November 2025 Property Market Update: What Buyers and Borrowers Need to Know

Australia’s property market continues to show its resilience as we move through the final quarter of 2025. Prices have now risen for eight consecutive months, climbing another 0.8% in September, and buyers, sellers and homeowners are watching the November 4 RBA meeting closely to see whether the cash rate will hold steady or shift again.

Despite the uncertainty, the latest indicators paint a clearer picture of where the market is heading. New home construction is strengthening, brokers are filling the service gap left by branch closures, selling conditions are shifting, and borrowers are taking a closer look at comparison rates as they assess the real cost of their mortgages.

In this month’s newsletter, we break down what these changes mean for you and how you can stay ahead of the market as the year draws to a close.

Home Construction Picks Up as Conditions Improve

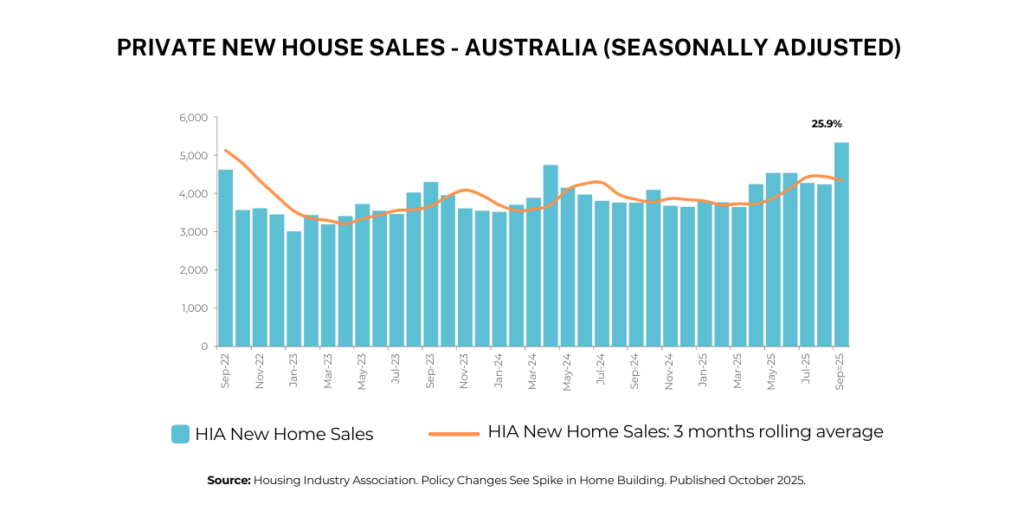

While established home prices continue rising, a growing number of Australians are turning their attention to building rather than buying. The Housing Industry Association (HIA) reports a 25.9%increase in new home sales in September, with quarterly growth at 4%.

This uptick reflects three key shifts:

1. Lower interest rates

The recent rate cuts have helped reduce borrowing costs, pushing more buyers to reconsider building as a more financially viable option.

2. Government incentives

Some state-based grants, stamp duty concessions and construction support packages remain active, particularly for first home buyers and regional movers.

3. Rising established home prices

In many suburbs, construction now provides better dollar-for-dollar value compared to purchasing an existing home, especially when factoring in energy-efficient builds and modern layouts.

Why more Australians are building instead of buying

Building allows buyers to design the home they want, benefit from new-building warranties, avoid major renovation costs and sometimes access incentives that established properties do not qualify for.

However, construction comes with its own challenges. Progress payments, builder timeframes, supply shortages and cost variations can create unexpected pressure if not managed well.

Five Practical Tips for Financing a New Home Build

If you are thinking about building, here are the essentials to keep your project running smoothly:

Set a clear budget

Include a 10 to 15% buffer for variations, material price changes or upgrades.

Secure pre-approval early

Knowing your borrowing power helps you plan your build with certainty and gives builders confidence in your finances.

Understand how construction loans work

Funds are released in stages rather than all at once. Knowing when each progress payment is triggered helps you manage cash flow.

Plan for dual living costs

Many owners pay rent or an existing mortgage during the build. Factor this into your budget so the overlap period does not strain your finances.

Stay in frequent communication

If costs shift or construction plans change, notify your lender quickly. Clear documentation prevents approval delays.

If building is on your radar for 2026, it is worth discussing your finance options before you start comparing designs or visiting display homes.

