Rateseeker Property News Round-up September – 2023

Australia’s property market has been a tale of remarkable milestones and perplexing challenges in recent times. Amid the ever-rising property prices, the Federal Government’s Home Guarantee Scheme (HGS) has emerged as a ray of hope for first-time homebuyers, particularly those with modest incomes. Research commissioned by the National Housing Finance and Investment Corporation reveals that HGS is facilitating entry into the market with small deposits, potentially reshaping the landscape for aspiring homeowners.

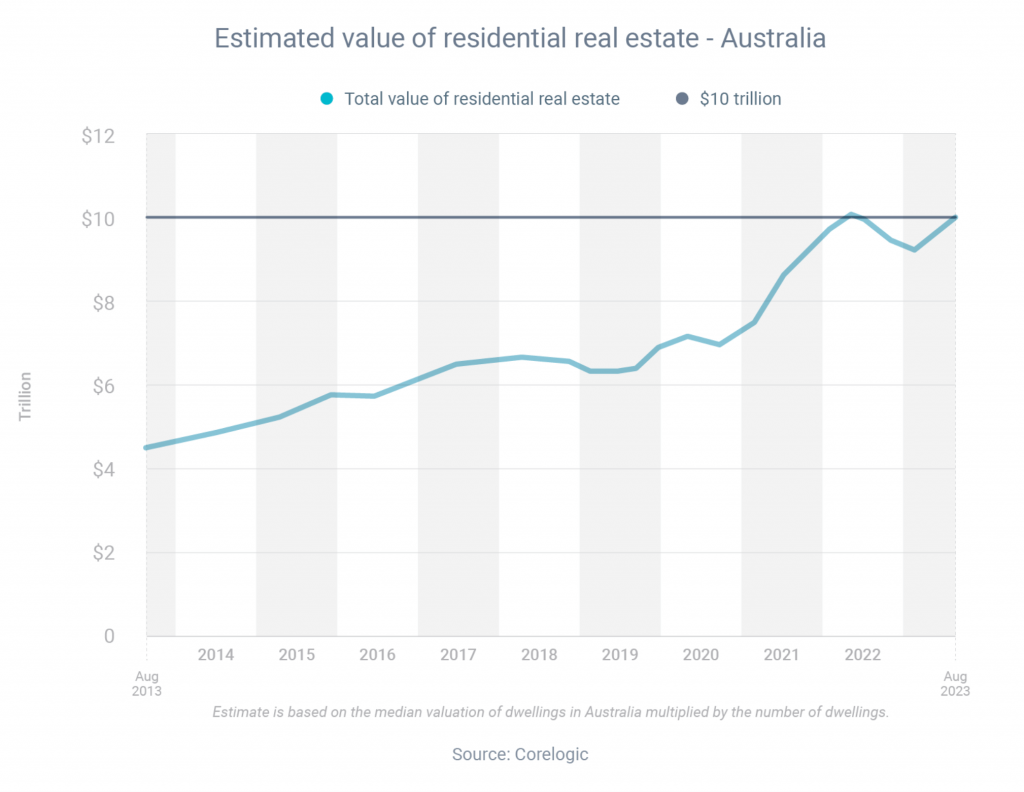

On a broader scale, the combined value of Australian real estate soared to an unprecedented $10 trillion by the end of August, a milestone last seen back in June 2022. The reasons behind this phenomenal growth, however, raise some pertinent questions.

What is driving property prices to these soaring heights, and how does it impact both seasoned investors and those looking to step onto the property ladder for the first time?

In the backdrop of Australia’s bustling property market, the challenge of saving for a home deposit has become increasingly complex, compelling us to delve into the intricacies of our shifting financial landscape. A recent revelation states that household savings have seen a decline over seven consecutive quarters.

The rising cost of living, an omnipresent concern, has added an extra layer of complexity to this savings dilemma. As everyday expenses continue to grow, the dream of homeownership for many seems to drift further away.

Read on as we explore the implications of these persistent trends on the aspirations of hopeful homeowners and the broader financial picture in Australia.

Aussie property market at over $10 trillion milestone

In a notable milestone, the collective worth of Australian real estate surged to an impressive $10 trillion by the close of August, as reported by CoreLogic. This achievement marks the first instance since June 2022 that the real estate market has reached such a pinnacle.

The substantial growth in valuation can be attributed to a dual phenomenon – an upswing in property construction and a simultaneous appreciation in the overall value of housing across the nation.

Interestingly, after breaching the $10 trillion mark last year, the property market embarked on a 10-month downturn, during which the national median property price experienced a decline of 9.1%. However, commencing in March, we have observed a noteworthy reversal of this trend.

