Rateseeker Round-Up: April 2026 Property & Finance Update

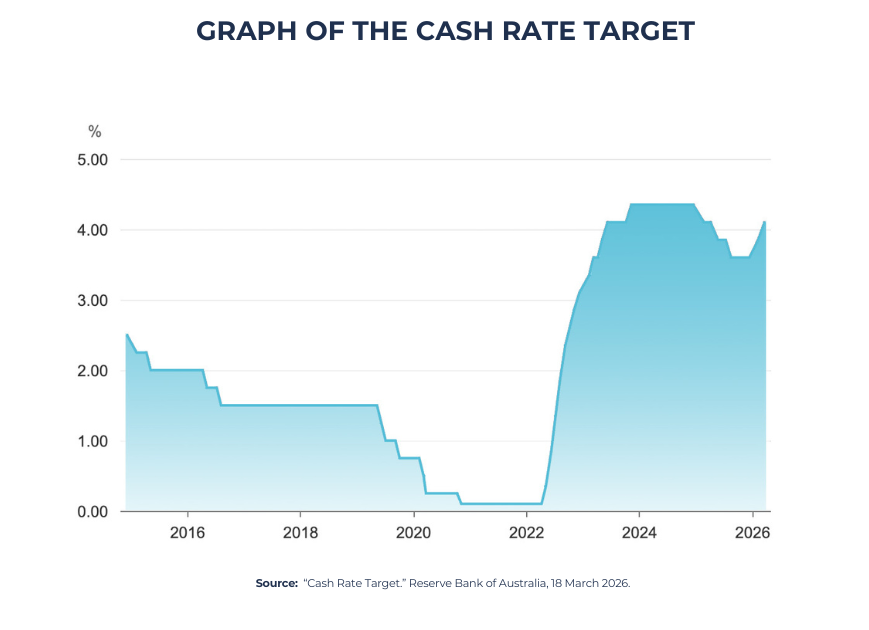

As we move deeper into 2026, many Australian borrowers are reassessing where they stand financially. Interest rates have risen twice already this year, inflation pressures remain a talking point, and global uncertainty continues to influence financial markets.

With the next Reserve Bank of Australia decision scheduled for May 5, homeowners, investors and first home buyers are all asking similar questions. Should I refinance now? Is my loan structure still working for me? Why are property prices still holding up? And is buying a home still realistic in today’s market?

The truth is, conditions are changing, but opportunities still exist for borrowers who stay informed and make strategic decisions.

In this month’s Rateseeker Round-Up, we break down the key trends shaping Australia’s property and lending landscape right now, including:

- The refinancing question more borrowers are asking

- Why offset accounts matter more in a higher-rate market

- Why property prices have remained resilient despite rising rates

- A more realistic pathway from renting to owning

Let’s dive into what these changes mean and how borrowers can respond confidently in the current environment.

Refinancing in 2026: Should You Act Now or Wait?

Over the past few years, many Australians simply focused on surviving rising repayments. But now, more borrowers are shifting from reactive thinking to proactive planning.

They are asking an important question:

“Is my current home loan still the right fit for today’s market?”

That question matters more than ever.

Between inflation pressures, ongoing geopolitical uncertainty, and two interest rate increases already this year, household budgets are under pressure. For many borrowers, repayments have climbed significantly compared to where they were just a few years ago.

As a result, refinancing activity is picking up again.

Why More Borrowers Are Reviewing Their Loans

Many home loans that were competitive a few years ago are no longer particularly sharp in today’s market.

Lenders are constantly adjusting:

- Interest rates

- Cashback offers

- Loan features

- Serviceability policies

The difference between lenders can now be substantial.

Some borrowers are discovering they could potentially:

- Reduce their interest rate

- Improve their cash flow

- Consolidate debts

- Access better loan features

- Structure their repayments more effectively

In a higher-rate environment, even relatively small rate differences can create noticeable savings over time.

The Big Question: Refinance Now or Wait?

This is where many borrowers feel stuck.

On one hand, refinancing now may allow you to:

- Lower repayments sooner

- Improve your loan structure immediately

- Protect yourself if rates continue rising

On the other hand, some borrowers wonder whether waiting could provide:

- Better refinancing deals later

- Lower rates if conditions improve

- Fewer switching costs over time

The reality is there is rarely a perfect moment to refinance.

The right timing depends less on headlines and more on your own situation.

For example:

- Are your repayments becoming uncomfortable?

- Are you still on an outdated rate?

- Do you need more flexibility?

- Are your financial goals changing?

These factors often matter more than trying to predict the exact direction of rates.

Why Loan Structure Matters More Than Ever

Many borrowers focus only on interest rates.

But in 2026, loan structure is becoming just as important.

