Feeling the pinch? The impact of fixed rate changes

More and more Aussies are beginning to feel the effects of what’s being called the “fixed rate cliff.” As they transition from those super-low fixed rates they enjoyed for a while, many are finding themselves facing significant increases in their mortgage payments all across the country.

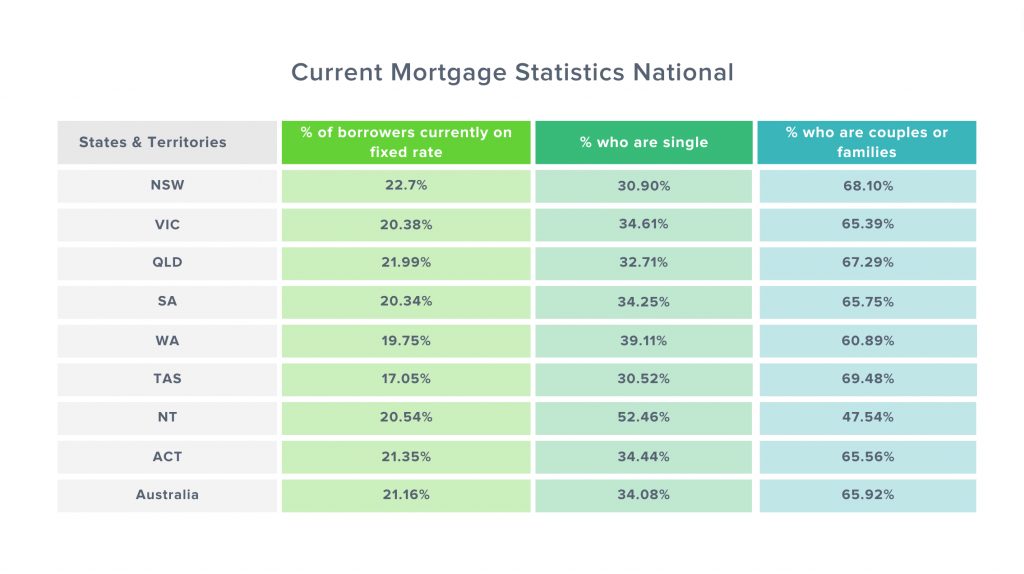

Finance experts have done some digging and found that only 21% of people with mortgages in Australia are still cruising along on those pandemic-era rock-bottom interest rates.

Let’s break it down and take a peek into what it means to own a home in Australia after several interest rate hikes.

These hikes have taken the average mortgage interest rate from a cozy 2% back in May 2022 to the current average of 6.27% for a basic interest rate.

So, where are the most fixed-rate lovers hiding? New South Wales takes the lead with 22.27% of folks still hanging on, followed by Queensland at 22%, Australian Capital Territory at 21.35%, and the Northern Territory at 20.5%. Meanwhile, Tassie residents seem to be the quickest to adapt, with only 17% still clinging to those fixed rates.

Now, let’s talk about who’s really feeling the squeeze. Out of those still on fixed rates, about 34% are solo homeowners who are now facing these rate hikes all by themselves. On the flip side, 65.9% are couples or families who will be hit with higher repayments when their fixed rate party comes to an end.

As the landscape keeps changing, it’s important for Aussie homeowners to stay informed and be prepared for potential changes in their mortgage costs.

