Getting a home loan during COVID-19: the changes you need to be aware of

The COVID-19 pandemic has literally touched every sector in Australia, from small business to tourism, technology, and banking. One of the biggest changes, however, has been the temporary lending policy changes that banks and other financial institutions have put into place for buyers looking to purchase a home.

Under the current lending climate, getting an approval for your home loan isn’t what it was before — and with the second wave of the pandemic in full swing, it’s difficult to predict how long these restrictions will remain in place for.

If you’re thinking of buying a home this year, it’s important to wrap your head around these changes to put yourself in the best position possible to secure a loan during COVID-19.

How has COVID-19 affected lender policies?

There are a number of changes that lenders have put in place in light of the COVID-19 pandemic. With more borrowers experiencing a temporary reduction in work hours and salary — or worse yet, redundancy or business closures — lenders have tightened up their policies to adapt to the new financial climate.

Why?

Banks and lenders use risk as a key determining factor when determining home loan approvals. With an uncertain economic climate brought about as a result of the pandemic, banks have less of a risk appetite — which directly translates to more restrictions in terms of who they are willing to lend to and how much they are willing to lend.

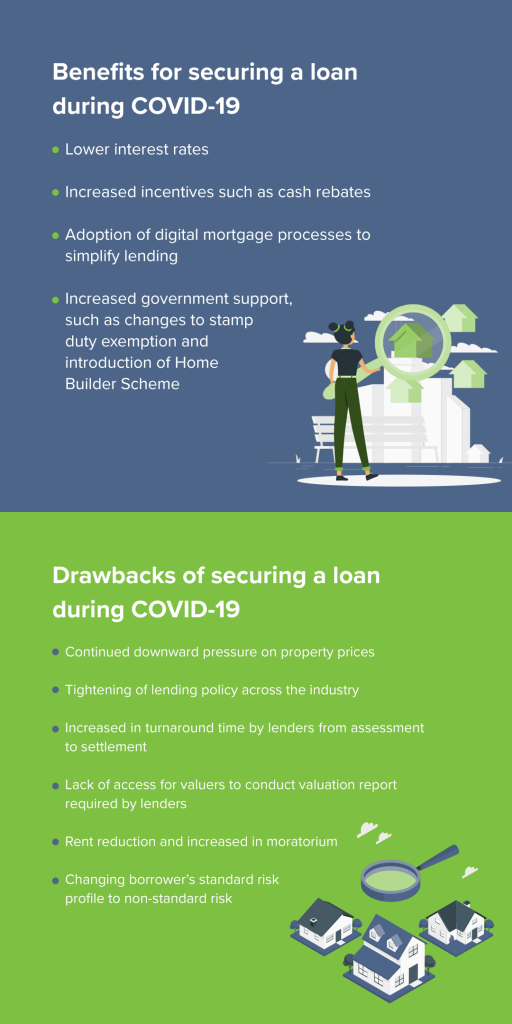

These changes have both upsides and downsides for borrowers:

What are the key criteria that lenders are focusing on?

Despite tightened lending criteria, banks and financial institutions are still approving residential and commercial loans during this time — the criteria has simply changed.

When considering loan approvals, lenders are now considering a number of factors including:

- Occupation. Lenders are now wanting to know if the industry you are working in has been heavily impacted by COVID-19 (i.e.hospitality, travel, entertainment, etc.)

- Employment type. Casual workers and contractors are deemed as higher risk, and some lenders may not accept a casual employee or contractor’s income when working the borrowing capacity.

- Rental income. Due to the continued downward pressure on rental prices, some lenders have reduced the reliance of rental income by using 60-70% of the gross rental income, instead of the full amount.

- Discretionary income. This refers to bonuses, commissions, and overtime. Lenders may only use a portion of this income when calculating borrowing capacity (for example, only factoring in 50% of the gross commissions earned, rather than the full 100%). Borrowers who work in essential services, such as health professionals or emergency service personnel, may be exempt from this lending provision.

- Loan-to-Value Ratio (LVR) restrictions. Lenders may reduce how much they are prepared to lend against a security deposit, depending on the purpose of the loan.

