RateSeeker Round-Up: March 2026 Property News

Rates rise, buyer strategies shift, and new opportunities emerge

As we move further into 2026, the property market continues to evolve in ways that are both challenging and full of opportunity. Interest rates are back in focus, first home buyer behaviour is changing, and more Australians are rethinking how and where they buy.

If you are planning to purchase, refinance, or simply review your current loan, now is the time to stay informed. Small changes in rates, policy, or strategy can have a meaningful impact on your long-term financial position.

This month’s update breaks down four key trends shaping the market right now:

- Rate rises and what they mean for borrowers

- The growing role of the 5% Deposit Scheme

- Fixed versus variable loans in today’s environment

- Why building a home is back on the radar

Let’s take a closer look at what is happening and what it could mean for your next move.

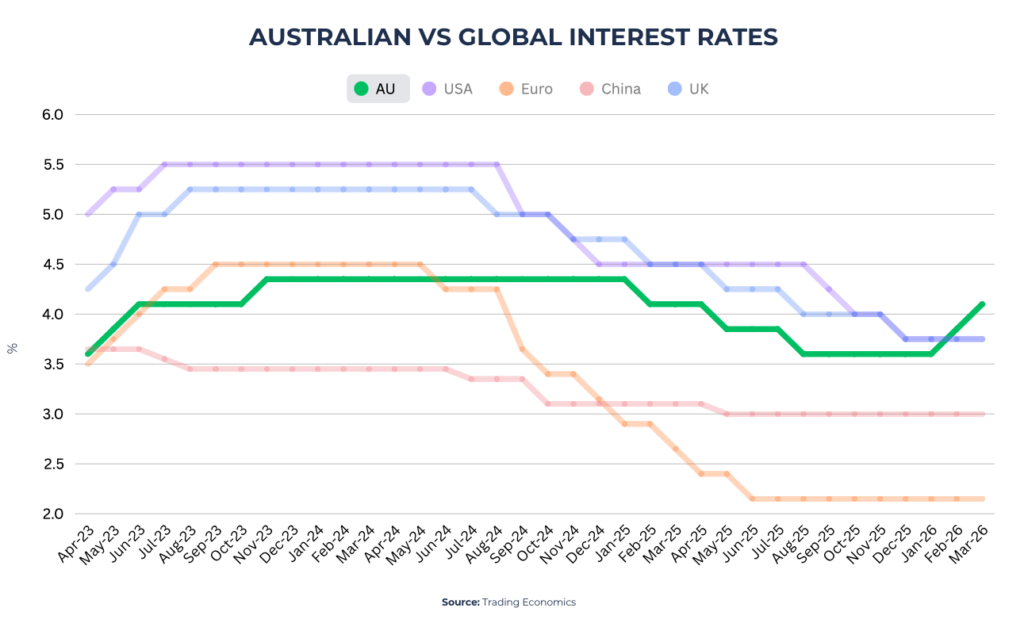

Interest Rate Rises Are Reshaping Borrower Decisions

Over the past few weeks, many lenders have passed on the full 0.25 percentage point rate increase to borrowers. This follows the earlier move in February, meaning many households are now adjusting to two consecutive rate rises in a short period.

For borrowers, this is where the impact becomes real. Repayments are increasing, monthly budgets are tightening, and financial decisions require a bit more planning.

What is driving the rate increases?

Australia is not operating in isolation. Globally, interest rates remain elevated as central banks continue to manage inflation and economic stability. This broader environment is influencing local lending conditions.

At the same time, lenders are adjusting both variable and fixed rates based on expectations about where interest rates are heading, not just where they are today.

What this means for your repayments

Even a relatively small rate increase can have a noticeable impact over time. For many borrowers, the combined effect of recent rate movements is now starting to show up in their monthly cash flow.

This is also the point where differences between loans become more important.

Two borrowers with similar loan sizes can be paying very different amounts depending on:

- Their interest rate

- Their loan structure

- Features like offset accounts or redraw facilities

Why now is the time to review your loan

When rates move, lenders do not always adjust pricing in the same way. Some pass on changes in full, others partially, and some reprice more aggressively than others.

This creates gaps in the market.

If you have not reviewed your loan recently, there is a chance you could be paying more than necessary. Even a small difference in rate can translate into meaningful savings over the life of your loan.

Taking a few minutes to check where your loan stands today can give you clarity and potentially improve your financial position.

