Rateseeker Property News Round-up July – 2024

This month, the Australian residential property market is experiencing some exciting developments, which both homebuyers and investors should keep an eye on. With interest rates fluctuating, shopping around for the best loan deals is more important than ever. Experts advise borrowers to explore various lenders to secure the most favourable terms.

At the same time, the Home Guarantee Scheme has expanded and is providing great opportunities for first-time buyers, especially in regional areas. However, concerns about eligibility and property price caps continue to be a topic of discussion.

Vendor data shows that property sales have been on the rise, with an impressive 94.3% of vendors making a profit. This positive trend reflects the resilience of the market despite variations in regional performances. Additionally, investor borrowing has seen a significant surge of 29.5%, demonstrating renewed confidence and increased activity in the investment sector.

In our July property news update, we dive into the latest news and data crucial for navigating the property market this year.

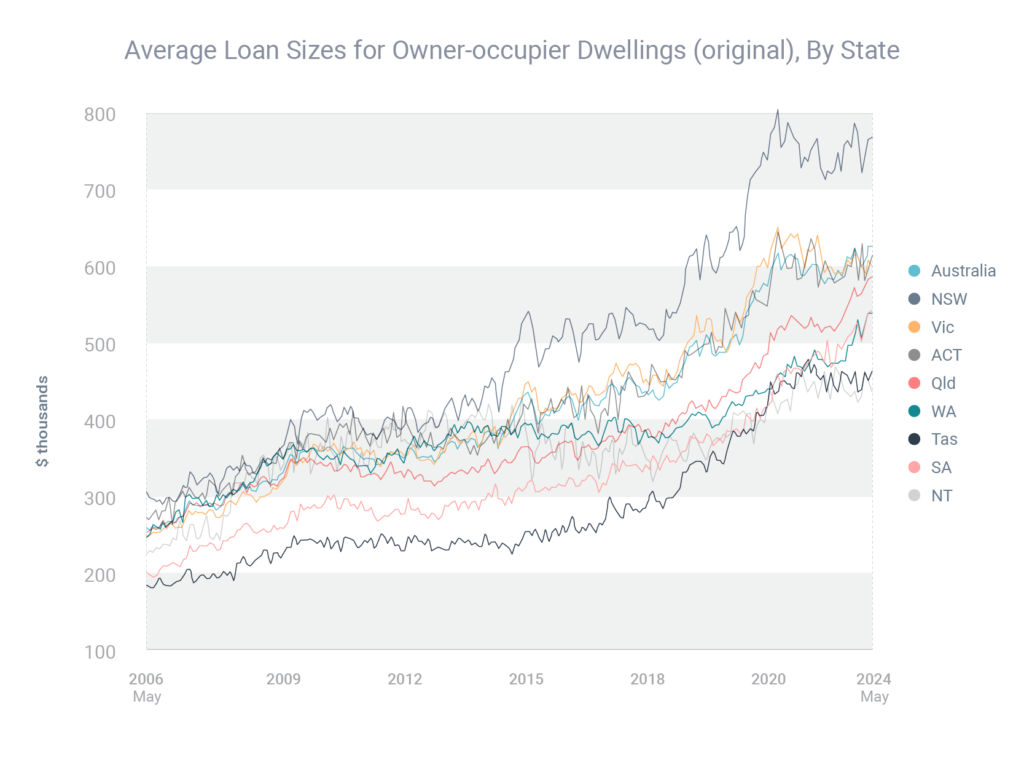

Record-high mortgages demand strategic loan choices

With property prices soaring to record highs, the average mortgage size in Australia has also reached staggering levels, emphasising the critical importance of borrowers shopping around for the right loan.

According to CoreLogic, as of June 2024, the national median property price hit $794,000, reflecting an 8.0% yearly increase. Concurrently, the average owner-occupied loan size surged to $626,055 by the end of May, marking a 7.1% increase from the previous year, as reported by the Australian Bureau of Statistics.

In such a dynamic market, the variance in interest rates and borrowing power across different lenders can be significant. Your financial profile, the type of property, and its location can all influence how much one lender might offer compared to another. Sometimes, the difference could be tens or even hundreds of thousands of dollars.

Navigating these variables on your own can be overwhelming, which is why enlisting the help of a trusted home loan strategist or mortgage broker is a must in 2024.

Need help from an industry expert? Contact our brokers at Rateseeker. We provide detailed knowledge of lender policies and can match you with the lender that best suits your unique needs, potentially saving you substantial amounts in the long run.

Expanded Home Guarantee Scheme in 2024-25: A lifeline for first home buyers and families

In other property news, the federal government has bolstered its commitment to helping Australians enter the property market by allocating an additional 50,000 places to the Home Guarantee Scheme (HGS) for the 2024-25 financial year. This significant expansion includes 35,000 places for the First Home Guarantee. It is designed to support eligible first-time homebuyers by enabling them to purchase a property with as little as a 5% deposit, all without the burden of paying lender’s mortgage insurance (LMI).

Additionally, 10,000 places have been earmarked for the Regional First Home Buyer Guarantee, which offers similar support but specifically targets those purchasing in regional areas. This will make it easier for residents to secure a foothold in their local property markets.

The scheme also introduces 5,000 places for the Family Home Guarantee to assist eligible single parents and legal guardians. This program allows them to purchase a home with just a 2% deposit, free from the need to pay LMI, thereby significantly reducing the upfront costs associated with buying a home.

However, it’s important to note that the HGS comes with strict eligibility criteria. All applicants must be owner-occupiers, with income caps of $125,000 for single applicants and $200,000 for joint applicants. Property price caps also apply and vary across states, reflecting regional market conditions. Furthermore, the HGS is not available through all lenders, adding another layer of complexity for prospective buyers.

