Rateseeker Round-Up: August Business News

August has brought a fresh wave of economic updates, shaping the outlook for Australian households and businesses alike. While inflation is easing and wages continue to outpace price growth, questions remain about the sustainability of these gains and how they flow through to property markets, refinancing activity, and broader business conditions.

At the same time, investor participation in housing continues to trend upwards, though at a slower pace than earlier in the year. New home sales remain resilient despite a modest monthly dip, and refinancing volumes are holding at historically high levels. Beyond property, businesses are grappling with changes to fuel tax credits, the cost pressures of construction, and global trade uncertainties.

This month’s business round-up explores these developments in detail, highlighting what they mean for households, businesses, and investors heading into the final quarter of 2025.

Inflation Eases, Borrowing Conditions Supportive

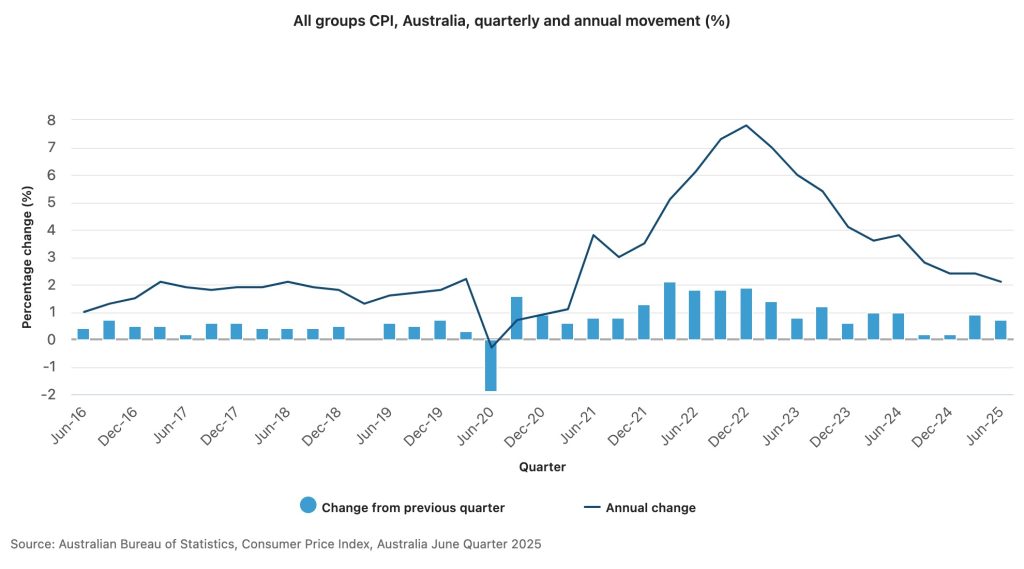

The Australian Bureau of Statistics (ABS) reported that consumer prices rose 2.1% in the year to June 2025, well within the Reserve Bank of Australia’s 2–3% target band. This marks the slowest annual pace of inflation in nearly four years, down from 3.8% a year earlier.

With inflation moderating and long-term expectations stable, the RBA has kept its cash rate on hold in recent months. While some analysts speculate that a further cut could be on the horizon, the central bank has so far signalled cautious optimism rather than aggressive easing.

For households, this backdrop creates a supportive environment. Even without a fresh rate cut, lower-than-expected inflation has improved real borrowing conditions. When combined with steady wage growth, families are finding themselves with slightly more room in their budgets — an encouraging sign after several years of pressure from rising living costs.

According to PropTrack economist Angus Moore, a 0.50 percentage point change in the cash rate can shift borrowing capacity by around 5%. That means a family looking at a $700,000 property could see an additional $35,000 in borrowing room from such a move. While no new cuts have yet materialised, the possibility of future easing is enough to keep market sentiment buoyant.

Refinancing Holds at Elevated Levels

Refinancing continues to be a key trend across the mortgage market. According to the ABS, new loan commitments for owner-occupiers (excluding refinancing) totaled $54.7 billion in the June quarter 2025. While slightly down from its 2022–2023 peaks, this remains a historically high level, underscoring how actively households are managing their loans.

Borrowers are refinancing for a variety of reasons:

- To secure sharper interest rates.

- To switch between fixed and variable products.

- To access equity for renovations or investment.

- To consolidate debts and simplify repayments.

Mortgage brokers are playing a crucial role in this process. With lenders offering diverse products and criteria, broker guidance helps households navigate fees, policies, and potential pitfalls. For many families, professional advice has been the difference between marginal savings and significant long-term financial gains.

It’s worth noting, however, that the pace of refinancing has moderated. Compared to the surging growth rates seen in 2022 and early 2023, refinancing activity has levelled out.

For households, this suggests that while opportunities remain, the biggest refinancing rush may be behind us. Still, with interest rates steady and inflation easing, many borrowers continue to find value in reviewing their mortgage arrangements.

New Home Sales: Strong Despite Monthly Dip

The Housing Industry Association (HIA) reported that new home sales fell 6.4% month-on-month in July 2025, following a surge in June driven by end-of-financial-year promotions. Despite this dip, sales remain 15.9% higher over the three months to July compared with the previous quarter, the strongest activity since late 2022.

