January 2026 Property Update: What Buyers and Investors Should Know Right Now

Welcome to a new year in property. While many people were enjoying a summer break, the market certainly did not slow down. Lending rules are shifting, investor activity is rising, affordability pressures are shaping where buyers look, and there are early signs that household budgets are starting to breathe again.

If you are planning to buy, invest, refinance or simply make smarter decisions with your home loan in 2026, understanding these early trends will put you in a far stronger position.

Here is what is already shaping the year ahead.

Investors Are Back in a Big Way

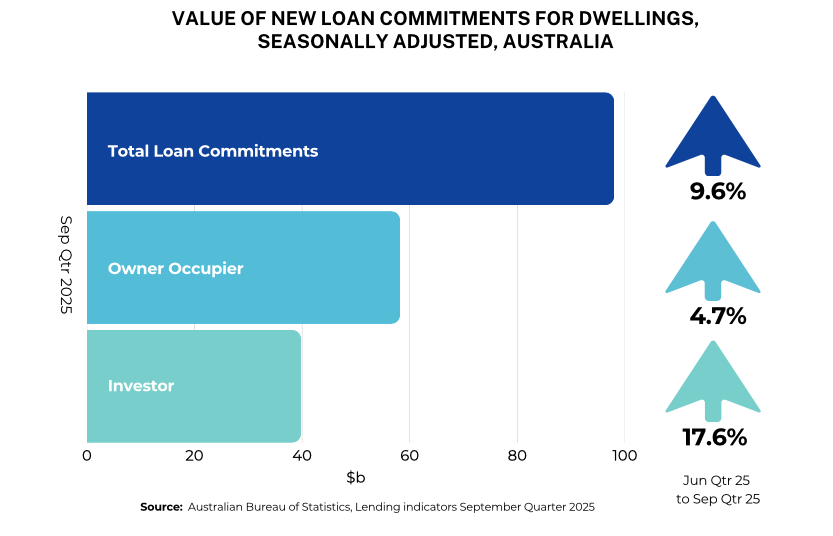

The latest figures from the Australian Bureau of Statistics show a clear and meaningful shift in investor activity.

In the September 2025 quarter, the value of investor loan commitments jumped by 17.6%. Compared to the same time a year earlier, investor lending was up 18.7%.

Investors now account for 40.6% of the value of all new loan commitments. That is the highest share since 2016.

This is not a small movement. It signals renewed confidence from investors, even though affordability challenges are still very real.

What Is Pulling Investors Back Into the Market?

Two main forces are doing the heavy lifting.

First, price growth has remained strong. National dwelling prices rose 8.6% over the course of 2025. That level of growth is hard for investors to ignore, especially after a period where many were sitting on the sidelines.

Second, rental demand remains robust. Rents climbed 5.2% over the same period, helping to support stronger rental income for property owners.

Yields did ease slightly, slipping from 3.7% at the end of 2024 to 3.6% at the end of 2025. This was not because rents fell, but because prices rose faster than rents. Even so, yields are still well above the pandemic low of 3.2% seen in 2021.

For experienced investors, yield is only one part of the picture. Borrowing capacity, cash flow buffers and the structure of the loan matter just as much. These are the factors that determine whether an investment is sustainable over the long term, not just whether it looks good on paper.

If you are considering an investment in 2026, the numbers need to be tested carefully against your current commitments, income and future plans.

Affordable Homes Are Growing Faster Than the Rest

If you are shopping in the more affordable end of the market, you may have already noticed that competition feels stronger, not weaker.

