February 2026 Property Update: Rising Borrowing, Higher Rates and New Lending Rules

It is shaping up to be a decisive start to 2026.

Borrowing activity is lifting. Interest rates have moved again. Rental markets remain tight. Property prices have reached new highs. New lending caps are reshaping how banks assess risk at the margins.

There is momentum in the market, but it is disciplined momentum.

If you are buying, investing, refinancing, or even just thinking about your next move, the key theme for February is this: preparation now matters more than ever.

Let us break down what is happening and what it means for you.

Loan Activity Is Rising Again, But Credit Is Not Loose

The latest data from the Australian Bureau of Statistics shows a clear shift in borrowing activity.

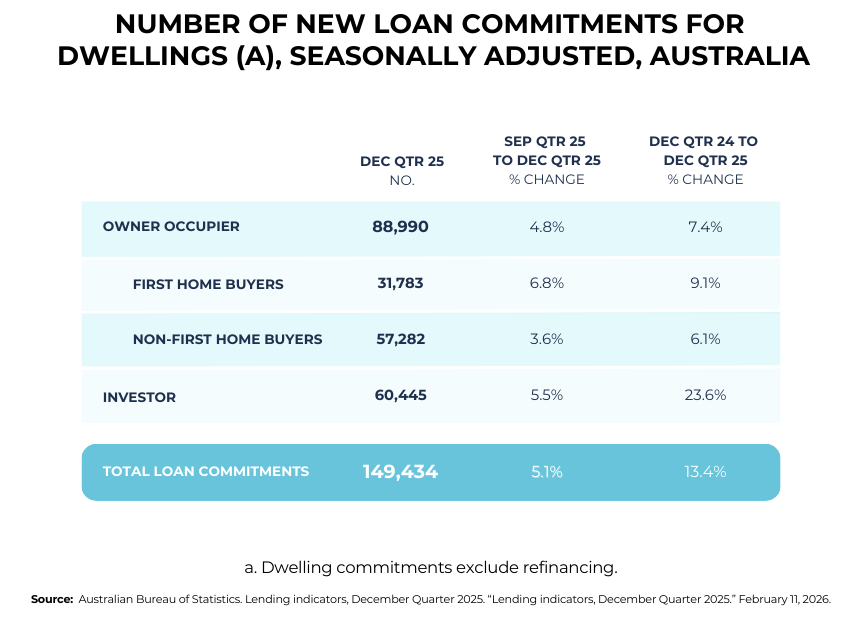

In the December 2025 quarter, the number of new loan commitments, excluding refinancing, was 13.4% higher than a year earlier.

On the surface, that is a strong rebound.

But the detail underneath tells a more nuanced story.

Owner-occupier activity rose 7.4% year on year.

First-home buyer loans increased 9.1%.

Investor activity jumped 23.6%, with investor loans hitting a quarterly record.

Confidence is improving. More Australians are stepping back into the market. Investors, in particular, are moving decisively.

However, rising activity does not mean lenders have relaxed their standards.

Serviceability buffers remain in place. Living expense assessments are still thorough. And from February, new limits on high debt-to-income lending add another layer of discipline.

In other words, borrowing is rising, but the gates are not wide open.

What Rising Loan Activity Means for Buyers

When more borrowers enter the market, competition increases.

You may see more bidders at auctions. More private treaty properties are selling quickly. More investors are competing for the same opportunities.

This environment rewards preparation.

If you are buying, clarity around your borrowing capacity is not optional. It is essential.

A pre-approval is no longer just a comfort. It is a strategic advantage. Knowing your numbers allows you to move quickly and confidently when the right property appears.

It also prevents emotional overspending.

Rising activity can create urgency. But the smartest buyers anchor decisions to their financial reality, not headlines.

What It Means for Investors

Investor lending has surged by 23.6% over the past year, reaching a new quarterly record.

That signals a strong belief in the long-term fundamentals of Australian property.

But investors are also operating in a more structured lending environment.

With tighter oversight around higher debt-to-income ratios and careful serviceability checks, the loan structure becomes critical.

Are you using the right entity?

Is your debt positioned strategically?

Are you maximising deductibility while maintaining flexibility?

In a market where investor competition is strengthening, structure matters just as much as location.

February’s Rate Move Is Now Flowing Through

Borrowers are now feeling the impact of the Reserve Bank of Australia’s decision on 3 February to lift the cash rate.

Since that move, many lenders, including the four major banks, have increased their variable rates.

For variable borrowers, that means higher repayments.

And the repricing did not begin on 3 February.

