How to pay your mortgage off faster

A home is a significant purchase, and the biggest debt that most people will take on in their lifetime.

The average home loan term is between 25 and 30 years, which means you’ll spend a good portion of time repaying your mortgage.

Paying off your mortgage faster can save you thousands, and bring you one step closer to financial freedom. If you want to get ahead on your repayments, these 6 tips will help.

Why should you pay your mortgage off faster?

While shaving a few years off your mortgage might not seem like a big deal now, it can actually save you a significant amount in the long run.

Paying off your mortgage faster reduces the amount of interest you pay over the lifetime of your loan, which can add up to tens of thousands.

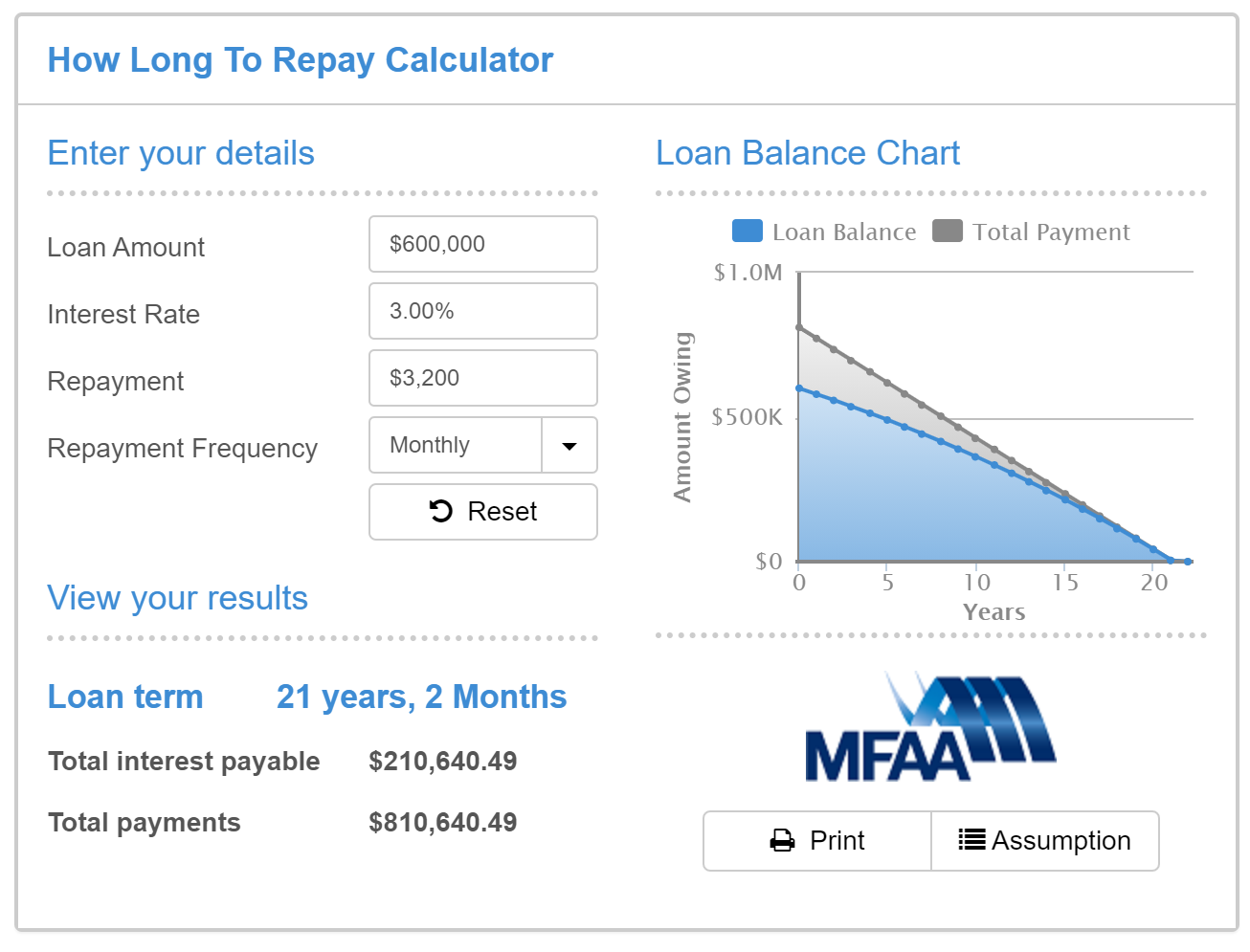

These two examples from our How Long to Repay calculator illustrate how long it takes to repay your home loan, depending on whether you make extra repayments.

Example 1

You have a home loan of $600,000 with an interest rate of 3.0%, and are making monthly repayments of $3,000. Based on these numbers, it will take you roughly 23 years and 2 months to pay off your loan and you’ll end up paying $232,815.90 in interest.