- Exit strategy. Lenders now want to understand how the borrower can pay off the loan if the requested loan term is longer than borrowers’ planned retirement age.

- Additional supporting documents. Self-employed borrowers may need to provide additional trading statements or Business Activity Statement (BAS) to confirm their business has not been affected by COVID-19. Salaried employees may be required to provide updated payslips prior to settlement.

- Employment check. Some lenders may contact your employer to confirm your employment arrangement prior to approval. This is to make sure your job is still secure.

Keep in mind that different lenders will apply different lending criteria depending on their risk appetite.

On top of this, there may be additional requirements from the lender which can be requested during the application process on a case-by-case basis. The above is just some of the ‘temporary’ changes that lenders are implementing.

The best way to secure a loan in this climate is to work closely with a mortgage broker, like the Rateseeker team.

Mortgage brokers are in constant communication with lenders, and can provide you with up-to-date advice on the best lender for your circumstances, as well as the lending criteria for that particular bank or financial institution. Learn more about the benefits of working with a broker here.

What happens if my loan is approved, but my employment circumstances change between approval and settlement?

Our expert brokers have seen some lenders continue to settle loans in this circumstance. However, many have demonstrated a tightening of their assessment criteria depending on their risk appetite — and some have started applying new lending restrictions on their existing pipelines of loans that are approved but not yet settled.

This means that if your employment circumstances change between approval and settlement, you may need to seek an alternate lending solution or work with different lenders to complete your purchase or refinance. This can be quite stressful, particularly if the application is time-sensitive.

How are lenders assessing borrowing capacity under stricter lending guidelines?

Lenders will apply their new temporary lending standards when assessing how much an individual can borrow during COVID-19.

When calculating household expenditure, lenders may also take into account factors such as a borrower’s ability to pay their loan based on their pre-COVID-19 income, their expectation to return to work after COVID-19, any anticipated income reductions in the near-future, personal circumstances, and more. This varies from lender to lender, which is why it’s crucial to work with a mortgage broker during this period.

For borrowers looking to refinance their existing loan to reduce their monthly repayments, lenders might suggest instead offering a repayment holiday as part of their COVID-19 financial assistance packages. Learn more about repayment holidays in Australia here.

What questions are lenders asking as part of the loan application?

If you’re applying for a loan during COVID-19, it’s a good idea to prepare yourself for some common questions that lenders are asking. These include queries like:

- Can you tell me about your job and the impacts of COVID-19?

- Has your employer given you any indication that COVID-19 may result in reduced hours or income?

- Have you reduced the rental income amount on any of your investment properties?

- How have COVID-19 measures impacted your business?

- Can you tell me about any future changes that you are aware of and how they may potentially impact your financial situation?

- After the COVID-19 pandemic, do you believe that you will be able to return to your normal employment conditions?

How to increase your chances of getting a loan during COVID-19

Despite tighter lending restrictions, it’s entirely possible to secure a loan during COVID-19.

If you’re planning to apply for a home loan, refinance your mortgage, or take out a commercial loan, here are a couple of things you can do to help with your application:

- Increase your deposit and minimise your unnecessary spending. Lenders prefer borrowers that can demonstrate strong savings conduct. This will give the lender comfort that you are able to service the requested loan amount.

- Minimise your unsecured liabilities. This includes unused credit cards, After Pay, overdrafts, and so on.

- Ensure you have a good credit score.

- Have a well-presented and comprehensive loan application. The application should outline your key strengths and mitigate any perceived risks by lenders, such as temporary reduction in income. Doing this will make your application look more favourable in the eyes of lenders.

Using a mortgage broker will help you navigate through the COVID-19 lending changes, and take the guesswork and stress out of applying for a home loan.

Our Rateseeker mortgage brokers have assisted a number of borrowers to get approved for a loan. Get in touch and learn how we can help you today with a complimentary, obligation-free consultation.

** General Advice Warning

The information provided on this website is general in nature only and it does not take into account your personal needs or circumstances into consideration. Before acting on any advice, you should consider whether the information is appropriate to your needs and where appropriate, seek professional advice in relation to legal, financial, taxation, mortgage or other advice.