Rateseeker Round-Up: December 2025 Business & Commercial Finance News

As 2025 draws to a close, the landscape for Australian businesses is shifting once again. Interest rates have eased, lending activity is strengthening, and confidence, while still cautious, is beginning to stabilise across key industries. For many business owners, this period marks the final chance to take stock before rolling into a new year of planning, investing, and growth.

This month’s Rateseeker Round-Up takes you through the most important developments shaping the business and commercial finance sector. Whether you’re considering an expansion, preparing a fit-out, upgrading equipment or simply reviewing your cash flow strategy, understanding these trends can help you make smarter decisions heading into 2026.

In this edition, we explore:

• The RBA’s latest signals and what they mean for SMEs

• Why construction finance is surging close to record levels

• A strong rise in asset finance demand across industries

• Why many businesses are stepping away from credit cards

• Practical steps to prepare your business for better conditions in the new year

Let’s break it all down.

Stability Returns: RBA Signals a More Supportive Environment for SMEs

After a challenging period marked by high borrowing costs, tight margins and unpredictable cash flow patterns, the Reserve Bank now says conditions for small and medium enterprises have finally steadied.

It is not a full recovery, certain industries are still feeling the strain, but the worst of the instability appears to have eased.

Confidence Is No Longer Sliding

For most of 2024, SME sentiment trended downward each quarter. The combination of elevated costs, falling sales in some sectors and limited access to cheap capital kept business confidence subdued. The RBA now notes that confidence has stabilised, giving business owners a slightly clearer runway to plan ahead.

For many, this stability is an opportunity to bring forward decisions that were delayed earlier in the year.

Cash Flow Pressures Are Easing

The interest rate cuts delivered through 2025 are gradually flowing through the system. While the full benefit will take several more months to show up in business loan repayments, early signs indicate that many SMEs are seeing modest improvements in cash flow.

Lower interest expenses mean more flexibility, whether that’s paying suppliers faster, investing in growth or rebuilding liquidity buffers.

Access to Credit Has Improved

Competition between banks and non-bank lenders has played a significant role in improving credit conditions. Non-banks, in particular, have been more aggressive in offering faster turnaround times and more flexible approval criteria.

This doesn’t mean lending is wide open, lenders remain selective, but overall conditions are more supportive than they were at the start of the year.

Margins Are Holding Up

One of the more encouraging signs is that SME operating profit margins remain close to pre-pandemic averages. It hasn’t been easy: staffing costs, rents and insurance all climbed over the past two years. Yet many operators have adapted, improving efficiency and finding creative ways to maintain profitability.

But Some Sectors Remain Under Pressure

Construction, hospitality and discretionary retail continue to shoulder more strain than others. Higher debt levels combined with still-soft consumer demand mean these industries face longer recovery timelines.

If your business falls within these sectors, the key is to balance caution with opportunity. Reduced rate pressure could provide breathing room heading into 2026, but careful planning remains essential.

How Rateseeker Can Help

If you want to use this more stable environment to revisit your loan structure, strengthen your cash flow or explore refinancing opportunities, our team can guide you through your options and help you position your business for the year ahead.

