Rateseeker Property News Round-up August – 2024

As we bid farewell to August, it’s important to take note of the exciting developments in the Australian residential property market. Big changes are afoot for both renters and homebuyers. The rental market, which has been red-hot for quite some time, is finally starting to cool down. Tenants can breathe a sigh of relief, while property investors might need to rethink their strategies.

Borrowing activity has seen a remarkable surge of 19.1%, indicating a renewed sense of confidence among buyers as they navigate the intricacies of today’s market. At the heart of this borrowing resurgence is the 3% mortgage buffer, a crucial tool that aims to protect borrowers from potential interest rate increases. This buffer remains a pivotal factor in assessing loans.

More Australians are exploring construction loans as a great option for bringing their dream homes to life, especially with construction costs starting to stabilise. It’s crucial for anyone thinking about new construction projects to grasp how these loans operate and how they can be maximised in today’s market.

This month’s blog will explore the latest residential property news providing valuable insights and expert advice to empower you in navigating the dynamic and ever-changing property landscape.

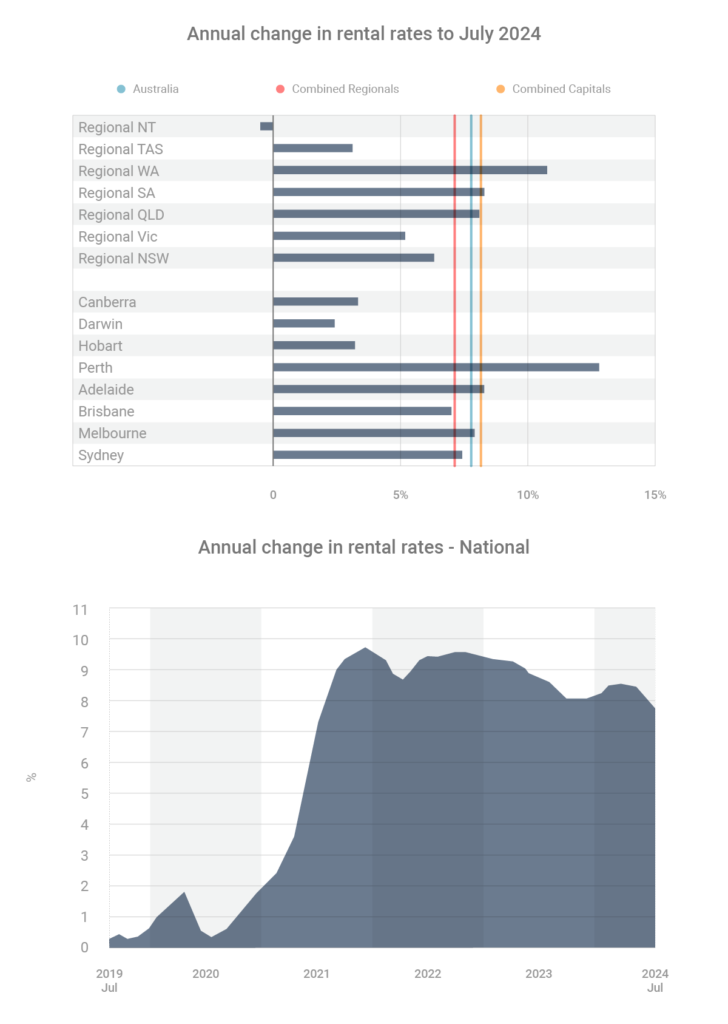

Rents Expected to Keep Growing Despite Slowing in Pace

Over the past five years, property investors have enjoyed substantial gains, with the national median rent increasing by an impressive 39.7%. However, the rental property market showed signs of cooling in July 2024, with rents increasing by just 0.1%—the slowest rate of growth since 2020, according to CoreLogic. This slowdown reflects a broader trend of declining rental growth, particularly in major cities.

Between February and July 2024, annual rental growth in the combined capitals dropped from 9.7% to 8.0%, suggesting that these markets may be reaching their rental affordability limits. In contrast, regional areas, where rental growth has been more modest, saw an increase from 5.4% to 7.1%, indicating some remaining capacity to absorb higher rents.

Despite this slowdown, CoreLogic economist Kaitlyn Ezzy emphasised that rents are still expected to rise, albeit at a slower pace. The persistent issue of low housing supply continues to exert upward pressure on rents, a situation compounded by historically low levels of dwelling approvals and commencements. This shortage of new housing is not a problem with a quick fix, presenting ongoing challenges for policymakers, the property industry, and tenants alike.