Example 2

You have a home loan of $600,000 with an interest rate of 3.0%, and are making monthly repayments of $3,200. Based on these numbers, it will take you roughly 21 years and 2 months to pay off your loan and you’ll end up paying $210,640.49 in interest — saving you $22,175.41 in the long run.

On top of this, paying your mortgage off faster also:

- Frees up a large sum of money every month in the future for travel, investments or retirement

- Protects you against any future interest rate increases

- Takes a massive financial weight off your shoulders

It’s worth noting, however, that making additional repayments may not always make sense. For example, if you’re on a fixed-rate home loan, making extra repayments above the minimum repayment amount may end up costing you in break fees. Learn more here.

It’s best to consult with your mortgage broker or lender before making the switch.

6 tips to pay off your mortgage faster

1. Focus on making bigger repayments in the early part of your loan

If you have to choose a time to make extra repayments, it’s best to do it in the early part of your loan (i.e. the first 5 or 10 years). The principal on your loan is at its largest at this stage and, given interest is calculated based on the principal, you’ll end up paying more interest during this period.

Make extra repayments early on if possible, and opt for principal and interest repayments. This will decrease the principal amount on your loan and reduce the amount of interest charged over time.

2. Switch to fortnightly or weekly repayments

Paying $1,500 every fortnight or $750 every week might seem like the same thing as paying $3,000 every month. However, this little trick can have a significant impact on your mortgage repayments and help you pay your loan off faster.

There are two reasons for this:

- You’ll make the equivalent of an extra month’s repayment each year, as each year has 26 fortnights and 52 weeks, compared to 12 months.

- You’ll pay less interest, as interest on your principal is calculated daily.

Using the example from earlier of a $600,000 home loan, here’s a breakdown of how making weekly or fortnightly repayments can affect your loan term and your total repayment amount:

| Monthly payment of $3,000 | Fortnightly payment of $1,500 | Weekly payment of $750 | |

| Loan term | 23 years 2 months | 20 years 17 fortnights | 20 years 34 weeks |

| Total interest payable | $232,815.90 | $205,215.16 | $204,983.09 |

| Total payments | $832,815.90 | $805,215.16 | $804,983.09 |

In this example above, the simple act of switching from monthly to fortnightly payments shaves approximately 2 years and 4 months off your loan and will save you $27,600.74. Likewise, switching to weekly repayments will also help you pay your loan off faster, and save you $27,832.81.

Want to find out how much you could save by switching to fortnightly payments? Use our How Long to Repay calculator.

3. Use your offset account or redraw facility

Some home loans offer an offset account feature or redraw facility, which can reduce the amount that you pay in interest throughout the duration of your mortgage.

An offset account is a savings or transaction account that effectively ‘offsets’ the amount that you owe on your mortgage. For example, if you have a $600,000 mortgage with a 25-year loan term and you have $50,000 in your offset account, this means you’ll only be charged interest on $550,000.

Use our home loan offset calculator to see how much an offset account could save you.

A redraw facility allows you to make extra repayments on your mortgage, which you can then draw upon in the future if you need it. Like an offset account, a redraw facility can reduce the amount of interest paid on your home loan.

4. Take advantage of interest rates

Interest rates influence the total amount you end up paying over the lifetime of your loan, and learning to work with them can help pay off your mortgage faster.

Let’s say interest rates are low. Rather than reduce your repayments, it’s the perfect time to pay off as much as you can on the principal amount, in order to reduce the amount you pay in interest in the future. On the other hand, if interest rates have increased and you have a split loan, focus on paying off the fixed-rate portion during this time.

5. Make extra repayments, even if they seem insignificant

An extra $100 every month doesn’t sound like a lot, especially when compared to a $600,000 home loan. However, making this seemingly small contribution every month will save 11 months and $8,421.55 in interest over the course of your loan.

Every little bit counts. Work out how much you can save on interest with our extra repayment calculator.

6. Refinance your mortgage

Refinancing your mortgage is a great way to take advantage of a lower home loan interest rate, free up equity, consolidate your debts, and benefit from additional home loan features, such as an offset account.

Bear in mind that refinancing does come with some additional costs, which should be considered when deciding whether to refinance. Learn more about refinancing your home loan here, or speak to one of our brokers to see if refinancing is the best option for you.

Ready to pay your mortgage off faster?

Talk to the team at Rateseeker today. Our expert brokers can help you with tailored advice and tips on how you can save money on your home loan, and find the best home loan option for you. Get in touch with us for an obligation-free consultation now.

** General Advice Warning

The information provided on this website is general in nature only and it does not take into account your personal needs or circumstances into consideration. Before acting on any advice, you should consider whether the information is appropriate to your needs and where appropriate, seek professional advice in relation to legal, financial, taxation, mortgage or other advice.