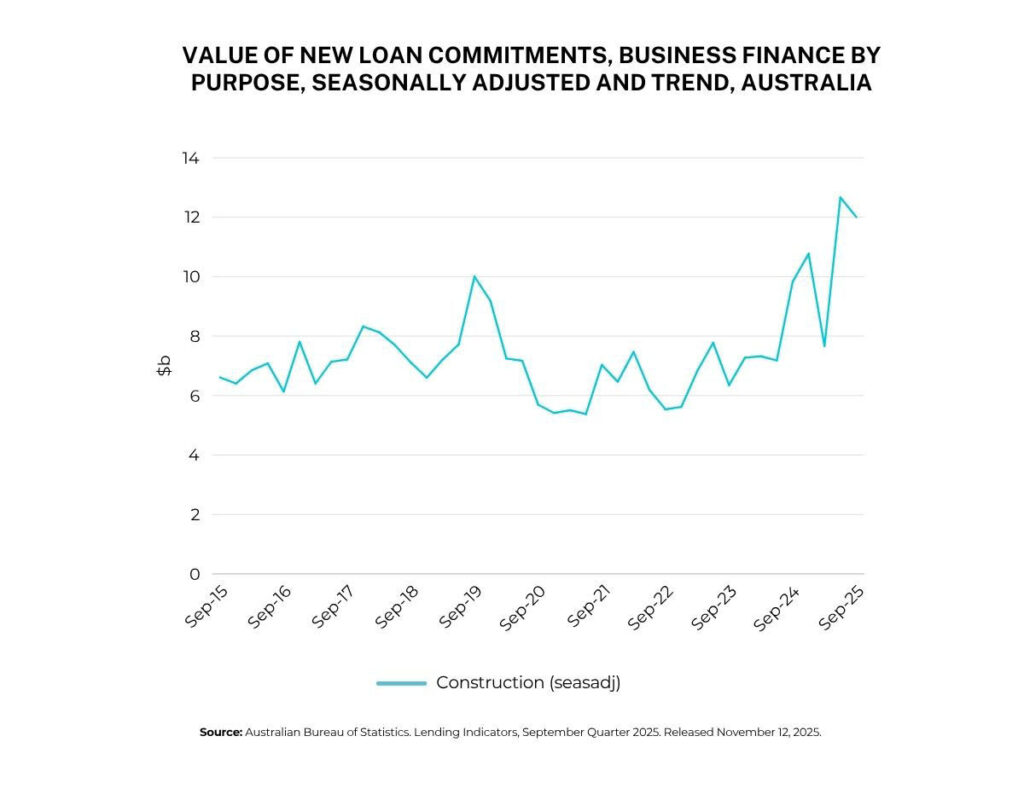

Construction Lending Surges as Businesses Lock In Funds

One of the standout developments this quarter has been the surge in construction finance. According to the Australian Bureau of Statistics, lending for construction in the September quarter was 22.1 per cent higher than a year earlier and close to record levels.

This upward trend suggests many businesses are choosing to invest in their current space rather than move into a new one.

Businesses Are Upgrading Instead of Relocating

With commercial rents elevated and suitable premises often limited in high-demand areas, business owners are opting for strategic upgrades instead of relocation.

Common examples include:

• Hospitality refurbishments

• Retail redesigns

• Warehouse extensions

• Office reconfigurations

• Workshop upgrades

• Fit-outs for specialised industries

These decisions aren’t just cosmetic. They support operational efficiency, customer experience and long-term growth.

Why the Timing Matters

Demand for trades and materials has risen again, which can stretch project timelines and introduce cost pressures. Businesses planning renovations or fit-outs are securing finance earlier to avoid delays once construction is underway.

Construction Finance Isn’t Like a Standard Loan

Unlike typical term loans, construction finance is released in stages as work progresses. Lenders require detailed documentation before approving and releasing funds, including:

• Builder contracts

• Cost breakdowns

• Council approvals (if required)

• Progress valuations

• Project timelines

Without these documents prepared early, approvals can stall, and construction can be delayed.

How Rateseeker Can Support Your Project

If you’re planning a fit-out, expansion or renovation, early preparation is essential. Rateseeker can help you map out funding requirements, coordinate the documentation process and ensure your project stays on track from start to finish.