Low supply will likely continue to put upward pressure on rents, albeit at a slower pace.

-CoreLogic Economist Kaitlyn Ezzy

With dwelling approvals and commencements at historic lows, providing sufficient new housing will not be a quick fix and remains a genuine challenge for policymakers, the property industry and, of course, tenants.

For investors, this cooling market suggests that while rental income will likely continue to grow, the double-digit increases of previous years may no longer be realistic. Strategic adjustments may be necessary to account for this more tempered rental environment.

Understanding the 3% Serviceability Buffer: What It Means for Borrowers in 2024

When getting a mortgage in Australia, lenders evaluate your capacity to repay based on various factors, such as your ability to manage repayments if interest rates were to go up. To ensure that borrowers can handle potential rate increases, lenders use a “mortgage serviceability buffer.

This buffer is typically set at a minimum of 3.00 percentage points, as mandated by the Australian Prudential Regulation Authority (APRA). For instance, if you apply for a loan with a 6.50% interest rate, the lender will assess your capacity to repay the loan at a rate of 9.50%.

This buffer plays a crucial role in the financial system. Firstly, it acts as a safeguard against lenders offering risky loans that could potentially disrupt the stability of the entire banking system if a large number of borrowers were unable to repay. Secondly, it protects borrowers from the risk of taking on loans that could become too expensive to handle if interest rates were to increase.

The serviceability buffer adds an extra layer of complexity to the mortgage qualification process, but it’s designed to protect the financial system and individual borrowers from potential financial stress in the future.

Activity Surge as Borrowers Take On $29 Billion of Loans

The latest home loan data from the Australian Bureau of Statistics (ABS) highlights three significant trends in the Australian property market as of June 2024.

Borrowing activity in the housing market is experiencing a significant uptick. The total value of home loan commitments has surged to $29.19 billion, marking a 1.3% increase from the previous month and a noteworthy 19.1% rise compared to the previous year.

This substantial growth underscores the increasing confidence of both homebuyers and investors. The favourable market conditions currently at play clearly propel them.

Secondly, investor activity is particularly strong. Investment loans saw a substantial increase of 30.2% year-on-year, totalling $11.02 billion. This surge far outpaces the 13.2% increase in owner-occupied loans, which rose to $18.17 billion.

The significant uptick in investment loans underscores the appeal of property investment in the current economic environment, as investors capitalise on opportunities for capital growth and rental income.

Finally, while refinancing activity remains elevated, it has cooled from the record levels observed in mid-2023. In June 2024, borrowers refinanced $15.79 billion worth of loans, a 20.9% decrease compared to last year. This decline suggests that the peak of the refinancing boom may have passed, possibly due to rising interest rates and changing market dynamics.

Building Your Dream Home and Navigating Construction Loans

Are you thinking about building your dream home? Constructing your own home gives you the freedom to customise every detail exactly the way you want. Here’s how to make it happen:

- Share your vision with a mortgage broker to create a finance plan that fits your budget and timeline.

- Then, it’s time to purchase the perfect piece of land, find the right block for your future home, this may take time.

- Speak with a trusted architect to design your dream home,

- Use a trusted builder to plan each building stage

- Then, obtain all the necessary permits and approvals

- And finally, watch your vision come to life as your dream home is built.

Unlike traditional home loans, where the funds are disbursed in one lump sum, construction loans work differently. The loan is released in five stages corresponding to the progress of your build, and you only pay interest on the funds that have been drawn down so far. Once construction is complete, your loan typically converts to a standard principal-and-interest mortgage.

Building your own home is an exciting prospect, but it’s important to be aware of the rising costs associated with construction. According to the ABS, the annual growth rate in house-building costs increased from 3.9% in September 2023 to 4.3% in June 2024.

With costs on the rise, it’s crucial to start your build sooner rather than later to potentially save money in the long run. If building your dream home is something you’ve been considering, now is the perfect time to chat with our loan strategists at Rateseeker and explore your options and secure financing. Don’t miss out on the opportunity to make your dream home a reality!

** General Advice Warning

The information provided on this website is general in nature only and it does not take into account your personal needs or circumstances into consideration. Before acting on any advice, you should consider whether the information is appropriate to your needs and where appropriate, seek professional advice in relation to legal, financial, taxation, mortgage or other advice.