If you’re uncertain about your eligibility or how to navigate the scheme, get in touch. We can help guide you through the process and help determine the best course of action.

Houses vs. Units: What 2024 sales trends reveal about vendor profits

According to CoreLogic, the Australian property market continues to deliver solid returns for vendors, with a remarkable 94.3% of all sellers achieving sales above their original purchase prices in the March quarter of 2024.

This marks the fourth consecutive quarterly increase and the highest percentage since 2010, highlighting the robust demand and limited supply driving the market. However, the profitability of property sales varied significantly across different capital cities, reflecting the diverse market conditions across the country.

Further analysis revealed that house owners were more likely to make a profit compared to unit owners, with 97.1% of houses sold at a profit compared to 89.0% of units. This trend exhibits the stronger capital growth typically associated with houses, particularly in sought-after locations.

Additionally, the length of time a property was held before being sold had a significant impact on the profit realised. Vendors who held their properties for up to two years saw a median profit of $82,000, while those who held onto their homes for up to 10 years enjoyed a median profit of $275,000. Those who held their properties for 20 years or more saw even more significant gains, with median profits soaring to $780,000 for a 30-year hold period.

These trends reflect the long-term value of property investment in Australia, particularly for those willing to hold onto their assets through various market cycles. Understanding these dynamics can be key for vendors to time the market effectively and maximise returns.

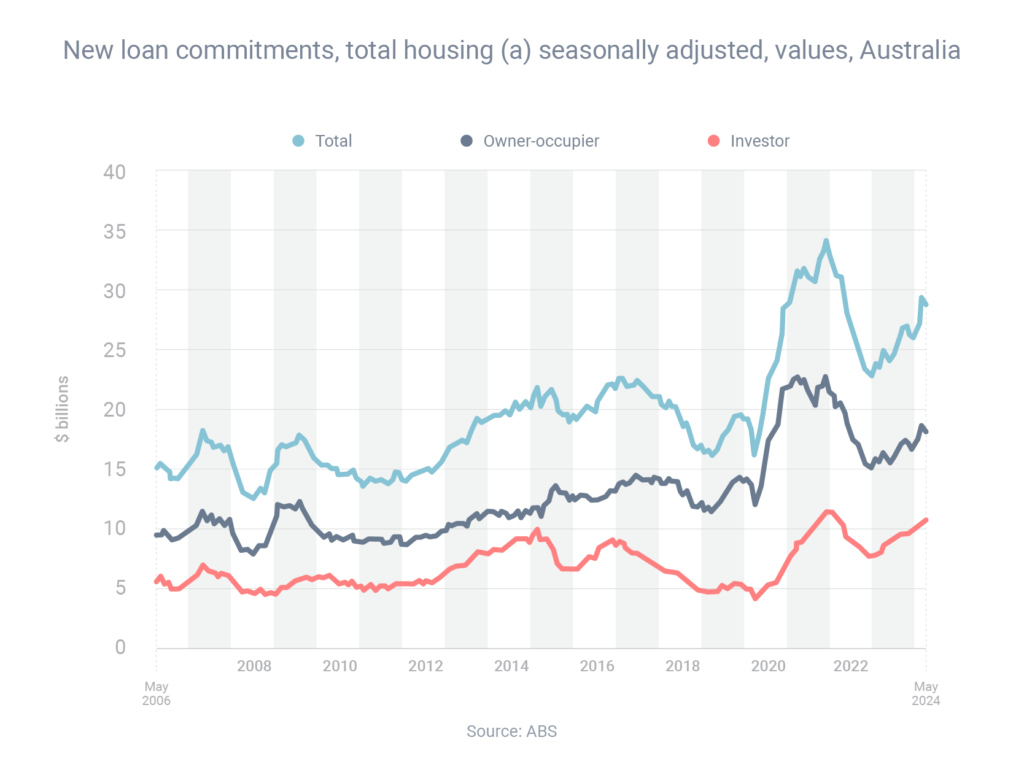

Investor confidence returns as market activity surges

The Aussie home loan market has witnessed a notable surge in activity over the past year, with a significant increase in borrowing volumes, particularly among investors. According to the latest data from the Australian Bureau of Statistics, investors committed to a substantial $10.67 billion in mortgages in May 2024, marking a 29.5% increase compared to the previous year.

This sharp rise indicates renewed confidence among investors in the property market, likely driven by favourable market conditions and opportunities for capital growth.

At the same time, owner-occupier borrowing also saw a healthy rise, with activity increasing by 12.2% to reach an eye-watering $18.13 billion. Investors accounted for 37.1% of all home loans issued in May, slightly above the long-term average of 35.9%, which has been tracked since 2002. This figure highlights the ongoing significance of investor activity in the Australian property market, although it’s worth noting that this percentage is still lower than the peak of 45.9% seen in 2015.

Improving your creditworthiness is essential for those considering entering the property market, whether as an investor or an owner-occupier.

Strategies that can help boost your borrowing power include:

- Reducing discretionary spending to free up funds for loan repayments

- Ensuring all bills are paid on time to maintain a strong credit score

- Consulting with a trusted mortgage broker for expert guidance, lending and property news

Looking for expert home loan advice? We’ve got you covered. At Rateseeker, we can help you start your home-buying journey and ensure you find the best deal suited to your financial situation. Get in touch with our expert home loan strategists at Rateseeker, who will guide you through over 1000+ loan options from 30+ lenders to find the perfect loan for you.

** General Advice Warning

The information provided on this website is general in nature only and it does not take into account your personal needs or circumstances into consideration. Before acting on any advice, you should consider whether the information is appropriate to your needs and where appropriate, seek professional advice in relation to legal, financial, taxation, mortgage or other advice.