RateSeeker Round-Up: July Property News

As the new financial year begins, Australia’s property market continues to evolve, and there’s no shortage of headlines shaping the outlook for both buyers and investors. From growing calls for another RBA rate cut to falling fixed-rate offers and continued rental growth, July brings a mix of opportunities and cautionary tales for the months ahead.

Here’s what’s happening right now in property.

Case Builds for an Extra Rate Cut

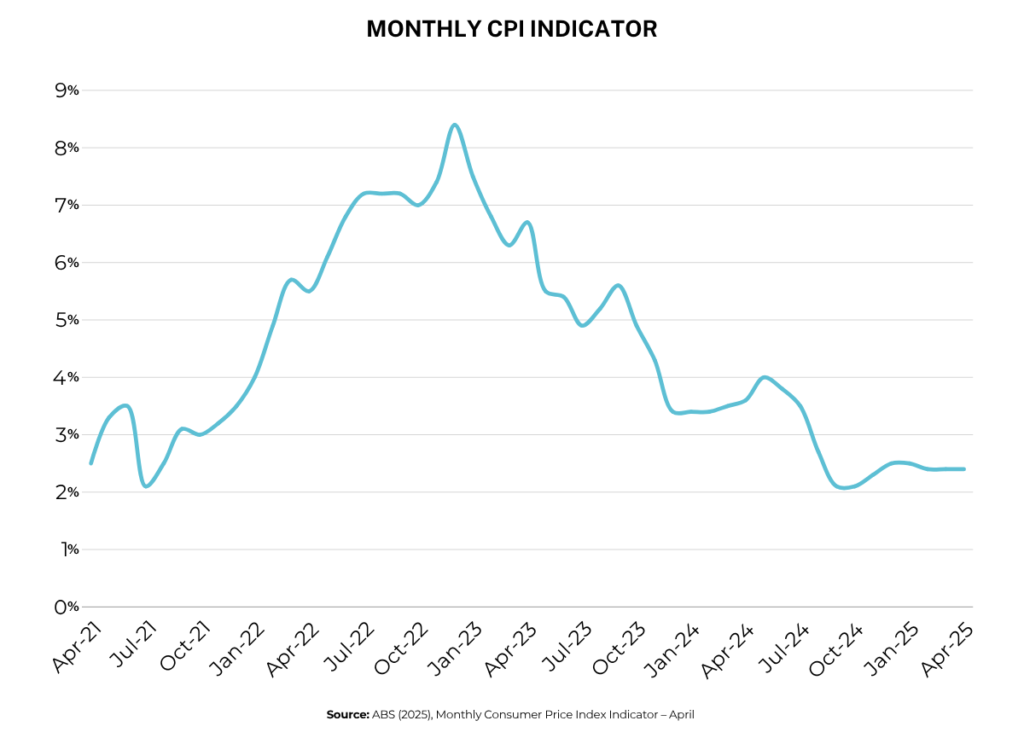

The Australian Bureau of Statistics (ABS) has released the latest inflation figures, and they make for encouraging reading. In April, the annual inflation rate sat at 2.4%, marking the ninth consecutive month within the Reserve Bank of Australia’s (RBA) target range of 2–3%.

The more closely watched trimmed mean inflation rate, which excludes volatile price changes, came in at 2.8%, its fifth month within target. That consistency is a sign that inflationary pressures are cooling, potentially paving the way for the RBA to deliver another rate cut later this year.

According to the minutes of the RBA’s May 20 monetary policy meeting, the board acknowledged that inflation had “eased significantly” and that global economic risks could prompt a need for further stimulus. Domestic growth remains soft, particularly in consumer spending, while household confidence continues to hover near multi-year lows.

However, the RBA also noted lingering risks that could complicate further cuts. The end of federal energy subsidies is expected to push electricity costs higher, and tight labour market conditions are sustaining solid wage growth — both of which may feed into renewed price pressures later in the year.

As a result, economists remain divided on whether the central bank will deliver another reduction in the cash rate before the end of 2025. Many expect at least one more 25-basis-point cut, which could bring the official rate down from its current 3.85%, though the timing remains uncertain.

