Rateseeker Property News Round-up November – 2023

As we stand on the cusp of bidding farewell to another eventful year, the landscape of home loans and property markets is marked by intriguing dynamics and noteworthy shifts. This month unveils a tapestry of trends that are reshaping the real estate and mortgage sectors. For those closely watching the pulse of the market, the following key developments are making waves as we approach the end of the year.

In the changing landscape of real estate financing, the month of November has seen a palpable surge in home loans activity. Prospective homeowners, driven by a combination of lower-interest rates and increased housing demand, are seizing the opportunity to step onto the property ladder. Lending institutions are moving with the flow by rolling out competitive loan products, delivering a diverse array of options for those ready to embark on their homeownership journey.

Homeowners who purchased during the pandemic driven by a combination of low-interest rates and increased housing demand, have been moving en-masse to variable rate loans, which now dominate the loan market as fixed term loans come to their end.

The latest CoreLogic report unveils a robust surge in median property prices across Australia. Covering 4,506 suburbs, the study offers a comprehensive look at market dynamics from July to October 2023. Impressively, median property prices climbed in 82.4% of local markets, highlighting the resilience and vitality of the real estate sector.

Despite a significant 4.00 percentage point increase in the cash rate from April 2022 to September 2023, banks, driven by competition, raised variable rates by an average of only 3.32 points for owner-occupiers and 3.28 points for investors. This competitive dynamic softened the impact of the interest rate hikes, providing a mitigating effect on borrowers.

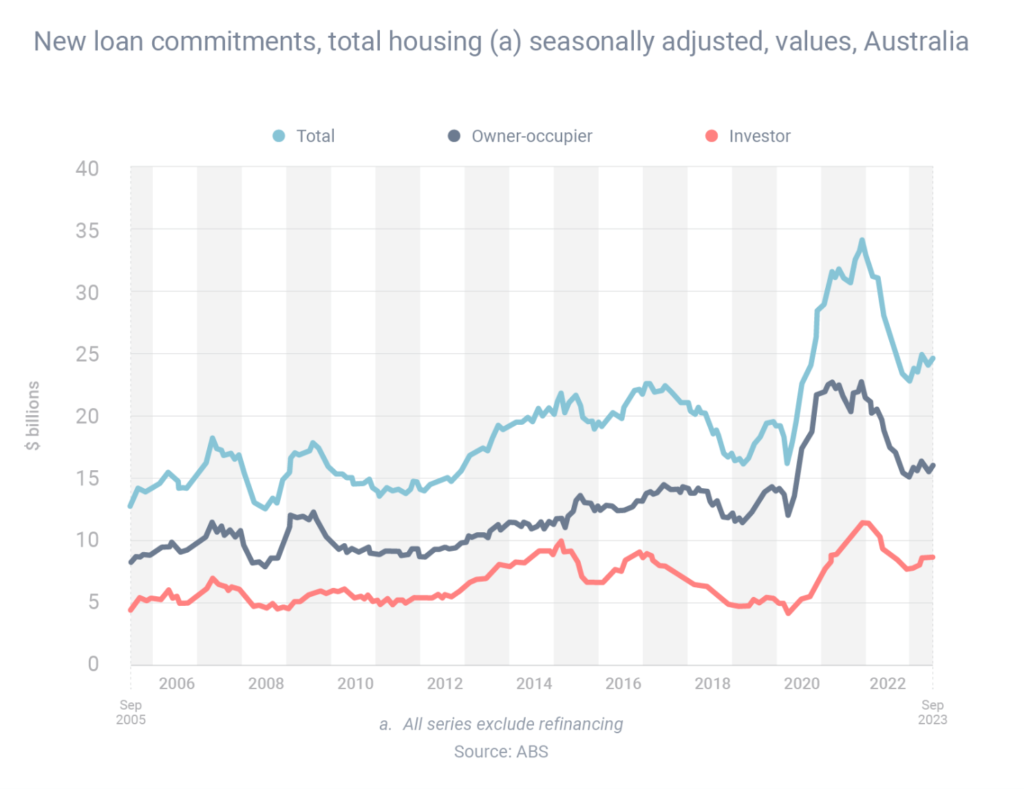

Borrowing on the rise as the property market heats up

The Australian property and mortgage landscape have witnessed a substantial surge in activity, ushering in a new era of opportunities with investors at the forefront. According to the latest data from the Australian Bureau of Statistics covering the period between February and September, the total volume of mortgage commitments surged by an impressive 9.5%, reaching a substantial $25.0 billion.

Investors have emerged as the trailblazers in this dynamic wave of home loans activity. The data reveals a substantial 16.0% surge in investor borrowing, totalling an impressive $9.0 billion. This surge underscores the resilience and confidence in the real estate market, as investors navigate the landscape with a keen eye on opportunities.