The right structure can help improve:

- Cash flow

- Financial flexibility

- Long-term interest savings

- Emergency preparedness

Features like:

- Offset accounts

- Redraw facilities

- Split loan structures

- Flexible repayment options

can all play a major role in helping borrowers navigate uncertain conditions more comfortably.

Where to Start

If you are unsure whether refinancing makes sense, the first step is not switching lenders immediately.

It is understanding where your current loan stands compared to the broader market.

That means reviewing:

- Your current rate

- Loan fees

- Repayment structure

- Features

- Long-term plans

Sometimes refinancing can create significant value. Other times, staying put may actually make more sense.

The important thing is making an informed decision rather than simply assuming your current loan is still competitive.

Why Offset Accounts Matter More in a Higher-Rate Market

Offset accounts have always been useful, but in today’s environment, they are becoming far more powerful.

As rates rise, every dollar sitting in an offset account can work harder for you.

Yet many borrowers are still not using their offset strategically.

How an Offset Account Works

An offset account is linked to your home loan and reduces the amount of interest charged on your mortgage.

For example:

If your loan balance is $700,000 and you hold $40,000 in your offset account, the lender only charges interest on $660,000.

This can reduce:

- Interest costs

- Loan duration

- Overall repayment pressure

While the exact savings vary depending on your rate and balance, the long-term impact can be substantial.

Why Offset Accounts Become More Valuable as Rates Rise

In a low-rate environment, offset savings are helpful.

In a higher-rate environment, they become even more powerful.

Why?

Because the interest avoided on that offset balance increases as rates rise.

That means your money is effectively working harder without needing to change your repayment habits.

Borrowers who use offset accounts strategically may benefit from:

- Faster mortgage reduction

- Lower interest costs

- Greater financial flexibility

- Better use of idle cash

Common Mistakes Borrowers Make With Offset Accounts

Not all offset setups are equal.

Some borrowers:

- Leave too much cash sitting in low-interest savings accounts

- Use offset funds inefficiently

- Structure their accounts poorly

- Choose loans with offset features they barely use

In some cases, borrowers pay higher loan fees for offset features without fully understanding how to maximise them.

The key is making sure the structure actually supports your financial habits and goals.

How Smart Borrowers Are Using Offset in 2026

Many borrowers are now using offset accounts as part of a broader cash flow strategy.

This can include:

- Directing salary income into offset

- Keeping emergency funds inside offset

- Using multiple offset accounts for budgeting

- Pairing offset strategies with investment planning

Done properly, this can create both flexibility and long-term savings.

Why Property Prices Have Not Fallen Despite Higher Rates

One of the biggest surprises for many Australians has been the resilience of property prices.

Traditionally, higher interest rates are expected to reduce borrowing power and slow the market.

Yet prices have continued rising in many areas.

So what is actually happening?

The Data Tells a Different Story

According to recent market data:

- National property prices rose 0.7% in March

- New listings increased 3.8% month-on-month

- Total listings remain 6.7% lower than a year ago

This tells us something important.

Supply remains tight.

Even though more homes are coming onto the market, overall housing availability is still constrained.

Supply Remains the Biggest Issue

Australia’s housing shortage continues to play a major role in supporting prices.

Construction activity is struggling to keep pace with demand.

According to Master Builders Australia, forecasts for new housing supply under the National Housing Accord have been revised lower due to:

- Labour shortages

- Rising construction costs

- Delays across the building sector

This means the market is not producing enough homes quickly enough to meet population growth.

Population Growth Continues to Add Pressure

Australia’s population growth remains strong, particularly across major cities.

More people means:

- More housing demand

- More rental demand

- More pressure on existing stock

Even with higher rates, this ongoing demand is helping support property values.

Why Rising Rates Alone Do Not Guarantee Falling Prices

Interest rates are only one piece of the property puzzle.

Property prices are also influenced by:

- Supply levels

- Population growth

- Employment conditions

- Consumer confidence

- Government incentives

Right now, supply shortages are offsetting some of the downward pressure that higher rates would normally create.

This does not necessarily mean prices will rise rapidly forever.

But it does explain why broad price declines have not occurred in the way some expected.

What This Means for Buyers

For buyers waiting for a dramatic market collapse, the reality may be more nuanced.

Instead of large nationwide declines, many markets are seeing:

- Slower growth

- More balanced conditions

- Different performance between suburbs and property types

This is why strategy matters more than headlines.

Understanding:

- your borrowing capacity

- local market conditions

- loan structure

- long-term affordability

can often be more important than trying to perfectly time the market.

Renting vs Buying: Is Home Ownership Still Possible?

For many Australians, particularly younger buyers, the current environment feels frustrating.

Rents are rising.

Property prices remain high.

Interest rates are elevated.

Living costs continue increasing.

It is understandable why many renters feel stuck.