For borrowers, that uncertainty highlights the importance of choosing the right mortgage structure and knowing how to position yourself, whether rates move down or hold steady.

Fixed Rates Fall to Three-Year Lows

There’s growing competition among lenders as they adjust to shifting market expectations. Several banks and non-bank lenders are now offering fixed-rate home loans starting with a “4”, a milestone not seen in more than three years.

That’s a notable shift from early 2024, when most fixed-rate products began in the mid-5s or higher. Meanwhile, variable rates remain anchored in the mid-to-high 5% range, meaning fixed loans have become the more affordable option — at least for now.

So, does that mean it’s time to fix your rate? The answer depends on your financial situation and future outlook.

Here’s what to consider:

1. Potential for more RBA cuts.

If the RBA does cut again later in 2025, only variable-rate borrowers would benefit immediately, as fixed loans would remain locked at current levels. However, further cuts could drive fixed rates even lower, particularly if lenders expect longer-term stability.

2. Rate differentials remain narrow.

Since January 2024, lenders have generally priced new fixed loans lower than variable loans, according to RBA data. That’s unusual and suggests fixed rates could rise again once the market stabilises.

3. Flexibility vs certainty.

Variable loans typically offer more features such as offset accounts, redraw facilities, and extra repayment flexibility, which can help borrowers get ahead on their loans. But for those prioritising budget certainty amid cost-of-living pressures, locking in a fixed rate might offer valuable peace of mind.

Ultimately, the right choice depends on your personal goals and risk appetite. Whether you’re refinancing, purchasing, or simply reviewing your existing mortgage, it’s worth comparing rates across the market before deciding.

If you’d like a personalised breakdown of current offers and forecasts, RateSeeker can help you find the best rate suited to your needs.

Rental Growth Continues Nationwide

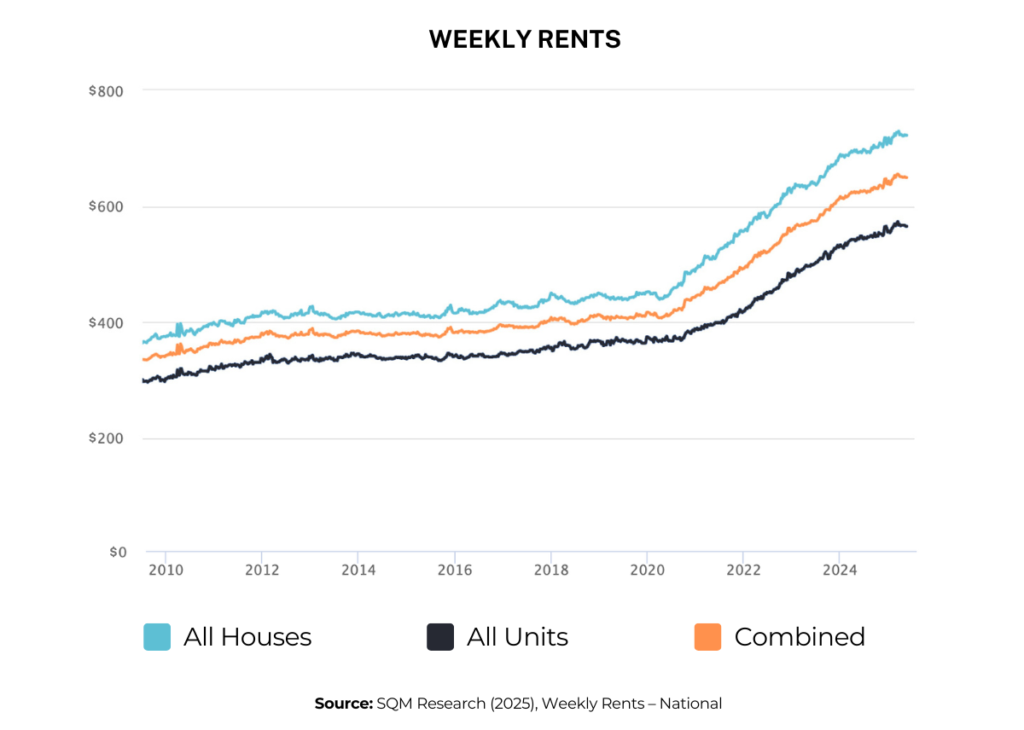

Australia’s rental market remains one of the most talked-about segments of the housing sector, with prices continuing to climb despite broader signs of economic slowdown.