Simultaneously, the increase in homeowner activity paints a picture of homeowners the moment. Owner-occupied borrowing witnessed a commendable 6.1% climb, reaching $16.1 billion. Homeownership remains a powerful force, contributing significantly to the overall surge in mortgage commitments during this period.

Three Additional Key Insights:

First Home Buyers Make Their Mark

The journey to homeownership has seen a surge in first home buyer activity, with loans increasing by a remarkable 18.4% to a total of 9,213. This surge signifies a vibrant entry into the property market by aspiring homeowners, adding depth to the evolving landscape.

Refinancing Trends

While refinancing with external lenders experienced a 7.1% decline, settling at $18.5 billion, the figure remains notably above the long-term average. This nuanced trend suggests a strategic financial maneuvering, indicative of the ongoing financial conversations homeowners are having amidst the evolving market conditions.

Renovations and Enhancements

The surge in borrowing for alterations, additions, and repairs, growing by 9.4% to $502 million, unveils a story of homeowners investing in the enhancement and personalisation of their properties. This trend reflects a desire for customisation and adaptability within the evolving homeownership landscape.

If you’ve been thinking about buying your first or next home, get in touch with us at Rateseeker. Our team of experienced home loan strategists can help you navigate through the lending landscape and secure the perfect loan for you.

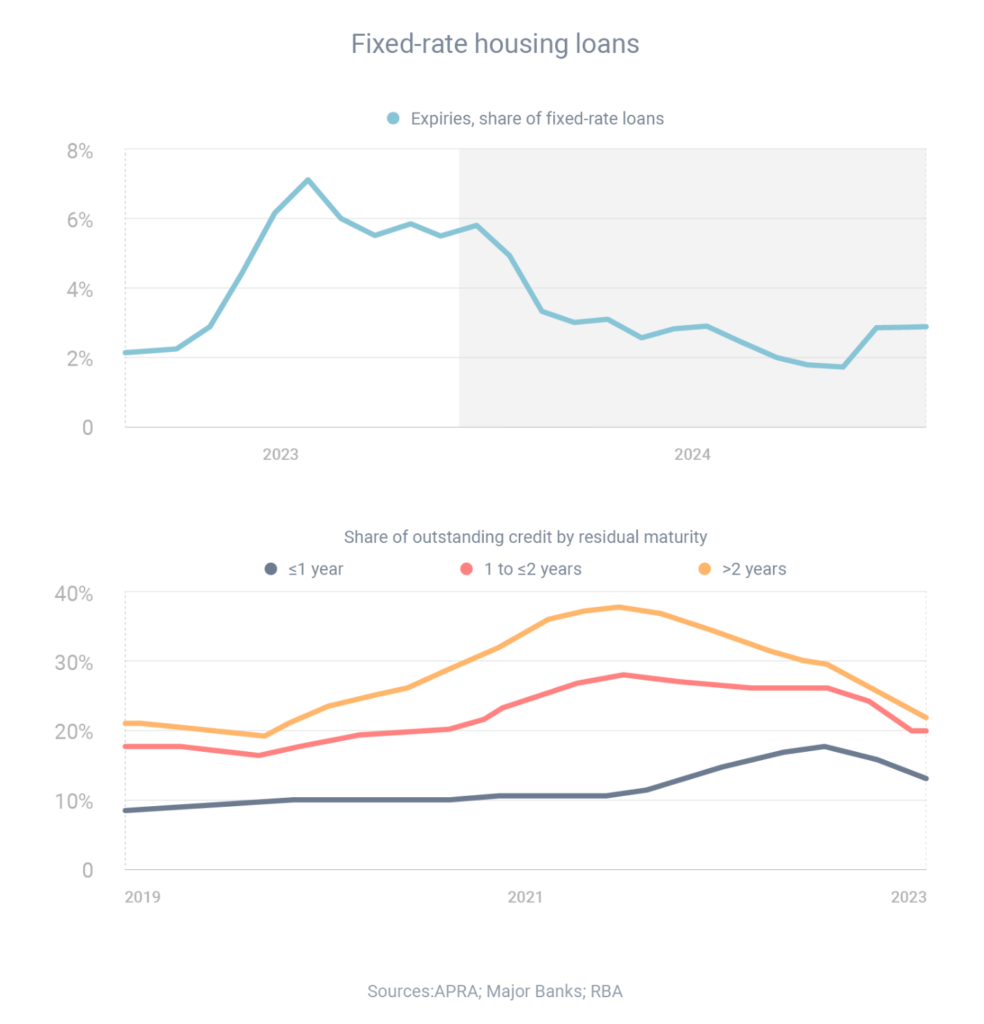

Fixed rate loans falling as variable rate loans dominate

In a notable transformation, the mortgage market is undergoing a profound shift, transitioning from a stronghold of fixed-rate loans to a dominance of variable-rate loans. Recent data from the Reserve Bank reveals the acceleration of this transition, shedding light on the dynamics that have propelled this monumental change.