Property values have climbed consistently for six consecutive months, accumulating a combined growth of 4.9%. While this resurgence is promising, CoreLogic suggests that the future trajectory of the market remains uncertain. The property landscape continues to evolve, offering both challenges and opportunities.

While the prevailing sentiment leans towards the Reserve Bank of Australia (RBA) concluding its cash rate hikes, the ability to borrow is still hindered by the presence of a relatively elevated serviceability buffer, noted by Core Logic Australia.

APRA’s data up to June revealed that the weighted average assessment rate for home loans hovered just below 9%. Concurrently, Australian Bureau of Statistics housing lending statistics indicate that mortgage lending has experienced a decline in three out of the past four months.

First home buyer scheme delivering results

In the realm of Australian real estate, the federal government’s Home Guarantee Scheme (HGS) has been a pivotal initiative, empowering first home buyers with modest incomes to venture into the property market, all while navigating the constraints of small deposits. Recent research, conducted and commissioned by the National Housing Finance and Investment Corporation, has provided invaluable insights into the scheme’s impact on aspiring homeowners.

Key findings from this research underscore the significance of the HGS:

- Income Insights: The research sheds light on the demographic of HGS participants, revealing an average annual income of $108,000, contrasting with the broader first home buyer market’s average income of $117,000. This data underscores the scheme’s accessibility for those with modest incomes.

- Deposit Dynamics: Examining deposit trends since 2020, the study unravels a 3.4% increment in the average deposit paid by HGS participants, rising from $35,200 to $36,400. In stark contrast, the broader first home buyer market saw a substantial 46.7% surge, elevating the average deposit from $108,400 to $159,000. These figures signify the HGS’s role in addressing deposit challenges.

- Loan Landscape: Tracking loan amounts since 2020, the research reveals a more conservative 4.7% increase among HGS beneficiaries. However, the broader first home buyer market displayed a more pronounced 13.4% upswing. These nuances reflect the tailored nature of the HGS.

- Equity Gains: An interesting revelation from the study is that the average HGS property has enjoyed an equity gain of $82,000. This signifies the scheme’s potential to foster property value appreciation.

The recent data not only offers hope to those aiming to enter the property market but also emphasises the need for multifaceted strategies to cater to the diverse landscape of aspiring homeowners. In a property market that continues to evolve, schemes like the HGS play a pivotal role in shaping accessibility and opportunity.

For eligible applicants, you only need a 5%, however conditions apply. If you’ve been thinking about owning your very first home and want to know more about whether you’re eligible, get in touch with our home loan strategists, we can help crunch the numbers and find the perfect home loan to suit your circumstances and future goals.

Why Aussie property prices are sky high

In a recent address just before concluding his role as Reserve Bank governor, Philip Lowe highlighted the intricate relationship between interest rates and Australia’s property market, shedding light on essential aspects that transcend the influence of interest rates.

While it’s undeniable that Australia has experienced lower interest rates for a significant portion of the past 30 years, contributing to the property price escalation, it’s crucial to acknowledge that interest rates alone don’t account for Australia’s status as one of the globe’s leaders in housing values. Recent news articles emphasise that interest rates in Australia align with those prevalent in most advanced economies.

Philip Lowe states that Australia’s housing price prominence is the result of a multifaceted interplay of societal choices. These encompass decisions regarding our residential preferences, urban planning and zoning regulations, transport infrastructure design, and land and housing investment taxation. Recent news reports have further highlighted the influence of these factors on the property landscape.

In each of these spheres, both society and political leaders have made decisions that ultimately drive urban land and housing costs to higher levels. Recent Australian news articles have elaborated on the impact of these choices in shaping the real estate landscape.

Philip Lowe contends that the solution to mitigating the high cost of housing in Australia, which he identifies as a significant economic and social issue, lies in addressing these multifarious factors. These insights provided by recent news articles align with his view, highlighting the need for comprehensive approaches to resolve Australia’s housing affordability concerns.