In the weeks leading up to the decision, several lenders had already started lifting fixed rates. Markets had anticipated a rate rise, and lenders moved early.

That means some borrowers who fixed recently may have locked in higher rates than were available late last year.

This is how rate cycles typically unfold.

Variable rates tend to move quickly after an RBA change.

Fixed rates often move in advance, based on market expectations.

Not all lenders adjust at the same pace or by the same amount.

That final point is important.

Even in a rising rate environment, pricing gaps between lenders can be meaningful.

Why Rate Comparison Matters More in 2026

When rates were stable, small pricing differences between lenders felt less significant.

In a rising rate environment, every fraction of a percent counts.

A slightly sharper rate can translate to thousands of dollars over the life of a loan.

But rate alone is not the full story.

Loan structure matters.

Do you have a full offset account?

Are you making principal and interest repayments or interest only?

Is your loan flexible enough to allow extra repayments?

These features can influence how much interest you pay over time, sometimes more than the headline rate difference.

Reviewing your current loan is not about chasing the absolute lowest rate in the market. It is about ensuring your structure still aligns with your goals in today’s environment.

Renting and Buying Are Both Getting Harder

One of the defining tensions of early 2026 is this.

Renting is difficult. Buying is expensive.

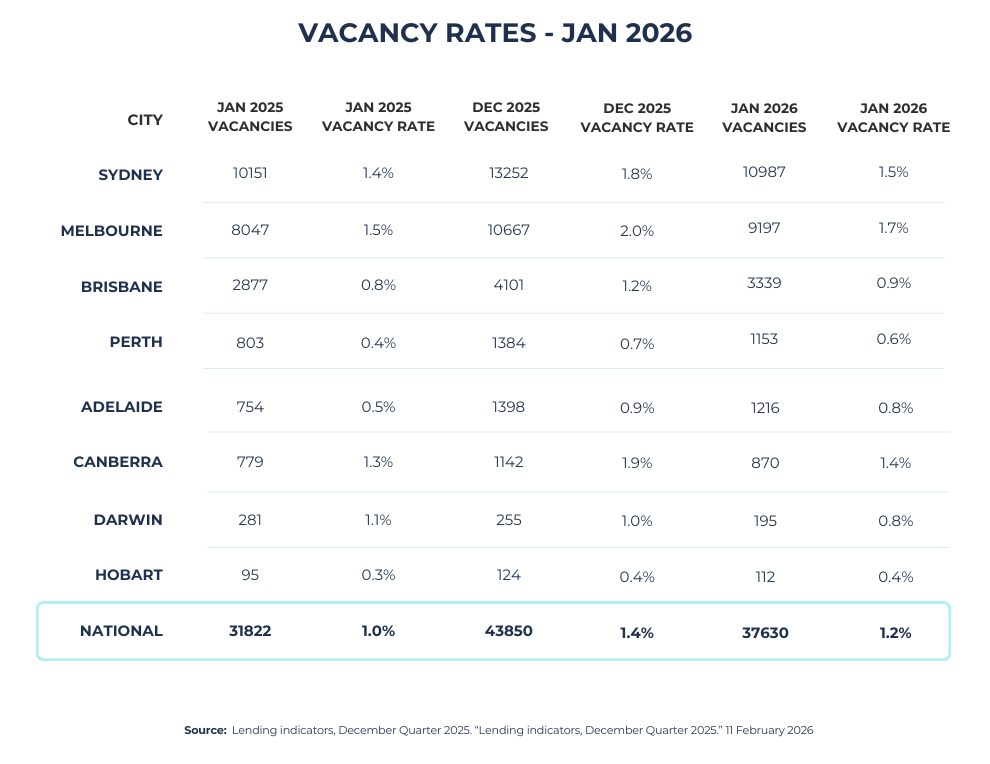

Australia’s national vacancy rate is sitting at just 1.2%, according to SQM Research. That means rental stock remains extremely tight.

At the same time, the national median property price has climbed to a record 912,000 dollars, according to Cotality.

Prices are up 9.4% over the past year. Over five years, they have increased 46.1%.

Low supply. Strong demand. Record prices.

That combination creates pressure across the housing market.

If You Are Renting

With vacancy rates at 1.2% nationally, competition remains strong.

When your lease comes up for renewal, rent increases remain a real possibility.

For some households, that is triggering a rethink.

If you are already paying a high rent and your income supports mortgage repayments at a similar level, the rent versus buy calculation can shift quickly.

Buying is not automatically cheaper. But when rents keep edging higher, ownership begins to look more attractive, particularly if you plan to stay in an area long term.

