June 2026 Property Market Update: What Today’s Changing Market Means for Australian Buyers

The Australian property market continues to evolve, and June has brought another wave of developments that are worth paying attention to. While much of the recent discussion has focused on the Reserve Bank and interest rates, several other trends are quietly influencing how Australians buy, build and finance property.

For many prospective buyers, affordability remains the biggest challenge. Yet at the same time, new government initiatives are making it easier for eligible Australians to enter the market sooner. Builders are seeing demand remain steady despite higher borrowing costs, more Australians are embracing electric vehicles, and the housing market is beginning to offer buyers something they have not enjoyed for quite some time: more choice.

As always, market headlines only tell part of the story. The real question is how these developments affect your own plans, whether you are purchasing your first home, upgrading, investing or simply reviewing your finances.

Let’s take a closer look at four of the biggest property and finance stories shaping the Australian market this month.

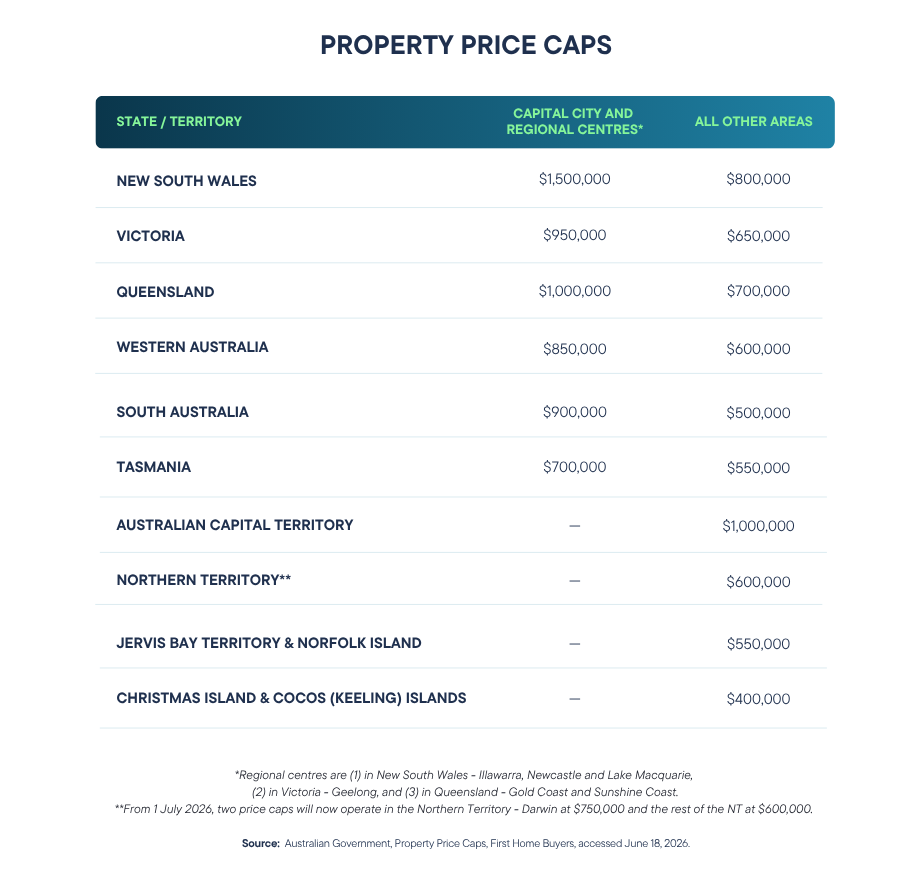

The 5% Deposit Scheme Continues to Change the Way Australians Buy Their First Home

Saving a 20% deposit has traditionally been one of the biggest obstacles for first-home buyers.

For many Australians, it can take years of disciplined saving while property prices continue rising around them. During that time, buyers often find themselves chasing a moving target, with higher prices requiring even larger deposits.

That is why the expansion of the Australian Government’s 5% Deposit Scheme has attracted so much attention since it was broadened in October 2025.

Recent figures from Equifax demonstrate just how significant the change has been.