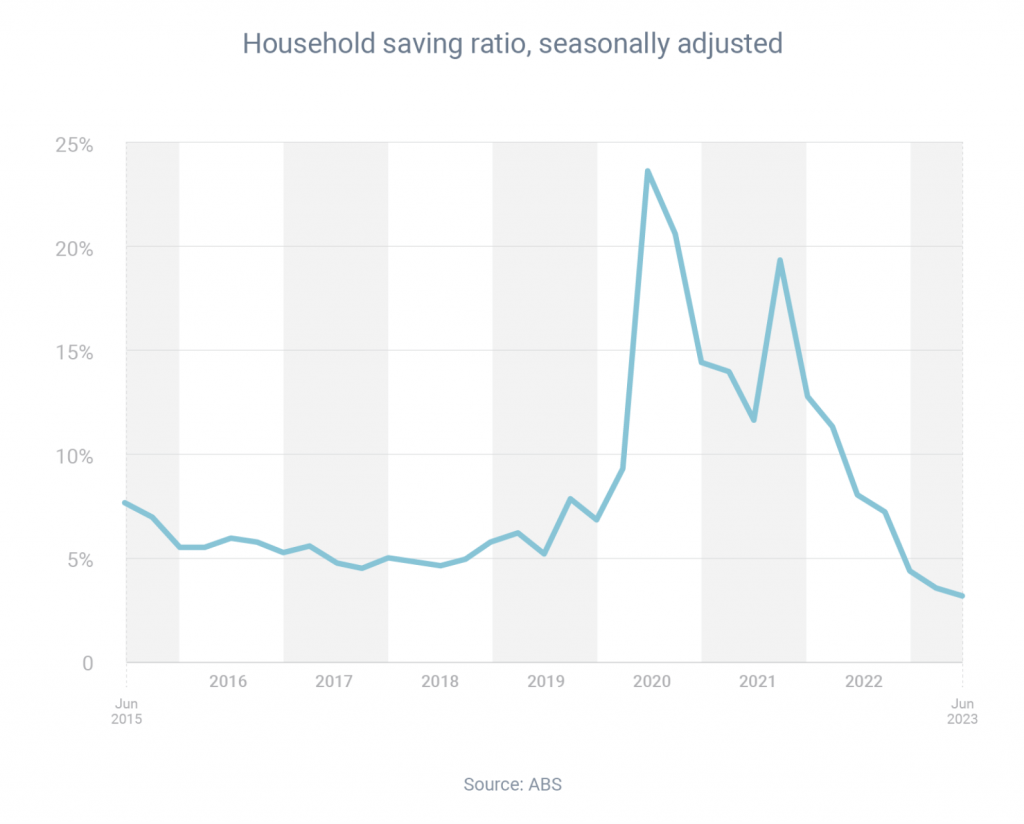

Aussies banking just 3.2% of their pay into savings

Over the span of seven consecutive quarters, there has been a persistent decline in household savings, which signifies the growing challenge faced by consumers in accumulating funds for a home deposit. This challenge is significantly influenced by the surging cost of living. According to recent data from the Australian Bureau of Statistics (ABS), the portion of income that households managed to save has exhibited a marked decrease between the quarters of September 2021 and June 2023:

- Sep-21: 19.3%

- Dec-21: 12.9%

- Mar-22: 11.3%

- Jun-22: 8.1%

- Sep-22: 7.2%

- Dec-22: 4.4%

- Mar-23: 3.6%

- Jun-23: 3.2%

These figures, as highlighted in recent reports, underscore the undeniable strain on households as they grapple with the ever-mounting cost of living. This financial challenge poses a significant obstacle for many individuals aspiring to save for a home deposit in today’s economic landscape, as detailed in recent headlines.

The decrease in savings over recent quarters can be attributed to a complex interplay of factors. The onset of the pandemic saw people spending less during lockdown periods as they were confined to their homes.

Subsequently, a phenomenon known as ‘revenge spending’ emerged, with consumers splurging on various purchases upon regaining a sense of freedom. However, this spending trend also coincided with a period of high inflation, a notable feature of recent times. As highlighted in recent economic reports, this inflationary pressure has led consumers to allocate more of their finances towards acquiring everyday items, effectively diminishing their capacity to save.

Need help?

For those grappling with mortgage repayments and experiencing financial constraints, it’s a wise move to take proactive measures now. Recent financial news reports indicate that lenders are generally more accommodating to borrowers who promptly address any financial challenges they might be encountering.

If you find yourself in such a situation, reaching out to your lender can be a prudent step, enabling you to engage in constructive discussions and explore potential solutions. If you’re unsure of how to tackle the situation, get in touch and we can speak with your lender to help find a solution.

We’ve helped countless Aussie borrowers open doors to their new homes all across the country, let us help you make your dreams a reality.

** General Advice Warning

The information provided on this website is general in nature only and it does not take into account your personal needs or circumstances into consideration. Before acting on any advice, you should consider whether the information is appropriate to your needs and where appropriate, seek professional advice in relation to legal, financial, taxation, mortgage or other advice.