The 5% Deposit Scheme Is Changing How Buyers Enter the Market

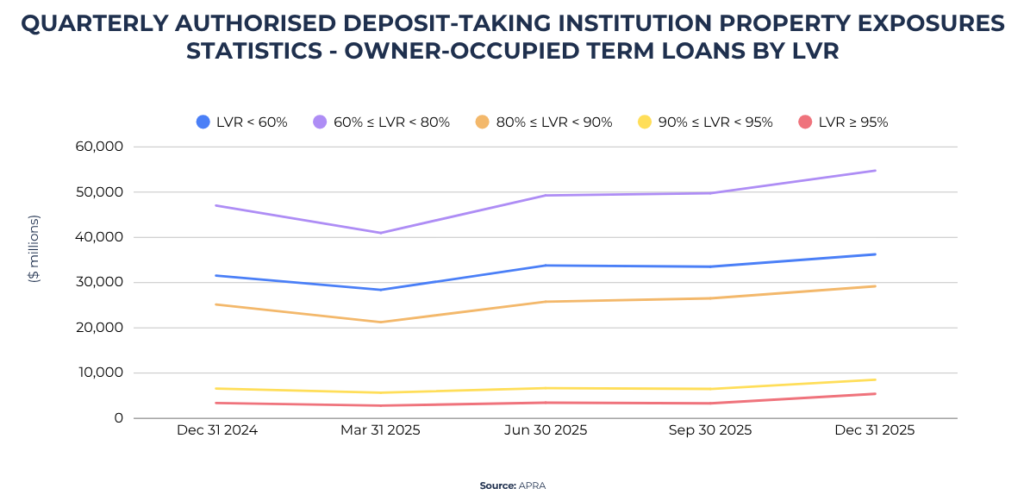

Despite rising interest rates, more buyers are entering the property market earlier than expected. One of the biggest drivers behind this shift is the expansion of the 5% Deposit Scheme.

Recent data shows a significant increase in borrowers purchasing with smaller deposits. The share of owner occupier loans with a deposit of 5% or less has risen sharply over the past year.

Why more buyers are using smaller deposits

The key appeal of the scheme is simple.

Eligible buyers can purchase a property with just a 5% deposit without paying lenders mortgage insurance. This can save tens of thousands of dollars upfront.

For many first home buyers, this removes one of the biggest barriers to entry.

Instead of waiting years to save a 20% deposit, buyers are choosing to enter the market sooner.

What this means in practice

This shift is having a real impact on buyer behaviour.

More buyers are:

- Entering the market earlier

- Targeting properties within scheme price caps

- Exploring more affordable suburbs or regional areas

In a higher rate environment, affordability still matters. So buyers are adjusting their expectations and strategies to match their borrowing capacity.

What you need to consider before using the scheme

While the scheme opens doors, it is not a one size fits all solution.

Key factors include:

- Eligibility criteria

- Property price caps based on location

- Lender participation and policies

- Your long term repayment comfort

Even though the deposit requirement is lower, the loan size is higher. That means repayments need to be manageable not just today, but over the long term.

Why structure matters more than ever

Getting the structure right is critical.

Choosing the right lender, understanding how the scheme works, and aligning the loan with your financial goals can make a significant difference.

For many buyers, the opportunity is not just entering the market, but doing so in a way that remains sustainable.

Fixed vs Variable Loans: What Matters in Today’s Market

One of the most common questions right now is whether to fix your loan or stay variable.

The answer is not as straightforward as it once was.

What is happening with fixed rates

Over recent weeks, fixed rates have been repriced across the market. Many lenders moved early, increasing fixed rates ahead of the latest rate rise.

Sub 5% fixed rates have largely disappeared, with most new offers now sitting higher.

This reflects rising funding costs and increasing bond yields.

Why fixed rates are moving differently

Fixed rates are not directly tied to the central bank cash rate.

Instead, they are influenced by:

- Wholesale funding costs

- Bond market movements

- Market expectations of future interest rates

In simple terms, fixed rates reflect where lenders think rates are going, not where they are today.

What we are seeing across loan terms

Different fixed terms are moving in different ways:

- Shorter term fixed rates have increased more noticeably

- Longer term fixed rates have been more stable, but still trending higher

- Pricing is increasingly forward looking

What this means for borrowers

The conversation has shifted.

Fixed rates are no longer just about securing a lower rate. They are about certainty.

Some borrowers are choosing to fix part of their loan to lock in repayments. Others are staying variable to maintain flexibility.

There is no single right answer.

Why loan structure is becoming more important

In this environment, many borrowers are focusing less on chasing the lowest rate and more on building the right structure.

This might include:

- Splitting the loan between fixed and variable

- Using an offset account to reduce interest

- Maintaining flexibility for future changes

The goal is to create a loan that supports your plans, not just one that looks good on paper.