Between October 2025 and March 2026, participating lenders experienced a 16.4% increase in loan volumes, while lenders not participating in the scheme saw demand fall by 6.5% over the same period.

Perhaps even more telling is the rise in enquiries from younger Australians.

Borrower enquiries increased by:

- 22.8% among buyers aged 18 to 25

- 17.4% among buyers aged 26 to 35

These numbers suggest that many younger Australians who previously believed home ownership was years away are now actively exploring their options.

Why the Scheme Has Become So Popular

Under normal lending rules, buyers contributing less than a 20% deposit are generally required to pay Lenders Mortgage Insurance (LMI).

LMI protects the lender, not the borrower, and depending on the loan size, can add many thousands of dollars to the upfront cost of buying a home.

The 5% Deposit Scheme changes that equation.

Eligible buyers can purchase a property with as little as a 5% deposit while avoiding LMI because the Australian Government guarantees part of the loan.

For many households, this removes one of the largest financial hurdles associated with entering the market.

Rather than spending several additional years saving a larger deposit, buyers may be able to purchase much sooner.

Buyers Are Becoming More Flexible

One particularly interesting finding from Equifax is that affordability is reshaping where Australians choose to buy.

According to the research, 81.9% of first home buyers purchased outside their existing suburb.

This reflects an important shift in buyer behaviour.

Rather than focusing only on familiar locations, many buyers are broadening their search to neighbouring suburbs, outer metropolitan areas and regional centres where their budget stretches further.

This approach can create opportunities that simply may not exist closer to city centres.

It also highlights an important lesson for today’s buyers.

Sometimes the quickest path into the property market is not waiting for prices to fall. Instead, it involves adjusting expectations about location while keeping long-term goals in mind.

A Smaller Deposit Is Not Always the Cheapest Option

Although entering the market sooner has obvious advantages, buyers should also understand the trade-offs involved.

A smaller deposit generally means:

- Borrowing a larger loan amount.

- Paying more interest over the life of the loan.

- Starting with less equity in the property.

That does not necessarily make it the wrong decision.

For many buyers, entering the market earlier allows them to benefit from future property growth while avoiding years of rising rents.

However, every situation is different.

The right decision depends on your income, long-term plans, repayment comfort and financial goals.

Before relying on any government support scheme, it is important to understand the eligibility requirements, participating lenders and the most suitable loan structure for your circumstances.

