Housing affordability and how it can impact your home goals.

Despite the slump in property market, housing affordability has barely improved, although a select number of affluent areas are the exceptions, new data reveals.

House prices are still tear-inducing in many neighbourhoods, and regional Aussie home buyers / home owners and renters are still copping the hardest of the recent property boom.

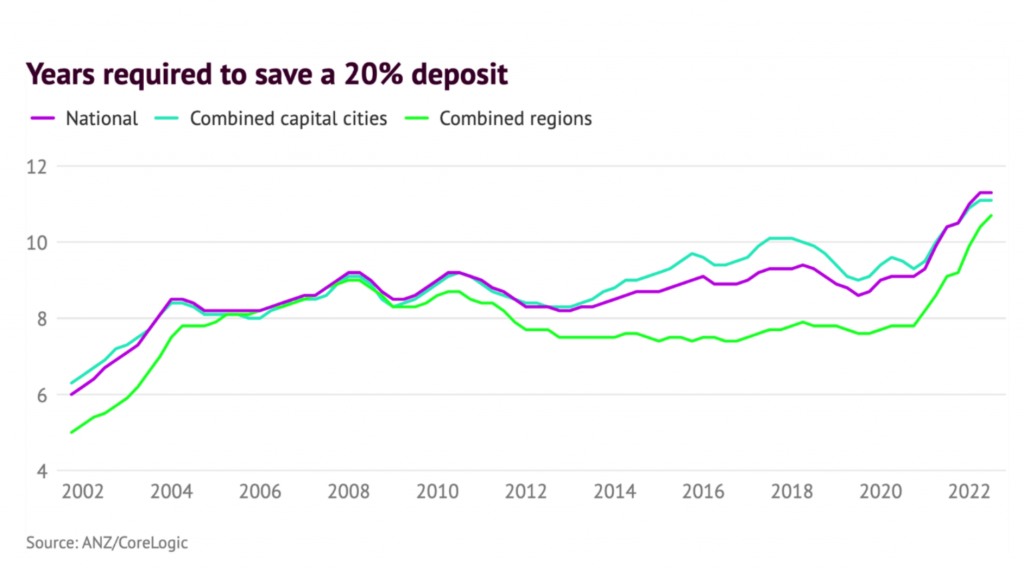

How many years will I need to save for a deposit?

The latest ANZ and CoreLogic report reveals that one of the primary obstacles for homebuyers, mainly the time it takes to save for a deposit, has across our capital cities , the figure fell 11 days to 11.11 years in the three months leading up to June.

This decrease is marginal due to price falls having been relatively modest so far in comparison to previous gains, although the data and economists predict that these slumps will continue to proliferate and reach wider areas.

The deposit issue faced by regional Australians has almost caught up with their capital city counterparts after two years of pandemic sea-changes skyrocketing the value of country homes.

Did you know it takes on average 10.7 years to save for a deposit in the regions as of the June quarter, up from 10.4 years three months earlier?