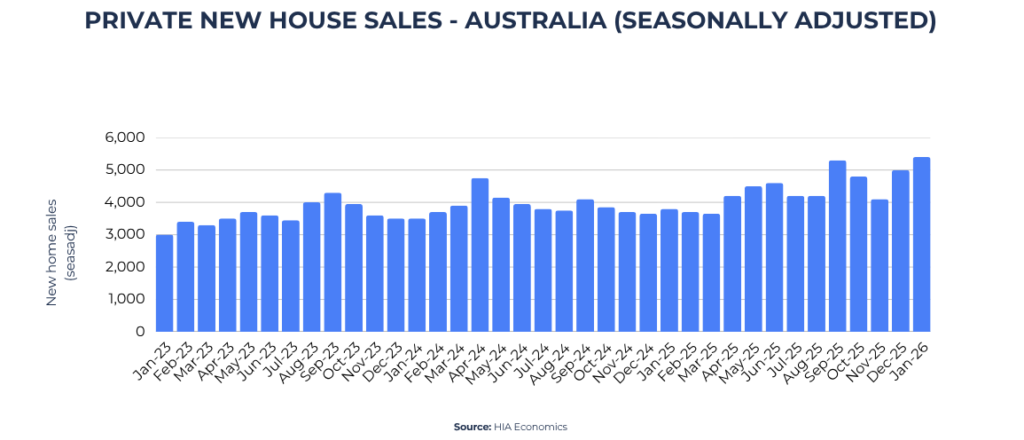

Building a Home Is Back on the Radar

As property prices continue to rise, more buyers are considering building instead of buying an existing home.

New data shows a strong increase in new home sales, reflecting growing demand in the construction space.

Why more buyers are choosing to build

There are several reasons behind this shift.

Strong population growth has pushed up demand for housing, which in turn has increased prices in the established market.

For some buyers, this makes building a more attractive option.

In many areas, new builds are now competitive in price compared to established homes.

What makes building appealing

Building offers a few key advantages:

- Potential access to government incentives

- The ability to customise your home

- Newer properties with fewer maintenance issues

- Opportunities in growing or emerging areas

For first home buyers and investors alike, this can open up different pathways into the market.

How construction finance works

Financing a build is different from a standard home loan.

Instead of receiving the full loan upfront, funds are released in stages as construction progresses.

These stages typically include:

- Foundation or slab

- Frame

- Lock up

- Fit out

- Completion

During construction, you usually pay interest only on the amount that has been drawn down.

This can help manage cash flow, especially if you are paying rent or an existing mortgage at the same time.

What to plan for before building

While building can offer value, it also requires careful planning.

Key considerations include:

- Budgeting for unexpected costs

- Understanding timelines and potential delays

- Ensuring your loan structure matches the build process

- Having the right documentation ready for approval

Construction loans involve more moving parts than standard loans, so preparation is essential.

What This Means for Buyers and Homeowners Right Now

When you step back and look at the broader picture, a few themes stand out.

1. Rates are influencing behaviour, not stopping activity

Even with rate increases, buyers are still active. The difference is in how they approach the market.

More buyers are adjusting expectations, exploring different locations, and focusing on affordability.

2. Flexibility is becoming more valuable

With uncertainty around rates, flexibility in your loan structure matters more.

Being able to adapt as conditions change can make a significant difference over time.

3. Strategy is replacing guesswork

Whether it is using a smaller deposit, choosing between fixed and variable, or deciding to build, borrowers are becoming more strategic.

Decisions are less about timing the market and more about structuring finances in a way that works long term.

Final Thoughts

The property market is never static, and right now it is going through another period of adjustment.

Interest rates are moving, buyer behaviour is shifting, and new opportunities are emerging for those who understand how to navigate the landscape.

Whether you are:

- Buying your first home

- Considering an investment

- Refinancing an existing loan

- Exploring a new build

The key is to stay informed and make decisions based on your own numbers, not just headlines.

A small adjustment today can have a lasting impact on your financial future.

If you are unsure how these changes affect your situation, or you simply want clarity on your options, it can be helpful to step back and review your position.

Because in a changing market, the right strategy is not about reacting quickly. It is about moving forward with confidence and a clear plan.

** General Advice Warning

The information provided on this website is general in nature only and it does not take into account your personal needs or circumstances into consideration. Before acting on any advice, you should consider whether the information is appropriate to your needs and where appropriate, seek professional advice in relation to legal, financial, taxation, mortgage or other advice.