Rateseeker Round-Up: August Property News

The Reserve Bank of Australia’s latest rate cut is reshaping the property and finance landscape. Lower borrowing costs are lifting household borrowing power, driving a surge in refinancing activity, and keeping new home sales elevated. Meanwhile, investors are steadily re-entering the market, adding further competition.

Here are the key trends impacting households this month:

- Borrowing power strengthens with lower rates

- Refinancing activity continues to climb

- New home sales remain elevated despite a monthly dip

- Investor lending rises, providing a broader market context

- Wage growth supports household confidence

Rate Cuts Lift Borrowing Power

The RBA’s cash rate cut has directly increased household borrowing capacity. Lower rates mean smaller monthly repayments, allowing buyers to qualify for larger loans.

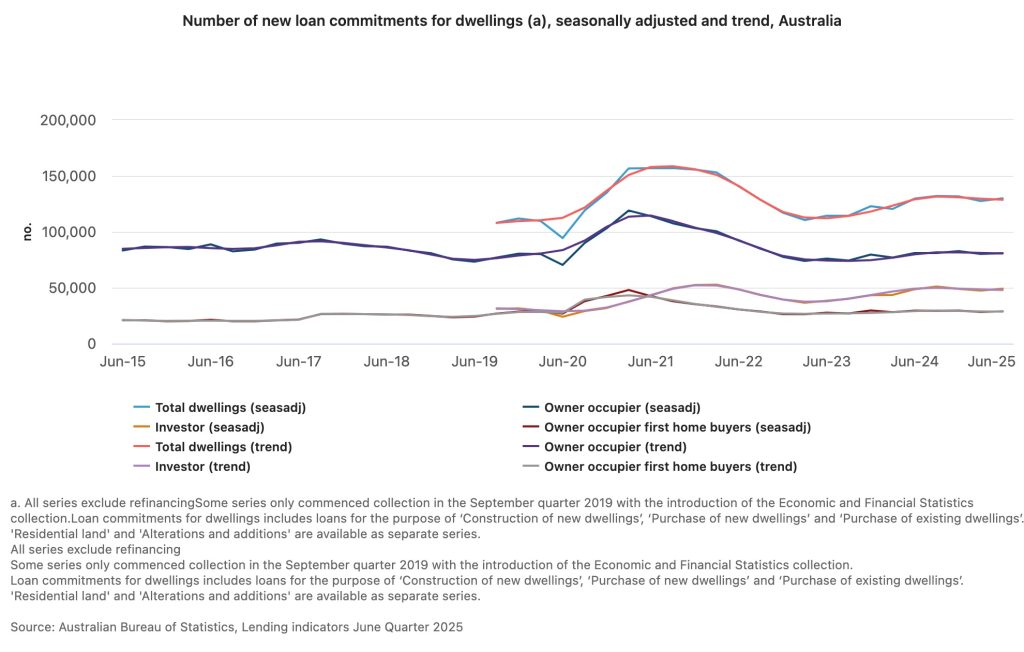

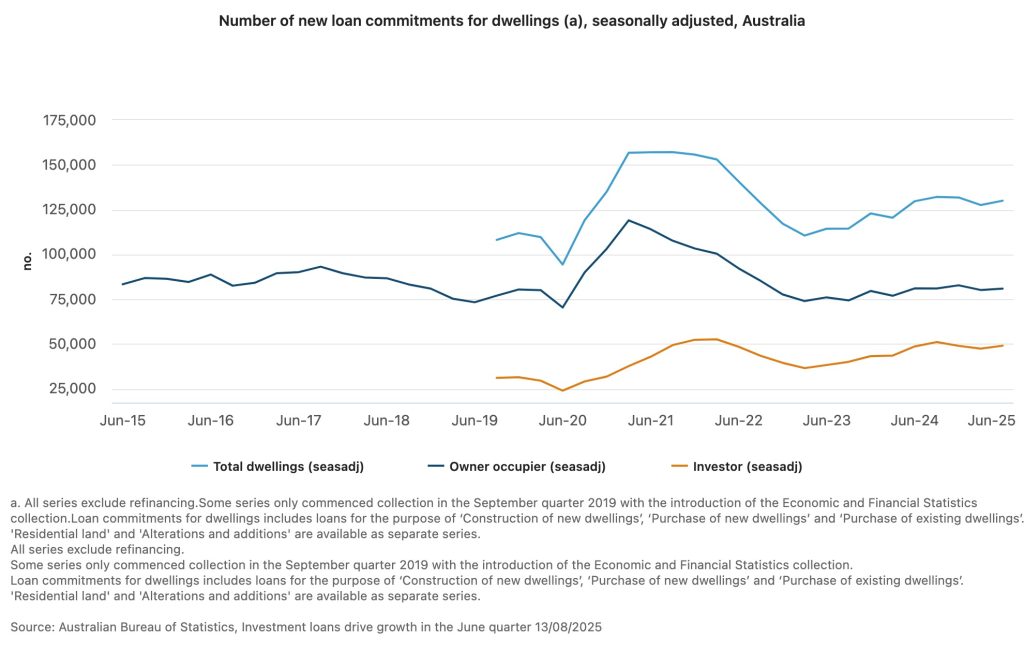

ABS data shows investor loan commitments rose 3.5% in the June quarter, signalling broader momentum across the market. For households, this translates into greater flexibility—whether buying a first home, upgrading, or renovating.