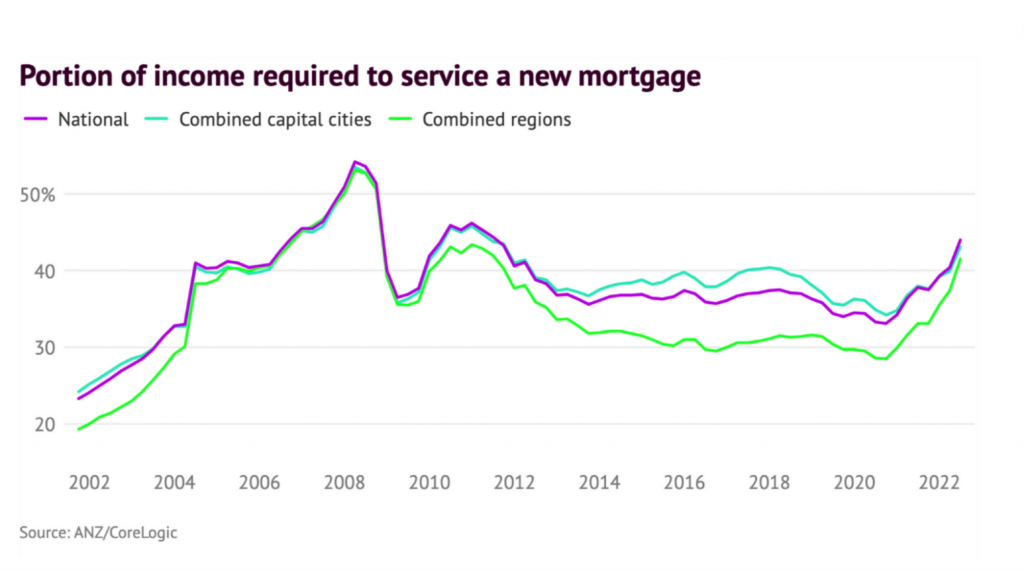

Property owners who have purchased in the recent months will also face a new affordability obstacle in the form of rapidly rising mortgage repayments as the RBA looks to tackle the inflation within the economy. There’s no wonder why mortgage serviceability has reached its worst level in the last 10 years.

Recent reports reveal that these days, households are spending up to 44% of their income on simply repaying their home loan. This is the highest level seen since June 2011, jumping from 40.4% in the previous three months.

And what about rental tenants?

While buyers face certain challenges, the nation’s renters face their own hurdles as affordability has crushed budgets for the typical tenant who forks over 30.9 per cent of their pay check towards rent in the June quarter up from 30.3 per cent in the previous comparison period.

Even less affordable in regional Australia, renting has tenants spending up to 34 per cent of their income on a new lease compared with 28.4 per cent spent by their fellow city renters.

Although we’re starting to see a drop in prices across the capital cities, home values are still absurdly high compared to many Aussie household incomes. Data reveals that the median home value is approximately 8.3 times what your household income is, however this has come down from 8.4 in the last 3 months.

Felicity Emmett, ANZ senior economist believes that house prices would need to see a fall of greater than 25 per cent to come close to seeing a broad improvement in many of these housing affordability measures, which at this stage is an unlikely scenario.

“Even though we might see some marginal improvement in some of these measures, the underlying problems around housing affordability aren’t going to be fixed by a correction of 15 per cent or so in national house prices, not from a perspective of mortgage serviceability,”

You’d need a decline of more than 25 per cent to offset the higher interest rates impact on mortgage serviceability.

Felicity Emmett- ANZ Senior Economist

What if I’ve got decent savings?

But what if you’re a homeowner with strong savings and high household incomes? If you’re thinking about looking to buy homes in lifestyle and coastal regions, you may be the biggest winners of the downturn, as years are already trimmed off the deposit hurdle in some of the most higher priced pockets of Sydney and Melbourne.

Perhaps it’s time for a sea-change or a tree-change?

Emmett indicated that the 15 per cent fall forecast might be a marked improvement in the deposit hurdles for some.

Some of the lifestyle coastal regions, we’re seeing quite significant improvement in the deposit hurdle,”

Some of the lifestyle coastal regions, we’re seeing quite significant improvement in the deposit hurdle.

felicity emmet – Anz senior economist

Experts said while there was a trade-off between falling property prices and rising interest rates, some home buyers on the hunt and are ready to buy, could find themselves in a beneficial position.

Head of Australian Research at Core Logic – Eliza Owen claimed that here is a trade-off in the places where the deposit hurdle has come down in the face of higher mortgage costs and higher rents. Buyers that had a 20 per cent saving levels before prices started to decline it might mean they will have more of a deposit.

Those really feeling the pinch are renters who are trying to save for their home deposits, whilst facing higher rental prices it can be a steep challenge.

Looking to buying a home?

Seek the sharpest home loan rates on the market with Rateseeker. We’ll guide you through every step of the mortgage application process and help you lock in the best deal for your home loan. Get started with our free home loan comparison tool or contact us to claim your free consultation.

** General Advice Warning

The information provided on this website is general in nature only and it does not take into account your personal needs or circumstances into consideration. Before acting on any advice, you should consider whether the information is appropriate to your needs and where appropriate, seek professional advice in relation to legal, financial, taxation, mortgage or other advice.