Rateseeker Round-up: February Property News

February’s here, and the property market is already stirring with movement, along with a few surprises. While investors are quietly stepping back, owner-occupiers are making a confident comeback. Loan sizes are pushing new highs, government reforms are shaking up lending rules, and more Aussies are finding creative ways to break into the market despite the rising bar for affordability.

Throw in a record year for new car purchases and a growing appetite for personal lending, and it’s clear that people are spending again, but they’re being strategic about it.

This month’s update breaks down what’s changing, what it means for buyers and borrowers, and how you can position yourself smartly in a shifting landscape. Whether you’re planning your next move or just watching from the sidelines, now’s a good time to take stock. Let’s get into it.

Owner-Occupiers Step Up as Investor Activity Eases

There has been a noticeable shift in the property market dynamics as we settle into the new year. Owner-occupiers are becoming more active, while investors appear to be pulling back.

Fresh ABS data shows that in the final quarter of 2024, loan commitments from investors dropped by 4.5%, while commitments from owner-occupiers rose by 2.2%. It’s a trend that reflects growing confidence among everyday buyers, especially as interest rate relief looks more likely this year.

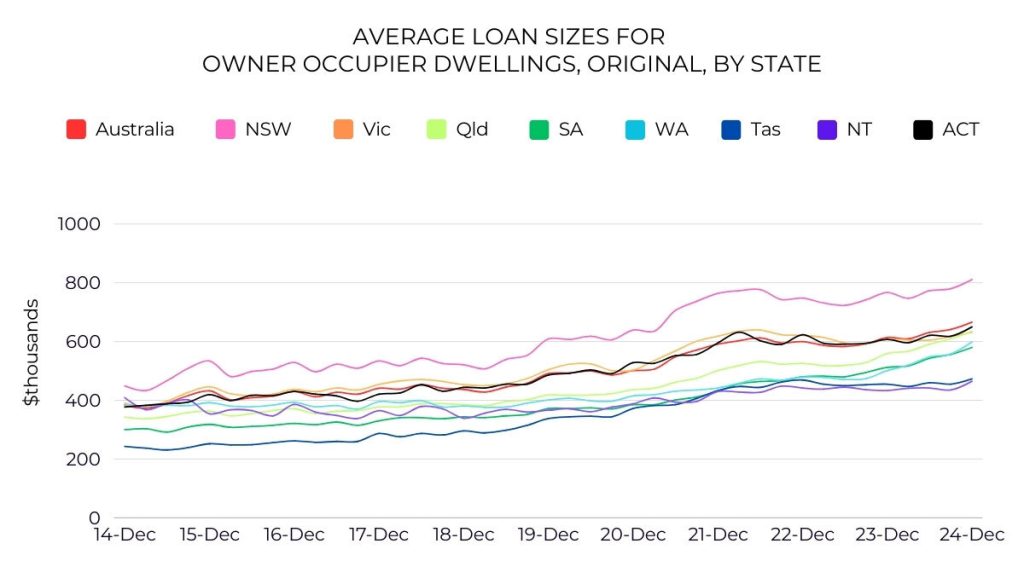

At the same time, the average mortgage size across Australia reached a record $666,000, which is 8.5% higher than the previous year. Breaking it down further, loan sizes ranged from $465,000 in the Northern Territory to $811,000 in New South Wales, highlighting just how varied the borrowing landscape is across the country.

Naturally, larger loan sizes mean bigger deposits, and for many buyers, that’s one of the biggest hurdles. If you’re trying to bridge the gap, there are a few smart strategies to help make your deposit more manageable:

- Consider low-deposit lending options, including those with less than 20% down

- Ask family about a guarantor loan, which could reduce your required deposit to 5% or even 0%

- Team up with a partner, friend or family member to combine deposits and buying power

- Look into the Home Guarantee Scheme, which lets eligible buyers purchase with just a 5% deposit and no LMI

- Step up your savings plan by reviewing your budget and finding ways to increase income or reduce spending

With the right advice and a well-structured strategy, buying in 2025 is still within reach, even if saving that deposit feels like a challenge.