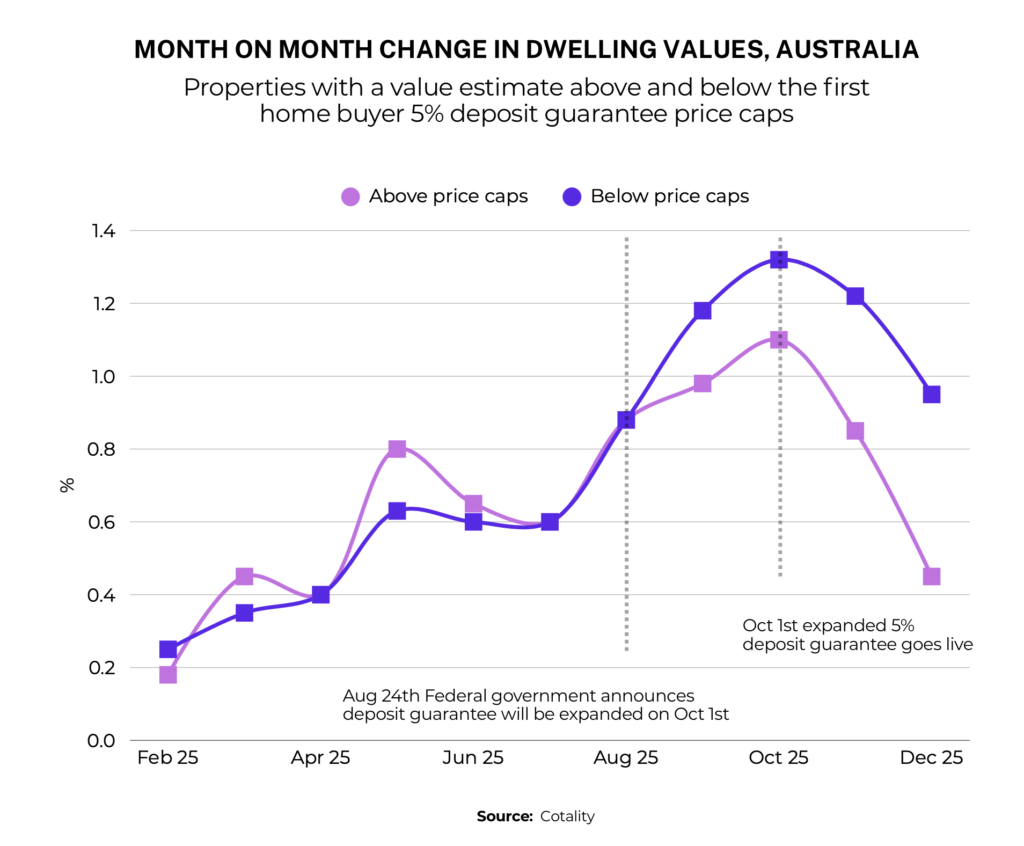

Since the federal government expanded the 5% Deposit Scheme in October 2025, homes under the scheme’s price caps have generally outperformed homes above those caps.

Cotality analysis shows that in the December quarter, median prices for properties under the cap rose 3.6%, compared to 2.4% for properties above the cap.

This is a meaningful difference in a short period of time.

Why Is the Lower End Growing Faster?

There are a few reasons.

Some buyers acted early, purchasing ahead of the official start date to secure a property before conditions tightened.

Serviceability limits are also steering buyer behaviour. With borrowing capacity still a hurdle for many households, more buyers are focusing on properties that feel manageable week to week, rather than stretching for the highest price they can technically qualify for.

In simple terms, buyers are prioritising comfort and sustainability over maximum borrowing.

A Reality Check Before Relying on the 5% Deposit Scheme

While the scheme is helpful, there are a few important things to understand before you base your strategy around it.

Price caps vary by location, so what qualifies in one area may not qualify in another.

Not every lender treats the scheme the same way. Some have more experience with it, while others apply stricter policies around servicing and documentation.

Your borrowing limit is still subject to normal credit checks and serviceability assessments. The scheme helps with deposit size, but it does not remove the need to qualify for the loan.

If you are considering buying under the scheme, it is important to check eligibility, lender participation and what the repayments would actually look like in your situation.

The Investing Shifts That Will Matter Most in 2026

This year, smart investing may be less about pushing limits and more about keeping your lending options flexible.

A few trends are already shaping how investors are approaching the year ahead.

Tighter Lending for Larger Loans

From February, banks are required to limit how many higher debt-to-income loans they write. This change is likely to reduce borrowing power for some investors, particularly those looking at larger purchases or already carrying significant debt.

It also means outcomes may vary more from lender to lender. Two banks may assess the same application very differently depending on their internal limits and current appetite for certain types of lending.

