NSW stamp duty reform: what the proposed changes mean for homeowners and buyers

Earlier this week, NSW State Treasurer Dominic Perrottet proposed one of the biggest changes to the way Australians have been taxed on property.

Under Perrottet’s proposed plan, stamp duty will be replaced with an annual tax based on the value of their land. While these changes have to be implemented, homeowners and buyers are already wondering how the NSW stamp duty changes would affect them — and whether they’ll be better off in the long run.

In this post, we explore what the proposed changes are, and what the new land tax would mean if you already own a home or are looking to buy one in the future.

Note: these are proposed changes only. The NSW Government will be getting community feedback over the coming months before moving forward with its planned proposal. Stay tuned for the latest updates on the stamp duty tax, property news, buying and refinancing advice and more.

What is stamp duty?

Stamp duty is a state tax on the sale of property in Australia. It covers the costs of changing the title of the property and ownership details which is usually paid by the buyer.

The amount of stamp duty you pay differs depending on:

- Your state or territory. Some states, such as VIC, charge more stamp duty than others.

- Purchase price of the property. Stamp duty is calculated on a sliding scale. The higher the purchase price of your property, the higher the stamp duty you pay.

- The type of property that you are purchasing. Stamp duty on an investment property will typically be higher than stamp duty on an owner-occupied property.

Earlier this year, the NSW Government abolished stamp duty for first home buyers purchasing new homes under $800,000. This stamp duty relief measure commenced on 1 August 2020 and will last for a 12-month period.

Why is the NSW Government proposing these changes?

The COVID-19 pandemic has devastated the Australian economy, and the property industry is no exception.

To cope with the economic downturn, state governments are trying to find ways to reduce unemployment, return to growth, repair their budgets in the long-term, and reduce the net debt created in the wake of the pandemic.

The proposed changes would remove a significant barrier to purchase for many buyers, as the average stamp duty cost in NSW is around $26,000. This cost can be a massive deterrent that discourages people from moving home, downsizing their property or purchasing additional investment homes.

The NSW government hopes that by abolishing stamp duty, the state will benefit from long-term economic gains, including more spending, increased economic growth and investment, and more property sales.

“This is a vision for every person and family in NSW – from first home buyers trying to get a foot on the property ladder, to frontline workers moving to service our regional communities, and retirees who are ready to downsize…Reform of the inefficient stamp duty system could also create and support thousands of jobs to boost the economy and kickstart our recovery for a prosperous, post-pandemic NSW.”

Dom Perrottet

How would the proposed annual land tax work?

Currently, stamp duty is calculated on a sliding scale depending on the purchase price of your property.

Under the proposed changes, buyers can either choose to:

- pay a one-off stamp duty bill when purchasing a property, or

- pay an annual tax based on the value of their land. This fee would need to be paid every year for the entire duration that they own the home.

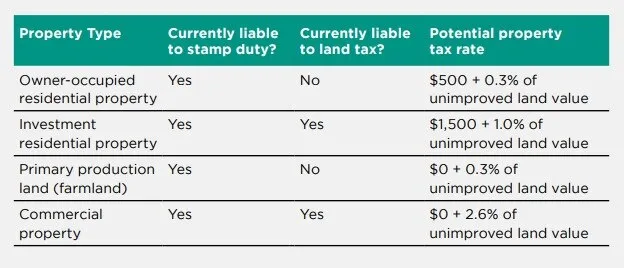

The NSW Treasury has also released a table of potential property tax rates under the new model:

Source: NSW Treasury

In addition to the annual land tax, Perrottet has introduced an additional incentive for first-time buyers — particularly after the stamp duty relief period ends.

As part of his proposed overhaul, first home buyers would get a grant worth up to $25,000 instead of an exemption from stamp duty. This can be used to purchase new items for the home, such as furniture or white goods.

What about existing homeowners?

As it currently stands, the proposed changes would only apply to future purchases on a home. This means that if you are an existing homeowner and have already paid stamp duty on your property, there is no change.

When will we know more?

The details have yet to be ironed out, but the NSW Government has said it will work with the community to get feedback on the changes before moving forward with the proposal.

The earliest that the proposed changes would kick in would be in the second half of 2021, in line with the new Federal Budget and the start of the 2021-22 Financial Year.

“The NSW Government will work with people and communities to shape any reform over the coming months to ensure it is tailor-made for the current and future needs of our state.”

– Dom Perrottet

Amidst these proposed changes, it’s more important than ever to work with a mortgage broker when buying or refinancing a property.

The expert brokers Rateseeker team is here to advise you on the best step for your personal and financial situation. Contact us today for an obligation-free consultation.

** General Advice Warning

The information provided on this website is general in nature only and it does not take into account your personal needs or circumstances into consideration. Before acting on any advice, you should consider whether the information is appropriate to your needs and where appropriate, seek professional advice in relation to legal, financial, taxation, mortgage or other advice.