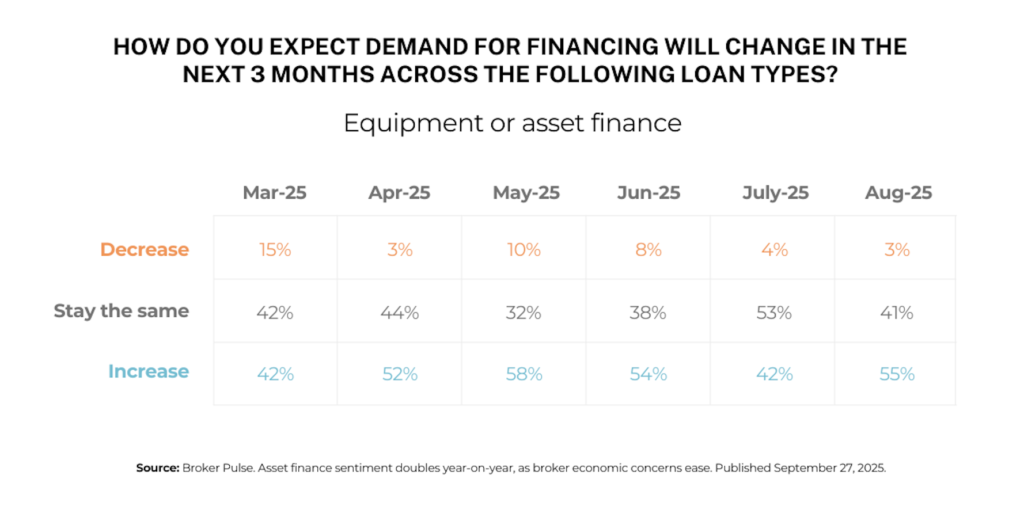

Asset Finance Demand Climbs as SMEs Prepare for Growth

Asset finance is staging a strong comeback, with businesses across industries preparing for expansion or refreshing vital equipment.

A recent Agile Market Intelligence survey found that 55 percent of brokers expect asset finance activity to rise over the next quarter. Only 3 percent expect demand to decline, creating a net positive sentiment of 52 percent, double what it was at the same time last year.

Why Businesses Are Upgrading Now

With interest rates easing, upgrading equipment is becoming more cost-effective. Businesses are looking to improve productivity, manage maintenance costs and prepare for higher demand in 2026.

The strongest activity is coming from industries such as:

• Transport

• Civil and construction

• Agriculture

• Manufacturing

• Trades

• Logistics

• Medical and allied health

Non-Banks Are Driving Competition

Non-bank lenders are stepping up by offering faster turnaround times and more flexible terms, which is particularly attractive for businesses needing equipment urgently. This competitive landscape is encouraging more businesses to explore new finance options that may not have been available a year ago.

Structuring Deals to Protect Cash Flow

When comparing asset finance options, the structure of the deal matters just as much as the interest rate. Balloon payments, repayment terms and seasonal payment options all play a role in supporting cash flow during slower periods.

If you’re considering new vehicles, machinery or equipment, Rateseeker can help you compare lenders, evaluate the structure and secure financing that suits your operational needs.

Why Businesses Are Moving Away from Credit Cards

While credit cards feel convenient, rising costs and persistent high interest rates have made them one of the least efficient ways to fund business purchases.

New RBA data shows that from September 2024 to September 2025:

• Interest rates on new variable loans for small businesses fell by 0.54 percentage points.

• Fixed rates fell by 0.90 percentage points.

The shift means business loans and equipment finance are becoming more affordable, while credit card rates have barely budged.

Credit Cards Compound Quickly

Most business credit cards carry double-digit interest rates. When balances roll over month to month, costs escalate rapidly. This results in short-term debt being used to fund long-term business needs, a mismatch that creates unnecessary financial pressure.

Smarter Alternatives Are Readily Available

Term loans, unsecured business loans and equipment finance allow for structured repayments aligned with the life of the asset. These options:

• Support cash flow more effectively

• Reduce reliance on revolving debt

• Offer clearer, more predictable repayment schedules

• Help businesses plan ahead without hitting credit limits

If you’re using a card to fund equipment, stock or seasonal growth, it’s worth reviewing lower-cost alternatives. Rateseeker can compare options and help you transition to more sustainable finance structures.

Final Thoughts: Set Your Business Up for a Strong 2026

With lending activity strengthening, credit conditions improving and interest rates easing, the final weeks of 2025 offer a valuable window for business owners to reset and prepare for the year ahead.

Whether you’re planning upgrades, reviewing your loan structure or exploring new equipment finance, small adjustments made now can have a compounding effect into 2026.

If you’d like to assess your options, talk through scenarios or map out a strategy aligned with your goals, Rateseeker is here to guide you every step of the way.

** General Advice Warning

The information provided on this website is general in nature only and it does not take into account your personal needs or circumstances into consideration. Before acting on any advice, you should consider whether the information is appropriate to your needs and where appropriate, seek professional advice in relation to legal, financial, taxation, mortgage or other advice.