The key is to compare numbers, not headlines.

How much deposit do you need?

What would repayments look like at today’s rates?

How do ongoing costs compare to rent?

A personalised comparison often tells a clearer story than broad market commentary.

If You Are Buying

Record prices can feel intimidating.

But record prices do not mean opportunities disappear.

They mean preparation matters more.

In a market where prices have risen 9.4% over the past year, realistic budgeting is crucial.

Stretching beyond your comfort zone because prices are rising can create stress later.

A clear budget, firm pre-approval and defined criteria can help you move decisively when the right property appears without overextending.

It is also worth remembering that long-term growth is built over years, not months.

Trying to perfectly time the market rarely succeeds.

Choosing a loan structure that remains manageable under different scenarios is far more important.

New Debt-to-Income Caps Are Now in Effect

From 1 February, a new layer of lending discipline has taken effect.

APRA, the Australian Prudential Regulation Authority, is ensuring that authorised deposit-taking institutions limit high-debt-to-income loans to no more than 20% of new mortgage lending in both owner-occupier and investor segments.

A high debt-to-income loan is defined as a total debts that are six times the annual income or more.

This is not a ban.

Lenders can still write high debt-to-income loans. But only within that 20% cap.

This introduces a guardrail around the riskiest lending without shutting it down entirely.

How the New DTI Limits May Affect Borrowers

For many borrowers, these changes will not be noticeable.

If your total debt sits well below six times your income, you may not feel any difference.

But if you are stretching toward higher leverage, the new limits could influence how lenders assess your application.

APRA has observed a modest rise in higher geared lending, particularly among investors. With housing credit and prices climbing from already elevated levels, regulators are keen to ensure vulnerabilities do not build across the system.

Limits like this do not change your credit score.

They do not automatically make you ineligible.

But they can influence lender appetite.

Some lenders may become more selective about which high-debt-to-income loans they approve, particularly as they approach their internal caps.

That makes lender selection and application positioning more important.

Positioning Your Application in 2026

With higher rates, rising investor demand and new DTI caps, a strong application is about more than just income.

It is about how your income and debt fit together.

Lenders assess:

- Your total income

- Your total existing debts

- Your living expenses

- Your deposit and equity

- Your employment stability

Understanding how these factors interact under different lender policies can significantly improve your outcome.

Sometimes, the difference between approval and decline is not your income. It is the lender’s risk appetite at that moment.

Preparation, documentation and strategic lender choice can make a noticeable difference.

Momentum With Discipline

February 2026 feels like a market with momentum.

Borrowing is up 13.4% year on year.

Investor activity is at a record.

National prices have reached 912,000 dollars.

Vacancy rates remain tight at 1.2%.

But this is not a free-flowing credit boom.

Rates have risen.

Serviceability buffers remain.

New DTI caps are in place.

It is a market that rewards informed borrowers.

A small adjustment now can make a significant difference later.

That might mean reviewing your current rate.

Restructuring your loan.

Strengthening your borrowing position before applying.

Or clarifying whether renting or buying makes more sense for your situation.

The Bigger Picture for 2026

Every year begins with its own narrative.

This year’s narrative is not about panic or frenzy.

It is about balance.

Confidence is improving, but discipline remains.

Prices are high, but supply is tight.

Rates have risen, but competition between lenders still creates opportunity.

For borrowers and investors, that means one thing.

Clarity beats speculation.

Knowing your borrowing capacity.

Understanding how rate changes affect your repayments.

Recognising how new regulatory caps influence lender behaviour.

These insights help you move from reactive to strategic.

Your Next Step

Between higher rates, stronger investor demand and record prices, 2026 has started with energy.

But energy without structure can create stress.

If you are considering buying, investing or refinancing this year, the smartest move is to understand exactly where you stand.

How much can you borrow under current settings?

Is your rate still competitive after February’s changes?

Do the new DTI caps affect your plans?

Does renting or buying make more financial sense right now?

These are not questions to leave to guesswork.

They are questions that deserve personalised answers.

A clear plan today can position you confidently for whatever the rest of 2026 brings.

If you would like to map out your next move, review your borrowing capacity or check whether your current rate still stacks up, reach out to mortgage experts at Rateseeker, and we will run the numbers together.

** General Advice Warning

The information provided on this website is general in nature only and it does not take into account your personal needs or circumstances into consideration. Before acting on any advice, you should consider whether the information is appropriate to your needs and where appropriate, seek professional advice in relation to legal, financial, taxation, mortgage or other advice.