it easier to deliver projects on schedule.

If these trends continue, they could provide the momentum needed to boost homebuilding activity, ultimately aiding affordability efforts.

A Balancing Act for Affordability

While the government’s target is a lofty one, improving housing affordability will require sustained efforts across multiple fronts:

- Increasing building approvals and ensuring projects proceed to completion.

- Addressing material shortages and ensuring stable costs.

- Encouraging developers and buyers through incentives and streamlined processes.

The target of 1.2 million homes is an ambitious but necessary step toward improving housing affordability in Australia. With favourable market conditions emerging, it remains possible—but will require coordinated efforts across the industry and government.

** General Advice Warning

The information provided on this website is general in nature only and it does not take into account your personal needs or circumstances into consideration. Before acting on any advice, you should consider whether the information is appropriate to your needs and where appropriate, seek professional advice in relation to legal, financial, taxation, mortgage or other advice.