The years 2020 and 2021 witnessed a surge in fixed-rate loans as interest rates plummeted to historic lows. Borrowers, enticed by the allure of ultra-low fixed rates, flocked to two-year and three-year fixed loans in unprecedented numbers. However, as rates began their ascent, a significant number of these loans expired, leading to borrowers transitioning from the security of fixed rates to the reality of substantially higher variable rates.

The Reserve Bank’s recent Statement of Monetary Policy reveals a substantial decline in the fixed-rate share of total outstanding housing credit. From its zenith just under 40% at the beginning of 2022, the fixed-rate share plummeted to 22% in September. This data paints a vivid picture of the swift and impactful shift in borrower preferences over a relatively short period.

In recent months, the momentum of fixed loans expiring has surpassed the initiation of new fixed loans, creating a ratio exceeding five to one. This unbalanced scale underscores the pronounced trend of borrowers transitioning away from fixed-rate arrangements in favor of the flexibility offered by variable-rate options.

As per the Reserve Bank’s projection, the majority of remaining fixed-rate loans are anticipated to expire by the end of 2024. This impending milestone marks the culmination of the great transition within the mortgage market, highlighting the temporal nature of fixed-rate preferences and the dynamic response of borrowers to changing economic conditions.

If your fixed rate loan is ending soon and you’re keen to refinance with a more competitive variable rate , simply get in touch with us at Rateseeker and can help ensure you’re able to securing the sharpest rate for your new loan.

High interest rates are no match for property market growth

The most recent report from CoreLogic paints a vivid picture of the Australian real estate landscape, showcasing a notable surge in median property prices. Analysing a diverse sample of 4,506 suburbs nationwide, the report unfolds a narrative of growth and resilience over the three months leading to October.

The data reveals a resounding uptick in median property prices, with 82.4% of local markets experiencing an increase. This overarching surge underscores the buoyancy of the real estate sector across various regions, reflecting a robust and widespread growth trend.

Delving deeper, the report highlights the synchronicity between house and unit markets. A remarkable 83.1% of house markets and 80.6% of unit markets witnessed price increases, emphasising the resilience and demand in both segments of the property market.

Focusing specifically on house markets, the report unveils compelling growth statistics across major Australian cities:

- Perth: 99.7% of suburbs experienced price increases.

- Adelaide: 99.0% of suburbs demonstrated growth.

- Brisbane: A substantial 98.7% of suburbs witnessed price upticks.

- Sydney: Maintaining a strong position, 91.4% of suburbs saw prices rise.

- Melbourne: Demonstrating solid growth, 80.8% of suburbs experienced price increases.

- Canberra: A notable 71.1% of suburbs showcased growth trends.

- Hobart and Darwin: Both cities recorded a significant 59.1% surge in house prices, further contributing to the national growth narrative.

In an exploration of Australia’s real estate landscape, CoreLogic’s Head of Research, Eliza Owen, sheds light on the multifaceted nature of the country’s housing markets. Despite facing challenges such as high-interest rates and economic headwinds, many housing markets are demonstrating resilience and growth, marking a departure from the notion of a singular, uniform market.

Owen emphasises that Australia is not a homogenous housing market. Instead, there exists a tapestry of diversity in capital city market performance. This diversity is evident in city-wide growth rates, varying levels of supply across different cities, and the distinctive dynamics present in the suburbs under scrutiny in CoreLogic’s latest report.

City-wide growth rates serve as a mirror to the varied conditions and performance levels across different urban centres. The report not only captures the resilience of these markets but also underlines the role of factors such as supply variations in shaping the growth of the Aussie property market.

Paying attention to the significance of suburb-level analysis in understanding the intricate layers of growth and resilience is key. This granular approach allows for a more detailed examination of the impact of diverse economic conditions and supply dynamics at the local level, showcasing the microcosms that contribute to the overall diversity in Australia’s housing markets.

Thinking about purchasing your dream home in the near future? We can help, simply get in touch with us at Rateseeker and our expert home loan planners are here to ensure you’re securing the best loan for your circumstances.