Previously, strict serviceability buffers limited the amount of borrowing households could afford. With lower rates, lenders are adjusting their calculations, which makes it easier for many to qualify for higher loan amounts. This shift could open up opportunities in suburbs or property types that were previously out of reach.

Still, experts caution against over-stretching. While approvals may be higher, staying within a manageable budget remains key to long-term financial stability. Families are encouraged to plan ahead and avoid relying solely on maximum borrowing capacity when making decisions.

Importantly, the boost in borrowing power is not just about purchasing property. Many households are also using the flexibility to consolidate existing debt, finance renovations, or direct funds towards other long-term financial goals. For first-time home buyers, a clear strategy is especially crucial to navigating today’s competitive market.

Refinancing Hits Record High

Refinancing continues to surge as households seize the opportunity to lock in lower repayments. ABS data show that external refinancing did not rise as much as initially thought, and year-on-year figures remain lower than those of the same quarter last year.

Borrowers are switching to more flexible loan structures, consolidating debts, and freeing up cash flow. Many are working with mortgage brokers to compare options and avoid costly fees or unsuitable loan terms.

Refinancing can deliver thousands in savings over the life of a mortgage, making it an attractive option for families looking to improve their financial position in 2025.

What Households Should Consider Before Refinancing

While refinancing can provide clear benefits, it is not always a one-size-fits-all solution. Key factors to weigh include:

- Loan Structure: Should You Choose a Fixed or Variable Rate? Fixed rates offer certainty, while variable rates provide flexibility.

- Costs and fees: Establishment, exit, and discharge fees can erode potential savings.

- Lender policies: Each lender applies different credit assessment criteria, which can affect approval outcomes.

This is where mortgage brokers play a valuable role, helping borrowers compare multiple lenders, simplify the process, and ensure that refinancing delivers genuine savings.

For households wanting to reduce repayments or free up cash flow, refinancing remains one of the strongest opportunities available in today’s market.

New Home Sales Hold Strong

Despite a 6.4% decline in July, new home sales remain at elevated levels. The Housing Industry Association notes that the end-of-financial-year incentives in June likely brought forward demand, explaining the dip.

Over the three months to July, sales were up 15.9%, the highest since September 2022. This highlights continued appetite for new builds, particularly in family-friendly suburbs and growth regions.

Construction Loans Explained

For those looking to build, understanding construction loans is essential:

- Funds are released in stages as building milestones are completed.

- Repayments are typically interest-only during construction.

- Interest is only charged on amounts drawn down.

- Stage inspections are required before each payment is released.

- After construction, loans usually convert to a standard mortgage.

This structure gives households flexibility to manage repayments while their home is being built. Planning ahead ensures families can budget effectively and avoid unnecessary financial pressure during construction.

Investor Lending on the Rise

Investor activity continues to grow, with new investment (investor) loan commitments rising 3.5% in the June 2025 quarter. ABS reports that around 49,065 new investor loans were approved, with a total value of $32.9 billion.

Year-on-year growth has slowed, with investor loan numbers rising only 0.8% compared to the same period last year.

While precise market share statistics (e.g. what percentage of all new home loans are investor loans) vary by source, it is clear that investor lending remains historically high and is contributing to heightened competition in some suburbs.

Wage Growth Supports Household Confidence

The Wage Price Index rose 3.4% over the year to June 2025, the same rate as in the March quarter. This is down from 4.1% year-on-year growth in June 2024. Wage growth is currently outpacing inflation, offering some relief from cost-of-living pressures.

This combination of stronger incomes and lower interest rates is creating a more supportive environment for households planning property purchases, refinancing, or renovations.

For first-home buyers, wage growth can help offset the challenges of saving for a deposit. For existing homeowners, stronger household income provides stability when considering bigger financial decisions such as building, upgrading, or consolidating loans.

However, economists warn that productivity growth remains weak. Without improvements in this area, sustained wage growth may be harder to maintain.

Broader Implications for Households

The RBA has signalled cautious optimism, with inflation easing and expectations anchored near its target range. For households, this translates into a favourable environment for property decisions in 2025.

Lower rates reduce monthly repayments, freeing up disposable income for savings, renovations, or other priorities. Refinancing opportunities are unlocking significant long-term savings. And a steady supply of new homes is providing realistic entry points for families looking to buy or build.

Importantly, the mix of lower rates, investor activity, and wage growth means conditions are shifting quickly. For households, staying informed is critical to making confident, well-planned property decisions.

Final Thoughts

The RBA’s recent rate cut is giving households more room to move, boosting borrowing power, driving refinancing, and supporting demand for new homes. With investors re-entering the market and wages still outpacing inflation, families have opportunities to act strategically in 2025.

Whether buying, refinancing, or building, understanding the current market is key. A mortgage broker can help you compare lenders, secure the right loan, and avoid costly mistakes.To explore how these market shifts affect your household, contact Rateseeker today for tailored guidance.

** General Advice Warning

The information provided on this website is general in nature only and it does not take into account your personal needs or circumstances into consideration. Before acting on any advice, you should consider whether the information is appropriate to your needs and where appropriate, seek professional advice in relation to legal, financial, taxation, mortgage or other advice.