Building a Home Remains an Attractive Option

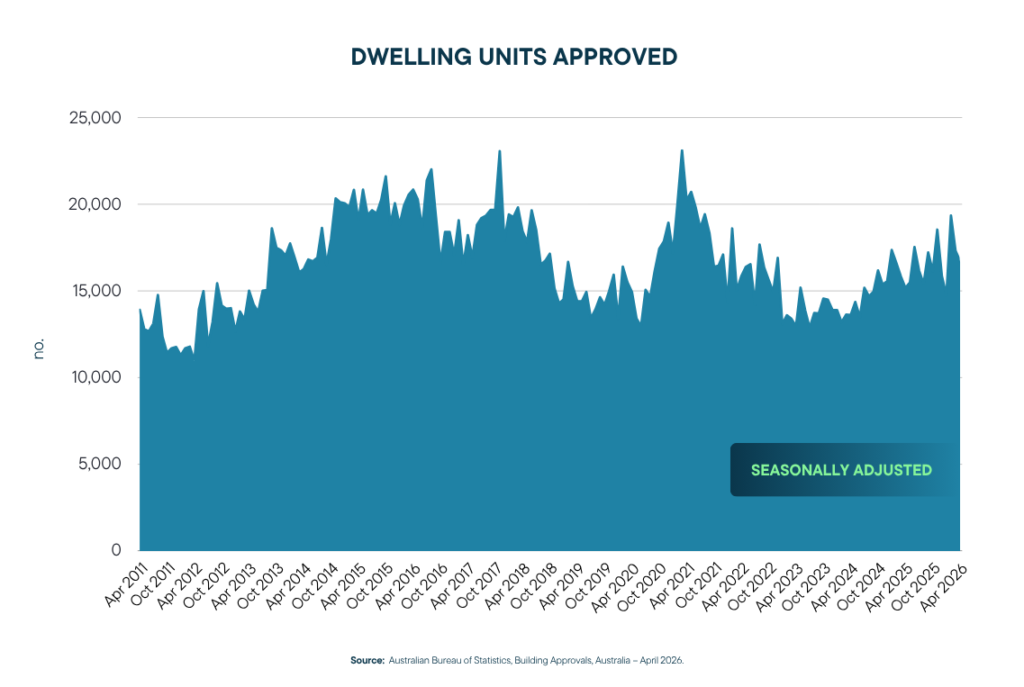

Despite higher interest rates, many Australians continue choosing to build rather than buy an established home.

Recent Australian Bureau of Statistics figures show that 200,424 homebuilding approvals were issued during the year to April.

That represents an 8.5% increase compared with the previous twelve-month period.

While this is encouraging news for the construction sector, it is still below the pace required to meet Australia’s National Housing Accord target of delivering an average of 240,000 new homes each year through to mid-2029.

In other words, Australia continues to face a housing supply challenge.

That ongoing shortage is one reason property prices have remained relatively resilient despite changing economic conditions.

Why Buyers Continue Choosing New Builds

Building offers several potential advantages.

Many buyers appreciate the opportunity to customise floor plans, finishes and layouts that better suit their lifestyle.

New homes also tend to deliver greater energy efficiency, lower maintenance costs during the early years and access to newer building standards and technologies.

Depending on where you build, government grants, concessions or incentives may also help reduce upfront costs.

For some buyers, particularly those struggling to compete in established suburbs, building represents a practical alternative.

Construction Finance Works Differently

One area that often surprises first-time builders is how construction loans operate.

Unlike a standard mortgage, construction finance does not provide the full loan amount upfront.

Instead, funds are progressively released throughout the build as each stage is completed.

Typical payment stages include:

- Foundation or slab.

- Frame.

- Lock-up.

- Fit-out.

- Completion.

This staged payment system helps ensure builders receive funds only as work progresses.

During construction, borrowers generally make interest-only repayments based only on the funds that have been drawn down.

That can make repayments more manageable while construction is underway.

However, construction loans also introduce additional considerations that buyers should prepare for.

Building delays, weather interruptions, material shortages and contract variations can all affect timelines and costs.

Having a financial buffer available becomes especially important during the construction process.

Planning Before Signing Can Save Stress Later

One of the biggest mistakes buyers make is selecting a builder before understanding their borrowing capacity.

Construction finance involves additional documentation, lender requirements and approval processes compared with purchasing an existing property.

Taking the time to organise finance early allows buyers to compare loan options, understand repayment stages and build realistic contingency plans before construction begins.

With demand for new housing continuing to grow, careful planning remains one of the best ways to keep a building project on track.

Electric Vehicles Continue Their Rapid Rise Across Australia

The way Australians think about transport is changing just as quickly as the way they think about property.

For years, electric vehicles (EVs) were viewed as a niche purchase, often associated with early adopters or environmentally conscious drivers. Today, they are becoming a genuine mainstream option, with more Australians considering them alongside traditional petrol and diesel vehicles.

Recent VFACTS data highlights just how quickly the market is evolving.

In May 2026:

- Battery electric vehicles accounted for 20% of all new vehicle sales.

- When hybrids and plug-in hybrids are included, electrified vehicles represented 46% of all new vehicles sold.

That is the highest share ever recorded in Australia.

This rapid growth reflects several factors coming together at once. Consumers now have far more vehicle choices than they did only a few years ago, charging infrastructure continues to improve, fuel prices remain unpredictable and various government incentives have encouraged more households to consider making the switch.

For many Australians, purchasing a vehicle has become one of the biggest financial decisions outside buying a home. That means understanding the long-term cost of ownership is becoming increasingly important.

Looking Beyond the Purchase Price

One of the biggest misconceptions surrounding electric vehicles is that they are simply too expensive.

While it is true that many EVs still carry a higher upfront purchase price than comparable petrol vehicles, that only tells part of the story.