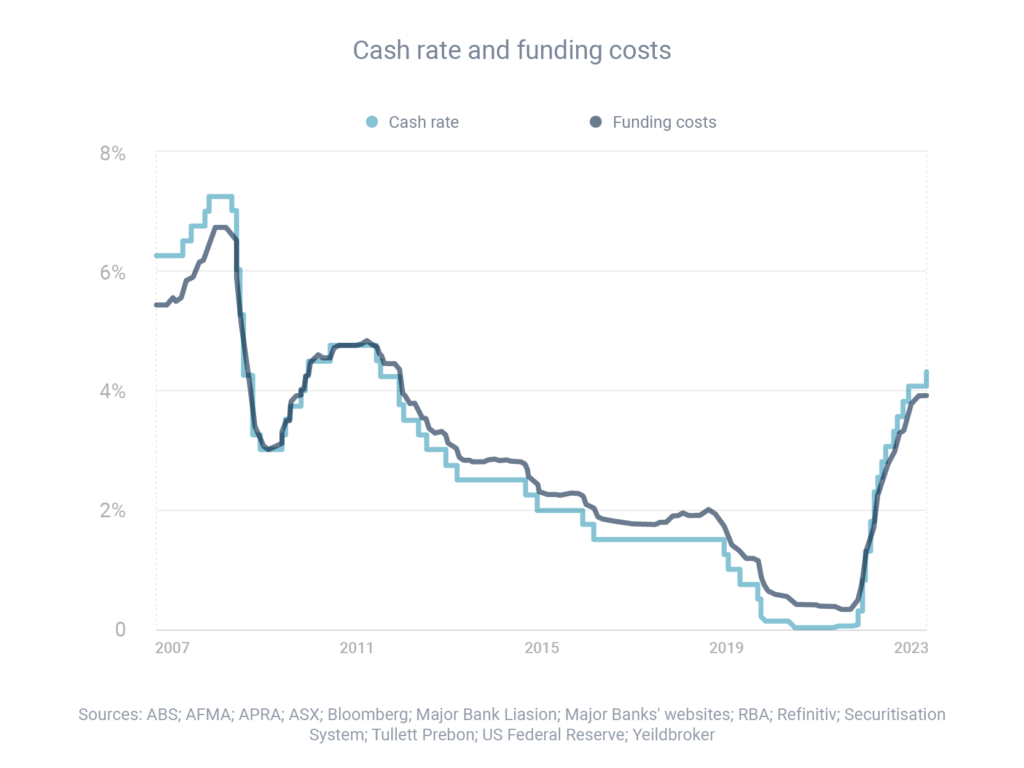

Why interest rates are on the rise

In the face of a notable surge in interest rates over the last 18 months, a glimmer of relief emerges as the Reserve Bank attributes the milder-than-expected increase to the competitive dynamics within the lending landscape. The delicate dance between central policy and market forces has resulted in an outcome where interest rates have risen, but the impact on borrowers has been tempered by robust competition among lenders.

The period from April 2022 to September 2023 witnessed a significant transformation in the interest rate landscape. The cash rate, a key indicator of monetary policy, saw an increase of 4.00 percentage points, reflecting the Reserve Bank’s response to evolving economic conditions and inflationary pressures.

In a balancing act influenced by competitive forces, banks responded to the shifting monetary landscape. The increase in variable rates, while reflective of the broader economic trend, was notably less severe than one might have anticipated. For owner-occupiers, variable rates rose by an average of 3.32 points, while investors experienced a slightly lower increase at 3.28 points.

The backdrop of increased funding costs, particularly between the June and September quarters, poses a new challenge for financial institutions. This surge is attributed to the replacement of maturing bonds issued at lower rates and the upward adjustment of average deposit rates. These factors collectively contribute to an increased cost burden on banks in their pursuit of securing funds.

Banks, acting as intermediaries in the financial ecosystem, acquire funding on the wholesale market. Adding a margin to cover operational costs and ensure profitability, they then channel these funds to borrowers through various loans, including home loans. The rise in funding costs, therefore, reverberates through this interconnected system, prompting a strategic response from banks.

When faced with escalating funding costs, banks find themselves compelled to make adjustments to maintain their financial viability. The standard recourse is to pass on the burden to borrowers by increasing interest rates. This shift, while a pragmatic response from the banks’ perspective, translates to potential financial strain for households relying on loans, especially home loans.

Most importantly, the Reserve Bank acknowledges the pivotal role of competition in mitigating the impact of interest rate hikes on variable-rate housing loans. The interplay between lenders striving for market share has acted as a cushion, softening the blow for borrowers and maintaining a delicate equilibrium between market competitiveness and monetary policy.

Looking to refinance your loan or buy a home while lending competition is fierce? Get in touch with our expert home loan strategists at Rateseeker, who will guide you through over 1000+ loan options from 30+ lenders to find the perfect loan for you.

** General Advice Warning

The information provided on this website is general in nature only and it does not take into account your personal needs or circumstances into consideration. Before acting on any advice, you should consider whether the information is appropriate to your needs and where appropriate, seek professional advice in relation to legal, financial, taxation, mortgage or other advice.