This resilience reflects continued demand for family-friendly homes, particularly in suburban growth corridors where new-build supply remains robust. Builders note that rising construction costs from materials to labour are creating challenges, but consumer appetite has not diminished significantly.

For households considering a new build, understanding construction finance remains critical. Unlike traditional mortgages, construction loans release funds in stages, require progress inspections, and typically charge interest only on drawn amounts during the build phase. Once completed, the loan converts to a standard mortgage.

This staged approach helps families manage cash flow throughout the construction period, but it also requires careful planning. Delays, cost overruns, or unexpected design changes can put pressure on budgets. Working with experienced builders and financial advisers helps ensure projects remain on track.

Investor Lending: Momentum Slows but Still Strong

Investor activity has been one of the standout themes of the past 18 months. ABS lending data shows that in the June 2025 quarter, investor loan commitments rose 3.5% compared to March, marking the highest quarterly level since 2017. In value terms, this amounted to $32.9 billion in new investor loans.

On a year-on-year basis, however, growth has slowed significantly, with commitments just 0.8% higher than June 2024. This suggests that while investor momentum remains strong, it may be reaching a more stable plateau after a period of rapid expansion.

For households, investor presence has a mixed impact. On the one hand, investors help supply the rental market, which remains under immense pressure. On the other, increased investor demand for properties can tighten availability and push prices higher in certain suburbs.

Industry economists, including PropTrack’s Angus Moore, emphasise that investor lending has steadily climbed since mid-2023, and their participation is now a defining feature of the market. Families seeking to buy should consider this context when choosing where to purchase, as investor competition is often concentrated in rental hotspots.

Wages Outpacing Inflation

The ABS Wage Price Index (WPI) showed annual wage growth of 3.4% in the year to June 2025, down from about 4.1% in June 2024.

Inflation, as measured by the CPI, stood at 2.1% for the same period.

With wages rising faster than consumer prices, there is modest real wage growth offering households some relief from cost-of-living pressures.

Meanwhile, ABS data for average weekly ordinary time earnings show full-time adult workers earned about AU$2,010 per week in May 2025, a 4.5% year-on-year increase.

It’s worth noting that different measures capture different aspects of the labour market: earnings vs wage inflation, public vs private sector, etc., so outcomes vary across industries.

Economists caution that without productivity improvements, these gains may be harder to sustain. Rising wages without matching gains in output risk adding inflationary pressures, especially if cost pressures elsewhere remain strong.

For households, the higher wages give a bit more room to save, invest, or manage rising mortgage or rental costs. For businesses, the challenge is balancing wage pressures with efficiency and competitiveness into 2026.

Fuel Tax Credit Changes

Two recent changes to fuel tax credit (FTC) rates are affecting businesses:

- July 1, 2025: The road user charge for heavy vehicles increased, reducing FTC entitlements for eligible users.

- August 4, 2025: Rates were adjusted again in line with CPI movements, reflecting changing economic conditions.

The Australian Taxation Office (ATO) advises that businesses making claims under $10,000 annually can use the rate applicable at the end of their BAS period. Larger claimants must apply rates more precisely.

For transport operators, agriculture businesses, and construction firms, these changes highlight the need for accurate record-keeping. Proper apportionment of fuel use, timely BAS lodgements, and professional guidance can help businesses maximise entitlements while staying compliant.

Trade Tensions: Australia Avoids Further US Tariffs

On the global stage, Australia has avoided additional tariff hikes from the United States this quarter. While this is a relief for exporters, existing 10% tariffs remain in place, continuing to weigh on some industries.

The Australian Chamber of Commerce & Industry (ACCI) described the outcome as “the best we could have expected” but emphasised that the tariffs are unjustified, given Australia imposes no equivalent duties.

Industry groups continue to press for fairer trade terms and warn that US–China tensions may indirectly impact Australia, particularly in commodity markets such as iron ore and coal. Businesses reliant on exports will need to remain agile, with diversification strategies becoming increasingly important.

Final Thoughts

August’s business news paints a picture of cautious optimism. Inflation is easing, wages are outpacing prices, and households are actively refinancing to manage their mortgages. Investor lending remains robust, and new home sales continue to show resilience.

At the same time, challenges persist. Productivity growth is lagging, rental markets remain tight, and businesses face cost pressures from construction to fuel. Global trade uncertainty adds another layer of complexity.

For households, this is a moment to plan strategically:

- Borrowers should review their mortgage options in light of stable but historically low rates.

- First-home buyers should balance optimism about borrowing power with careful budgeting.

- Investors should watch for potential supply-demand shifts in key rental markets.

For businesses, the focus should be on efficiency, compliance, and adaptability. From wage negotiations to fuel claims and export strategies, staying informed and proactive will be essential.

If you’d like tailored advice on how these developments could impact your household or business finances, the Rateseeker team is here to help you make confident, informed decisions.

Disclaimer: This content is for general informational purposes only and does not constitute financial advice. Readers should consider their own circumstances and seek professional guidance before making financial decisions.

** General Advice Warning

The information provided on this website is general in nature only and it does not take into account your personal needs or circumstances into consideration. Before acting on any advice, you should consider whether the information is appropriate to your needs and where appropriate, seek professional advice in relation to legal, financial, taxation, mortgage or other advice.