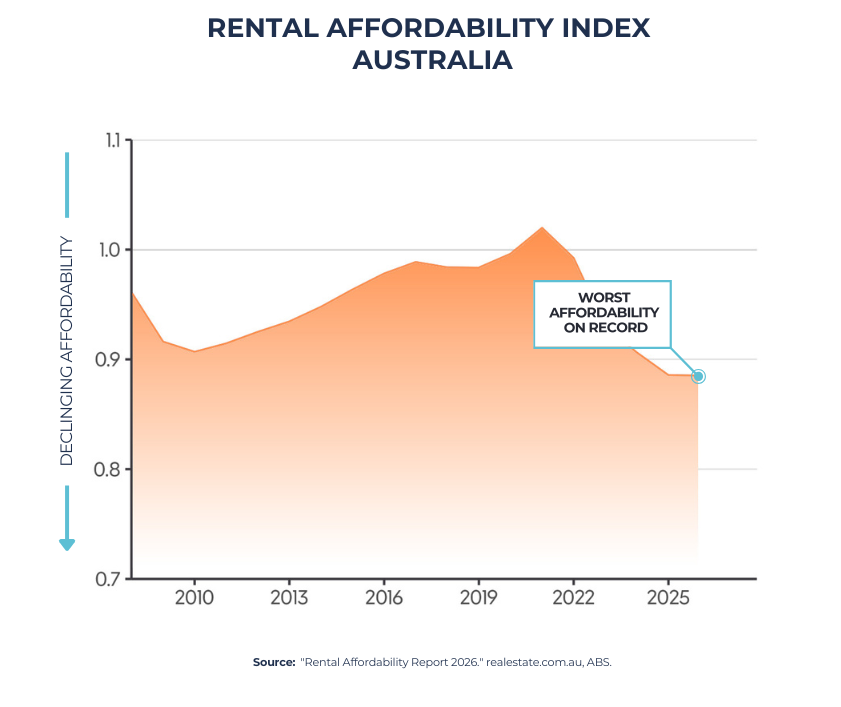

Rental Affordability Is Under Pressure

According to recent data from realestate.com.au, rental affordability is now at its weakest level since at least 2008.

This creates a difficult cycle.

As rents rise:

- Saving becomes harder

- Deposits take longer to build

- Financial pressure increases

Many renters feel as though they are moving backwards financially despite working hard and earning stable incomes.

Why Buyers Are Changing Their Strategy

Rather than waiting for perfect conditions, many buyers are adapting.

Instead of aiming for their dream property immediately, they are exploring more practical pathways into the market.

This includes:

- Buying smaller properties initially

- Considering different suburbs

- Looking at regional markets

- Exploring rentvesting strategies

- Using government support schemes

The shift is psychological as much as financial.

Instead of waiting indefinitely, buyers are focusing on understanding what is achievable now.

What Is Rentvesting?

One increasingly popular strategy is rentvesting.

This involves:

- Renting in an area you want to live in

- Buying an investment property in a more affordable location

For some buyers, this provides a way to enter the market sooner without compromising lifestyle entirely.

Government Schemes Continue to Play a Role

Support schemes such as the 5% Deposit Scheme are also helping some buyers enter the market earlier than expected.

These programs may allow eligible buyers to:

- Purchase with smaller deposits

- Avoid lenders mortgage insurance

- Reduce upfront costs

However, eligibility, borrowing limits and lender policies still matter significantly.

Why Knowing Your Borrowing Capacity Changes Everything

One of the biggest mindset shifts buyers can make is moving from uncertainty to clarity.

Even if you are not ready to buy immediately, understanding:

- What you can borrow

- What deposit you need

- What repayments may look like

can dramatically change your planning timeline.

Many buyers assume ownership is years away without ever properly assessing their position.

In reality, some may be closer than they think.

Final Thoughts

The property market in 2026 is not simple, but it is not impossible either.

Borrowers are navigating:

- rising rates

- higher living costs

- supply shortages

- changing lender policies

At the same time, opportunities still exist for those who stay informed and approach the market strategically.

This month’s trends highlight an important theme.

Small financial decisions now can create significant long-term differences later.

Whether it is:

- reviewing your loan

- improving your offset strategy

- understanding your borrowing capacity

- or exploring realistic pathways into the market

Taking action early often creates more flexibility and confidence moving forward.

At RateSeeker, we help borrowers cut through the noise and make decisions based on real numbers, not fear or speculation.

If you are reviewing your next move in 2026, we are here to help you explore your options and structure a strategy that fits your goals.

** General Advice Warning

The information provided on this website is general in nature only and it does not take into account your personal needs or circumstances into consideration. Before acting on any advice, you should consider whether the information is appropriate to your needs and where appropriate, seek professional advice in relation to legal, financial, taxation, mortgage or other advice.