New Ban Targets Overseas Property Investors

In a bold move to ease housing pressure, the federal government has announced a temporary ban on foreign investors buying established residential properties in Australia. The two-year ban will run from April 1, 2025, to March 31, 2027, with a review scheduled at the end to assess whether it should be extended.

At the moment, foreign buyers are typically restricted to purchasing newly built properties. However, they’ve been allowed to buy established homes in limited situations, something the government now wants to tighten up as part of its broader housing strategy.

The message is clear: the priority is getting more homes into the hands of local buyers.

In addition to the purchase ban, the government is also cracking down on illegal land banking, where foreign investors buy up vacant land, leave it untouched, and then flip it for profit without meeting development requirements. To ramp up enforcement, the Australian Taxation Office will receive extra funding to audit and monitor foreign investor activity.

This is all about easing pressure on our housing market at the same time as we build more homes. These initiatives are a small but important part of our already big and broad housing agenda.

Clare O’Neil – Housing Minister

While this change won’t solve housing shortages overnight, it aims to give Australian buyers more breathing room and ensure that land purchased by overseas investors is put to good use.

Big Changes Ahead for Home Buyers with HECS Debt

Good news could be on the way for Australians juggling student debt and home ownership dreams.

Treasurer Jim Chalmers has called on financial regulators to ease the rules around how student loans, like HELP or HECS debts, are factored into home loan applications. Currently, lenders are required by regulators (APRA and ASIC) to include student loan repayments when assessing your borrowing capacity, which can reduce how much you’re eligible to borrow.

But under the proposed changes, banks may soon be allowed to exclude HELP debt from serviceability calculations if the borrower is likely to repay it in the near term, according to reporting by the Australian Financial Review.

I’ve agreed these changes in discussions with regulators and convened the banks to discuss them. People with a HELP debt should be treated fairly when they want to buy a house, and we’re working with the regulators to make sure they are.

Jim Chalmers – Treasurer

While there’s no set timeline for when these changes will kick in, this shift could make a real difference, especially for younger buyers or anyone close to clearing their student loans.

Keen to find out how your HELP debt is affecting your borrowing power, or what these changes might mean for your home loan plans? Reach out to our expert loan strategists at Rateseeker and let’s crunch the numbers together.

From Cars to Getaways, Aussies Borrow Big

Australians hit the accelerator on new car purchases in the last year, with record-breaking sales driving a sharp rise in consumer lending.

According to the Federal Chamber of Automotive Industries, 1,220,607 new vehicles were sold last year, the highest annual total ever recorded. Not surprisingly, some of the top-selling brands were familiar favourites: Toyota, Ford, Mazda, Kia, and Mitsubishi all maintained strong market positions, appealing to both first-time buyers and long-time loyalists.

To support this surge in car ownership, consumers borrowed a massive $4.7 billion in the December 2024 quarter alone, up 13.0% year-on-year, according to the Australian Bureau of Statistics. That figure marks a new high for the car loan market, reflecting growing consumer confidence and a clear willingness to invest in personal transport.

But the borrowing boom wasn’t just limited to vehicles. Personal loans for holidays, household goods, and other discretionary spending jumped by 25.9%, reaching a record $3.9 billion. Whether it was overseas travel, new furniture, or long-postponed upgrades, it’s clear many Aussies were keen to enjoy life a little more after years of cost-of-living pressures.

So, what does this mean for you?

If you’re thinking about buying a car or funding a larger personal purchase, it’s important to explore all your financing options. While credit cards are often the default, car loans and personal loans typically come with lower interest rates, fixed repayment plans, and clearer end dates, which can make budgeting easier and costs more manageable over time.

Every situation is different, and the right loan depends on your goals, timeline, and financial profile

Whether you’re eyeing your next property, planning a big-ticket purchase, or simply looking to make smarter moves with your money this year, having the right guidance makes all the difference.

Get in touch with Rateseeker today and let’s talk about how we can help you reach your financial goals, smarter, sooner, and with confidence.

** General Advice Warning

The information provided on this website is general in nature only and it does not take into account your personal needs or circumstances into consideration. Before acting on any advice, you should consider whether the information is appropriate to your needs and where appropriate, seek professional advice in relation to legal, financial, taxation, mortgage or other advice.