Rates Still Matter Between Reserve Bank Meetings

Many borrowers assume that nothing changes unless the Reserve Bank moves the cash rate. In reality, lenders can and do change pricing, policies and serviceability settings independently.

These changes can affect both your borrowing capacity and your monthly cash flow, even if official rates remain steady.

Alternative Pathways Are Staying Popular

Self-managed super fund investing and rentvesting continue to appeal to people who want to balance lifestyle choices with longer-term wealth building.

Rather than buying where they live, some borrowers are choosing to rent in their preferred area while purchasing an investment property elsewhere.

The common thread across all these strategies is flexibility. The choice of lender, the repayment type, how offsets are used, and the buffers built into the loan can all determine whether today’s decision makes tomorrow easier or harder.

Mortgage Stress Is Easing, But Buffers Still Matter

After a challenging few years for household budgets, there is some encouraging news.

Research from Roy Morgan shows that mortgage stress has dropped to its lowest level since January 2023. Many households are starting to feel more comfortable with their repayments as incomes adjust and rates stabilise.

This is positive, but it is not a reason to become complacent.

Why Now Is the Time to Build a Buffer

When things feel more comfortable, that is often the best time to strengthen your position.

Building a buffer into your loan can help protect you if rates change, expenses rise or your income shifts in the future.

If you are buying this year, it is wise not to test your budget based only on today’s repayments. A safer approach is to check whether you could still manage if rates increased, your expenses jumped, or your income changed.

If you already have a loan and cash flow feels tight at times, you are not alone. Many households experience this. The key is addressing it early while you still have options.

What You Can Do If Cash Flow Feels Tight

Refinancing may help reduce your rate or improve your loan features.

Restructuring your loan by adjusting the term, repayment type, or offset strategy can help smooth out repayments.

Consolidating higher-interest debts into your mortgage may reduce the total interest you pay and free up cash flow.

There is no shame in reviewing your position. In fact, it is one of the smartest financial moves you can make.

What This Means for Buyers in 2026

For buyers, the combination of investor activity, government schemes and serviceability limits is reshaping demand.

Competition is strong in affordable price brackets. Investors are active again. Borrowing capacity remains a key constraint for many households.

This means preparation is more important than ever.

Understanding your true borrowing limit, what your repayments would look like under different scenarios and which lenders suit your situation can make a significant difference to the outcome.

Rushing into a purchase without this clarity can lead to unnecessary stress later.

What This Means for Investors in 2026

For investors, the environment is improving, but it is also becoming more complex.

Price growth and rental demand are attractive, but lending rules are tightening for higher debt levels. Lender policies are shifting. Yields are steady but not spectacular.

Success this year is likely to come from careful loan structuring rather than aggressive borrowing.

Choosing the right lender, setting up the loan with flexibility in mind and keeping buffers in place will matter more than simply chasing the next property.

The Importance of Early Planning

One clear theme is emerging across all of these trends. Early planning gives you more choices.

Waiting until you have found a property or until cash flow feels uncomfortable limits your options. Acting early allows you to compare lenders, structure your loan properly and make decisions that support your longer-term goals.

Whether you are buying your first home, upgrading, investing or simply reviewing your current loan, having a clear plan for 2026 will put you in a much stronger position.

A Busy Start to the Year

With investor activity rising, affordable homes outperforming, new lending limits coming into effect and household budgets beginning to stabilise, 2026 is already off to a busy start.

These are not isolated changes. They are all connected through lending rules, affordability and how borrowers are adapting to the current environment.

Understanding how they apply to your situation is the key step.

If you are planning a move this year, whether that means buying, investing, refinancing or restructuring, it is worth talking through your options early. The right structure today can make the rest of the year far more comfortable and far more strategic. If you’re planning a move this year, buying, investing or restructuring, let’s talk through your options early. Contact Rateseeker today!

** General Advice Warning

The information provided on this website is general in nature only and it does not take into account your personal needs or circumstances into consideration. Before acting on any advice, you should consider whether the information is appropriate to your needs and where appropriate, seek professional advice in relation to legal, financial, taxation, mortgage or other advice.