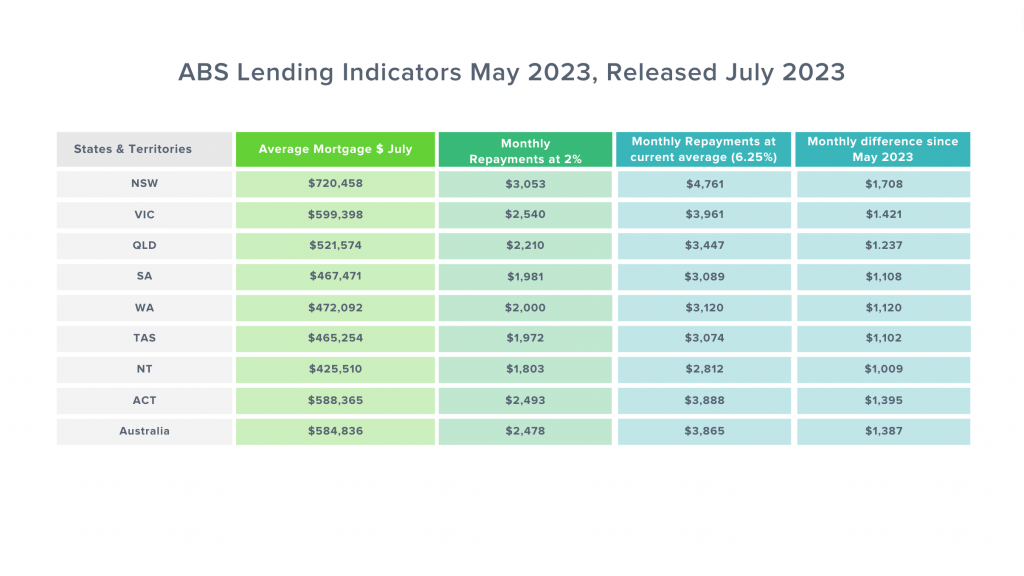

Further examination of the prevailing mortgage rates throughout the nation has unveiled a situation where homeowners transitioning from their fixed-rate periods, holding an average national mortgage of $585,000, are faced with a minimum increment of $1,000 in their monthly mortgage repayments. This increase is in comparison to the payments they were making before the current phase of tightening monetary policies.

The biggest surge is observed in New South Wales (NSW), where mortgage borrowers are feeling the heat with a spike of $1,708 per month. Following closely, in the state of Victoria, there is an increase of $1,421, while the Australian Capital Territory (ACT) is faced with an increase of $1,395, and Queensland observes a rise of $1,237.

On a nationwide scale, the average monthly mortgage repayments now stand at $3,865. This means homeowners have to dig deeper into their pockets to meet the additional financial commitment of $1,387 each month, as contrasted with the repayments calculated on a 2% interest rate that was applicable just 18 months ago.

The recent decision by the Reserve Bank of Australia to maintain interest rates for a consecutive second month has been met with widespread approval. Nevertheless, data shows that despite this decision, a significant majority of Australians are already grappling with substantial surges in their monthly mortgage repayments.

Who will be affected and how?

Given the current trajectory of interest rates, economists and property experts say it appears unlikely that there will be a substantial decrease in the near future. In light of this, it has been mentioned that the countdown has commenced for the 20% of homeowners who have yet to experience the full impact of the interest rate hikes.

As interest rates remain relatively fixed, it is anticipated that a heightened level of stress will be present within the housing market. Particularly felt among single homeowners, families with limited or single incomes, and investors who hold multiple properties. These people are most at risk of feeling the full effects of the fixed rates coming to an end.

As it stands, we are seeing a diminishing pool of disposable income, prompting an increasing number of individuals to explore all possible avenues to afford their property. For many new homeowners, this situation marks their inaugural encounter with such financial strain and possibly their first experience with financial hardship.

Why it’s critical to explore refinancing options now

A recent analysis has been done, encompassing potential monthly cost reductions associated with the average mortgage in each Australian state, assuming a homeowner chooses to refinance and secures a decrease of 0.45 basis points on their loan interest rate.

Data reveals that households who refinance their loans can save a minimum monthly amount of $117 by opting for a reduction of 45 basis points. For homeowners in New South Wales, the prospective monthly savings can even reach nearly $200.

On a national scale, the potential average monthly saving amounts to $161. This sum of money can be more effectively allocated to cover essential expenses such as groceries, bills, and other household necessities.

In a time of escalating living costs, it is crucial to actively pursue any avenues for savings that can help alleviate the financial, emotional, and psychological pressures arising from rising interest rates. Get in touch with us at Rateseeker, we’re committed to helping homeowners during this difficult time by making the refinancing process simple and stress-free.

Simply get in touch for an obligation-free chat and see how much we can save you on your monthly repayments.

** General Advice Warning

The information provided on this website is general in nature only and it does not take into account your personal needs or circumstances into consideration. Before acting on any advice, you should consider whether the information is appropriate to your needs and where appropriate, seek professional advice in relation to legal, financial, taxation, mortgage or other advice.