Brokers Step Up as Bank Branch Closures Accelerate

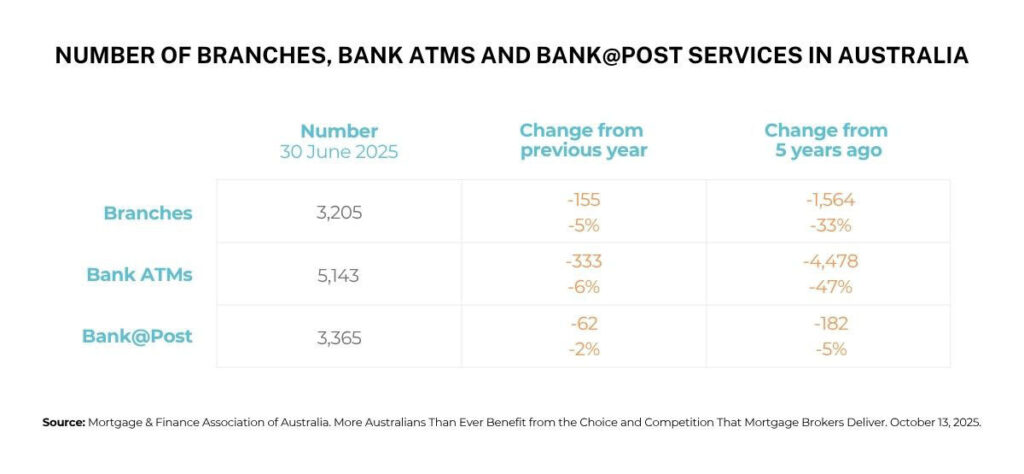

If your local bank branch has closed recently, you are far from alone. Canstar analysis reveals that Australian bank branch numbers have dropped 5% in the past year and 33% over the past five years.

Digital banking has become the default for routine transactions, but for major financial decisions like home loans, customers still value personalised guidance. With fewer branches and shorter in-person services, borrowers are turning to brokers for the support banks used to provide face-to-face.

Why more borrowers are choosing brokers

According to the latest Cotality research, brokers now write 77.6% of all new home loans, up from 67.2% just two years ago. That is a dramatic rise and highlights two important trends:

Choice matters.

A single bank can only offer its own products, but a broker can compare dozens of lenders and provide recommendations tailored to your situation.

Best Interests Duty protection.

Brokers are legally required to act in your best interests. Banks are not. This gives borrowers confidence that the guidance they receive is independent and aligned with their goals.

Why the shift away from branches is not slowing down

As banks streamline their networks and invest in digital systems, brokers have become the main source of personalised lending support in Australia. For many borrowers, meeting online or in person with a broker provides clarity, reassurance and a clearer path through complex lending policies.

If you are planning to buy or want to review your current loan, now is a good time to reach out so the right lender, loan type and structure can be compared for you.

Homes Are Selling More Slowly, But Prices Remain Firm

Selling conditions softened slightly in the September quarter, but the cooling has not resulted in weaker prices.

Cotality data shows:

Median days on market

Up from 27 to 30 days compared to the same time last year.

Median vendor discount

Narrowed from 3.3% to 3.2%.

What this tells us is that while buyers are taking a little more time to make decisions, sellers are still achieving strong results and pricing remains relatively firm.

What the shift means for buyers

Slower selling times can create opportunities for well-prepared buyers, but competition is still active enough to keep upward pressure on prices.

If you are planning to buy:

Get pre-approved early

The buyers who secure the best properties are the ones who can act quickly when they find the right home.

Do your research

Look at recent comparable sales, not just listing prices. This helps you understand fair value and avoid overpaying.

Focus on value over bargains

In a rising market, waiting for a major discount can mean missing out on quality homes.

Being finance-ready and market-aware is the key to moving with confidence.

Comparison Rates: What They Are and Why They Matter

When comparing home loans, many borrowers focus solely on the interest rate. While the headline rate is important, it does not show the full cost of a loan.

The comparison rate helps fill that gap.

What the comparison rate includes

Interest rate

The cost of borrowing the loan amount.

Fees

Most upfront and ongoing fees such as annual package fees and account-keeping fees.

Comparison rate

A combined figure that gives a clearer idea of what the loan will cost over time.

For example:

Loan A has a lower interest rate but higher ongoing fees.

Loan B has a slightly higher rate but low fees.

Once the fees are included in the comparison rate, Loan B may actually cost less overall.

A simple but important reminder

Comparison rates are based on a sample loan size of $150,000 over 25 years. Most home loans today are larger and longer, so the comparison rate should be used as a directional guide rather than a precise figure.

If you want a clearer picture of which loan suits your goals, we can compare your options side by side and calculate your personalised cost difference.

What This Means for You Heading Into the End of 2025

The property market remains active, lending policies continue shifting, and the broader economic environment is evolving as we wait for the next RBA decision. With new home sales growing, branch closures accelerating and selling conditions adjusting, this period of transition offers both opportunities and challenges.

For buyers, it is a good time to understand your borrowing power, secure pre-approval and explore all options, including building and established homes.

For homeowners, reviewing your loan could uncover meaningful savings, especially as lenders continue to adjust pricing differently after the rate cuts earlier this year.

For sellers, the market remains competitive, with firm prices and steady buyer demand despite slightly slower selling timelines.

If you are planning to build, buy or refinance, now is the time to check your finances and make sure your loan is set up for what is ahead.If you would like help comparing lenders or reviewing your borrowing position, feel free to contact RateSeeker. We are here to guide you through every step and make the next move as smooth as possible.

** General Advice Warning

The information provided on this website is general in nature only and it does not take into account your personal needs or circumstances into consideration. Before acting on any advice, you should consider whether the information is appropriate to your needs and where appropriate, seek professional advice in relation to legal, financial, taxation, mortgage or other advice.