Running costs are often considerably lower.

Owners typically spend less on fuel, servicing and ongoing maintenance because electric vehicles have fewer moving parts than traditional internal combustion engines.

Depending on how often you drive and how long you intend to keep the vehicle, those savings can become significant over time.

On the other hand, a conventional petrol or diesel vehicle may still make more financial sense for buyers who drive infrequently, live in areas with limited charging infrastructure or prefer a lower upfront purchase cost.

There is no universal answer.

Instead, the right choice depends on your own circumstances.

Questions Worth Asking Before Buying

Before deciding whether an electric vehicle is right for your household, it helps to think beyond the showroom.

Some useful questions include:

- Does the purchase comfortably fit within your overall budget?

- Do you have convenient access to charging at home or nearby?

- Approximately how many kilometres do you drive each year?

- What are the expected servicing and maintenance costs?

- How important is future resale value?

These considerations matter because a vehicle purchase should support your broader financial goals rather than compete with them.

If you are planning to buy a home, refinance or invest in property, taking on additional vehicle debt may influence your borrowing capacity.

Likewise, choosing a vehicle with lower ongoing running costs may help improve your monthly cash flow, freeing up money that could instead be directed towards your mortgage, savings or investment plans.

Finance should always be considered as part of the bigger financial picture.

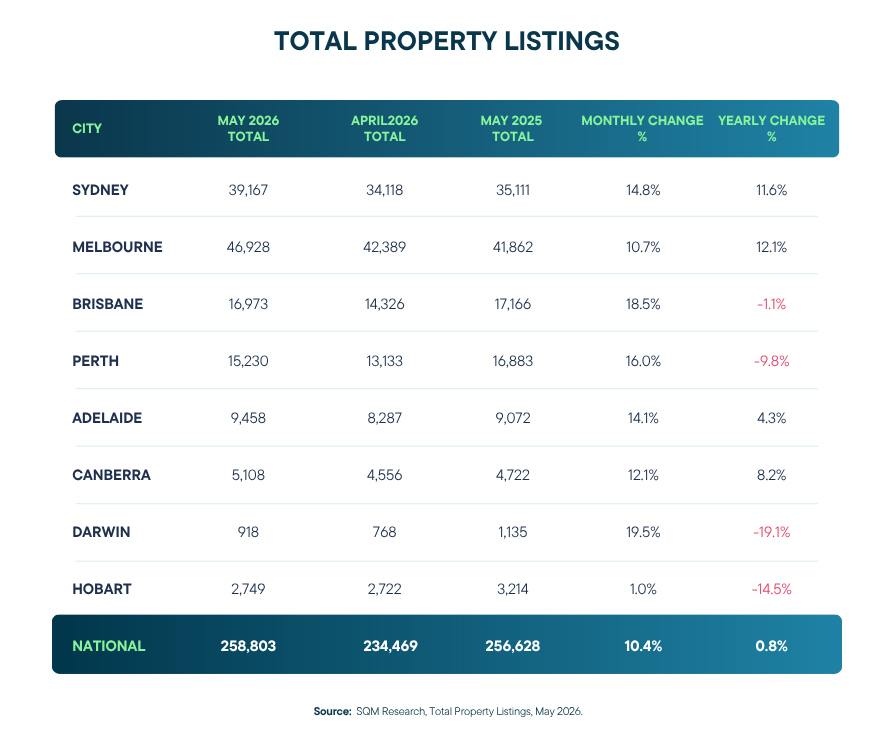

Buyers Are Finally Seeing More Choice in the Property Market

After several years of intense competition, Australia’s housing market is beginning to show signs of offering buyers more breathing room.

According to SQM Research, total residential listings increased by 10.4% during May, compared with April.

New listings rose by 5.0%, while older listings increased by 10.5%.

At first glance, this may simply appear to mean there are more homes available for sale.

However, the reasons behind the increase tell a more interesting story.

Many properties are now taking longer to sell.

Higher interest rates, stretched affordability, ongoing global economic uncertainty and softer consumer confidence have all made buyers more selective than they were during the rapid property boom.

