Rateseeker Property News Round-up May 2023

There has been some exciting news over the last month as data reveals that property prices are once again on the rise. With prices slumping over May and February this year, things started to look better across March (0.6% increase) and April (0.5% increase).

The Reserve Bank of Australia is also set to see new changes after a review commissioned by the federal government. The review resulted in 51 recommendations, including specific measures to create a clearer monetary policy framework and stronger monetary policy decision-making.

Although it may be too early to confirm first home buyers have made their come back, according to new data from the Australian Bureau of Statistics – new buyers are making a a welcome return to the market with a 15.8% increase in activity after a five-year low.

For those who own a unit for investment purposes, things are in your favour as prices and rents continue to rise, taking a jump at 14.8% over the year to April and growing significantly faster than housing prices.

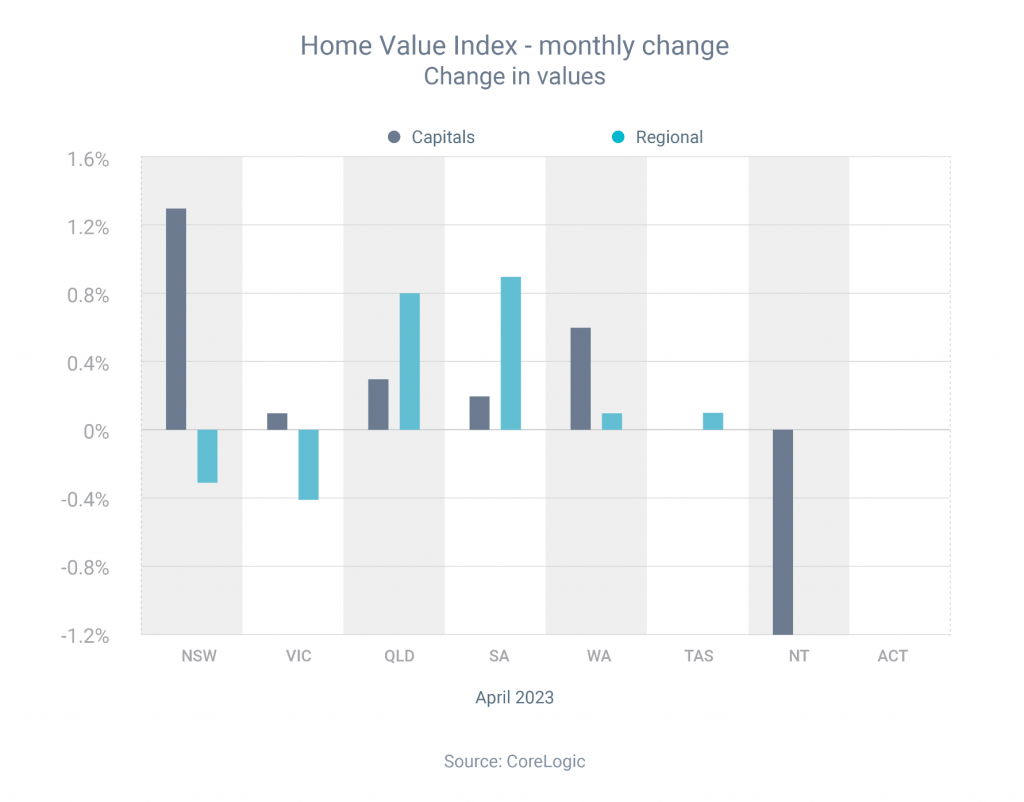

Property prices rising on the steady

According to recent data by CoreLogic, Australian property prices look to be on the rise once again.

It comes as a welcome change for homeowners looking to sell, after the national median price fell 9.1% between May 2022 and February 2023, it has since risen in consecutive months – by 0.6% in March and 0.5% in April.

Tim Lawless, CoreLogic’s research director has expressed a positive shift with housing values stabilising or rising across most of Australia along with a number of other indicators aligning with the indicated shift.

Auction clearance rates are also holding slightly above the long term average, indicating that sentiment has lifted and home sales are trending around the previous five-year average.

Mr Lawless said it was notable this housing turnaround was occurring despite interest rates remaining elevated.

The last time we saw housing values trending higher through a rising interest rate environment was during the mid-to-late 2000s when the mining boom was underway. This period was also characterised by surging net overseas migration that contributed significantly to housing demand.

Tim Lawless – CoreLogic Research Director

Since seller confidence has increased, a supply of higher quality homes are hitting the market. If you’re looking to own your own home before property prices hit a further historical high, now is the best time to get in touch with our team of experts at Rateseeker and we can help you determine how much you can borrow along with the most suitable loan for your circumstances.

Government commissioned review results in changes for RBA

The Reserve Bank of Australia is facing new changes, following a review commissioned by the federal government.

The review made 51 recommendations, including specific measures to provide clarity, monetary policy framework and stronger monetary policy decision-making.

Treasurer Jim Chalmers stated that the government has agreed in-principle with all 51 recommendations and would work closely with the RBA and parliament to implement them.