According to SQM Research, national median rents increased 4.2% in the year to June 12, extending the steady upward trend that began in 2021. While that growth rate is slower than the double-digit surges seen in 2023, it still adds pressure for tenants facing rising living costs.

At the same time, property investors are benefiting from higher gross rental yields, supported by limited supply and sustained demand in major cities. In some regional areas and outer suburbs, yields have reached their strongest levels in nearly a decade.

For renters, the ongoing squeeze underscores the importance of planning ahead if you’re considering buying your first property.

Here are three practical steps to prepare for homeownership in today’s market:

1. Build your deposit strategically.

The more you can save upfront, the wider your buying options will be and the less you’ll need to borrow. Setting aside even small amounts consistently can make a big difference over time.

2. Be flexible with your expectations.

While your dream home may be out of reach initially, entering the market through a smaller property or a different suburb can help you start building equity sooner.

3. Understand your borrowing capacity.

Before making any moves, it’s crucial to know how much you can realistically afford. A mortgage broker can help you calculate your borrowing power and explore options to increase it.

For existing homeowners, this same market dynamic could represent an opportunity. With property prices and rents rising in tandem, investors may be able to leverage existing equity to purchase additional properties, expanding their portfolios while maximising income potential.

If you’re weighing up your next step, a professional mortgage adviser can help you determine how to use your equity most effectively, ensuring your finance strategy aligns with your long-term goals.

Five Steps to Succeed at Tax Time

The end of the financial year often brings mixed emotions, it’s a time for both reflection and preparation. Whether you’re a homeowner, landlord, or first-time investor, tax time offers a valuable opportunity to review your finances and ensure you’re making the most of available deductions.

Here are five simple ways to stay ahead:

1. Organise your documents early.

Gather all relevant records, including loan statements, interest summaries, property management reports, and receipts for deductible expenses. Having everything ready streamlines your accountant’s work and reduces errors.

2. Keep your details current.

Make sure your contact and bank details are up to date with both your lender and the myGov platform to avoid processing delays.

3. Check your eligible deductions.

If you own an investment property, you may be able to claim expenses such as repairs, maintenance, insurance, council rates, and loan interest. Even depreciation on fittings and fixtures can add up to meaningful savings.

4. Seek professional guidance.

Tax laws evolve regularly, and professional advice ensures you’re claiming what you’re entitled to while staying compliant with ATO requirements.

5. Plan ahead for FY26.

Tax time isn’t just about the past year, it’s also an opportunity to set financial goals for the year ahead. Whether that’s refinancing for a lower rate, expanding your portfolio, or paying down more debt, strategic planning can position you for long-term growth.

Taking these proactive steps now can help you minimise stress, maximise deductions, and enter FY26 with clarity and confidence.

Final Word

The new financial year is off to a steady start, with the property market showing cautious optimism amid broader economic uncertainty. Inflation remains within target, fixed rates are trending lower, and rental markets continue to present opportunities for both investors and aspiring homeowners.

While challenges remain, particularly around affordability and future rate direction, informed decisions and strategic planning can help you stay ahead of the curve.At RateSeeker, we’re committed to helping Australians make smarter mortgage and investment choices. Whether you’re looking to refinance, invest, or buy your first home, speak to one of our mortgage specialists to guide you through the latest market movements and secure the most competitive rates available.

** General Advice Warning

The information provided on this website is general in nature only and it does not take into account your personal needs or circumstances into consideration. Before acting on any advice, you should consider whether the information is appropriate to your needs and where appropriate, seek professional advice in relation to legal, financial, taxation, mortgage or other advice.