Rather than rushing into purchases, many buyers are taking additional time to compare properties, organise finance and negotiate more carefully.

What This Means for Buyers

For buyers, this shift creates several welcome advantages.

More listings generally mean:

- Greater property choice.

- Less pressure to make rushed decisions.

- More opportunities to negotiate.

- Reduced competition at some inspections and auctions.

This does not necessarily mean buyers suddenly hold all the power.

Well-presented properties in highly desirable locations continue to attract strong demand.

However, buyers who are financially prepared may find they now have greater flexibility than they did over the past few years.

Instead of competing against dozens of offers, they may have more time to complete inspections, seek professional advice and negotiate favourable contract conditions.

That can lead to better long-term purchasing decisions.

Sellers Face a Different Market

While buyers benefit from increased choice, sellers need to adjust their expectations.

A larger number of available properties naturally creates more competition.

Homes that might have sold within days during previous years may now require longer marketing campaigns.

Pricing accurately has become increasingly important.

Buyers have more alternatives available, making it harder for overpriced properties to attract strong interest.

Presentation, marketing quality and realistic expectations now play a bigger role in achieving successful sales.

A Cooling Market Is Not a Collapsing Market

One important distinction is worth remembering.

More listings do not automatically mean property prices are about to fall dramatically.

Current conditions simply reflect a healthier balance between supply and demand.

Property values remain significantly higher than they were before the pandemic, and market performance continues to vary widely between suburbs, cities and regional locations.

Some areas continue recording solid price growth, while others have become more balanced.

This is why relying on national headlines alone rarely provides the full picture.

Property remains a highly local market.

Understanding what is happening in your target suburb often matters far more than broad national averages.

What These Trends Mean for Your Next Property Decision

Looking across all four stories, one theme becomes clear.

Today’s market is offering more opportunities, but those opportunities favour buyers who are well prepared.

Government support schemes are helping more Australians enter the market earlier.

Construction continues attracting buyers looking for greater choice and flexibility.

Households are making smarter long-term financial decisions about major purchases like vehicles.

And a growing number of property listings is giving buyers more options than they have enjoyed for some time.

None of these developments removes the importance of careful planning.

Buying with a smaller deposit still requires a realistic repayment strategy.

Building a home still demands a clear understanding of construction finance.

Vehicle purchases still need to fit comfortably within your broader financial goals.

More listings still require buyers to know exactly what they can afford before making an offer.

In many ways, preparation has become even more valuable than timing.

Markets will always move.

Interest rates will continue changing.

Government policies will evolve.

Property prices will rise in some areas while slowing in others.

The buyers who consistently make confident decisions are usually those who understand their finances well before they begin searching.

Knowing your borrowing capacity, comparing lenders carefully and choosing the right loan structure can often make a far bigger difference than trying to perfectly predict the market’s next move.

Final Thoughts

June’s property market update highlights just how quickly Australia’s lending and housing landscape continues to evolve.

The expanded 5% Deposit Scheme is helping many first-home buyers bring their plans forward. Construction remains an attractive pathway despite ongoing supply challenges. Electric vehicles are becoming an increasingly common financial consideration for Australian households. And buyers are finally seeing more choice as property listings increase across the country.

While each of these stories reflects different parts of the market, they all reinforce the same message.

Good financial decisions start with understanding your own situation.

Whether you are buying your first home, building, upgrading, refinancing or investing, having the right finance structure in place gives you greater confidence to act when opportunities arise.

Conditions will continue changing throughout the year, but careful planning remains one advantage that never goes out of style.

Ready to Take the Next Step?

Whether you’re buying your first home, planning a build, refinancing or simply reviewing your options, RateSeeker can help you understand your borrowing power, compare lenders and find a loan that suits your goals. Get in touch today, and let’s make your next property decision with confidence.

** General Advice Warning

The information provided on this website is general in nature only and it does not take into account your personal needs or circumstances into consideration. Before acting on any advice, you should consider whether the information is appropriate to your needs and where appropriate, seek professional advice in relation to legal, financial, taxation, mortgage or other advice.