Subject to consultations with the opposition, the Treasurer said the government would introduce legislation to:

- Reinforce the independence of the RBA in the operation of monetary policy

- Split the RBA board into two – with one board to oversee monetary policy and the other governance

- Strengthen the RBA’s mandate

- Clarify that Australia’s monetary policy framework will aim for both price stability and full employment

Treasurer Chalmers also stated that the government would institute a more transparent process for appointing external members to the RBA boards.

First home buyers are making their way back into the market

It’s too early to say first home buyers are back, but they’ve certainly made a welcome return to the market, according to recent data from the Australian Bureau of Statistics.

The number of new owner-occupier first home buyer loan commitments jumped 15.8% in March, after dropping to a five-year low in February.

Although numbers show promise, first home buyer activity was 21.8% lower than the year before and 50.5% lower than the January 2021 high.

As property prices currently appear to be rising again, experts urge buyers to consider that now may the right time for first home buyers to enter the market sooner rather than later, before prices rise further. Saving for deposit can be a challenge, however there are two ways to expedite the process.

- Under the First Home Guarantee, the federal government helps eligible first home buyers purchase a property with just a 5% deposit without having to pay lender’s mortgage insurance. Income and price caps apply.

- First home buyers who have parental support can use a guarantor home loan to enter the market with, potentially, a 0% deposit. Again, conditions apply.

If you’re new to the property market and are looking to get your foot in the door before prices get out of control, it may a good time to start getting your finances in order and speaking with a trusted mortgage broker to see where you stand. Get in touch with our mortgage experts, we’ve worked with countless first home buyers to help find out how much they can borrow, guide them through the process and find the most suitable loan for their circumstances.

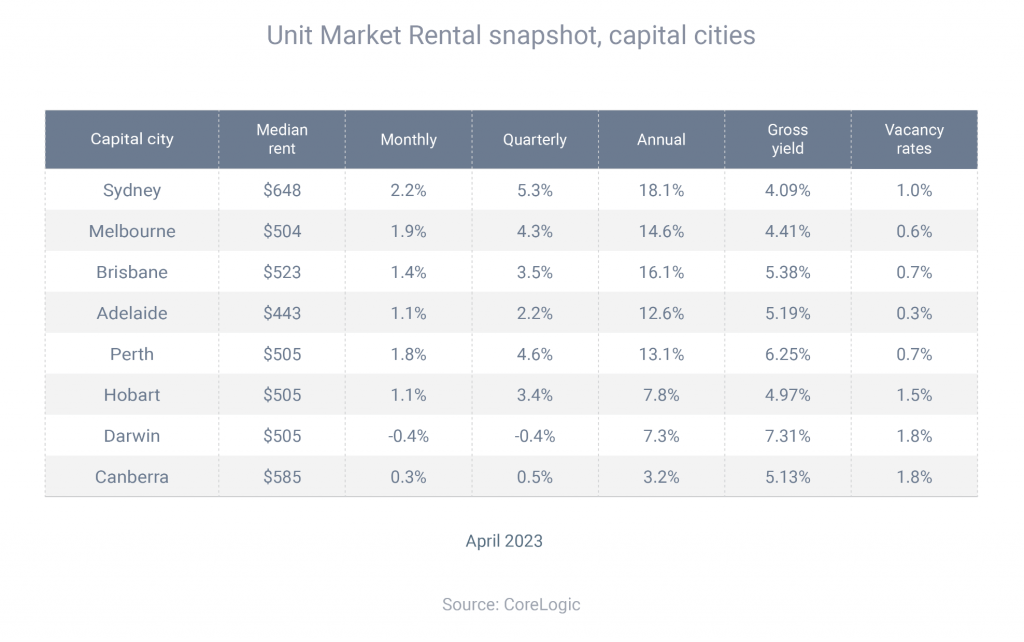

Unit prices and rents on the rise

Whether you are an owner-occupier or an investor, if you own a unit, the property market is pushing in your favour.

After the national median unit price slumped for 10 consecutive months, it took an upwards turn in both March (0.6%) and April (0.7%), according to CoreLogic.

This could signify the start of a slow recovery phase, with inflation seemingly moving past its peak and consumer sentiment rising from near-record lows.

Kaytlin Ezzy – CoreLogic Economist

Meanwhile, unit rents are not only growing at a significant rate (up 14.8% over the year to April), they’re growing much faster than house rents (8.4%).

Ms Ezzy explained that the mismatch between unit rental supply and demand has caused capital city rental growth to reaccelerate, which will be unwelcome news to many tenants already struggling to find affordable rental accommodation.

Although units across each of the capitals and rest-of-state regions still offer a more affordable rental alternative compared to houses, the stronger rental growth seen in the medium to high-density sector, in part due to their relative affordability, has seen the gap narrow.

Since the rental crisis began, this has had a number of Aussie renters in a position where they have decided to purchase instead of rent, with intention the lease out their property when the time comes and step on the other side of the fence.

If you’re tired of increasing rental prices and low supply of decent rental accomodation, it may be time to consider investing your hard-earned dollars towards a property of your own. Need help and don’t know where to start? Get in touch with our expert brokers for an obligation-free chat and we can help get your started.

** General Advice Warning

The information provided on this website is general in nature only and it does not take into account your personal needs or circumstances into consideration. Before acting on any advice, you should consider whether the information is appropriate to your needs and where appropriate, seek professional advice in relation to legal, financial, taxation, mortgage or other advice.