Rateseeker Round-up: April Property News

As we roll into April, the Australian property market is showing a mix of steadiness and shifting undercurrents. Prices across most capital cities nudged upward through March, with regional areas still holding their ground. Despite ongoing affordability challenges, auction clearance rates in places like Sydney and Melbourne stayed surprisingly solid, another sign that buyer interest is still out there.

On the economic front, there’s been more positive movement. Inflation has now stayed within the Reserve Bank’s 2 to 3 per cent target for seven months in a row. That’s encouraging news, especially after the rapid rate rises of the past few years. With inflation cooling, there’s now growing talk that the RBA could start easing interest rates later in the year, though global uncertainty is still very much part of the conversation.

Interestingly, the RBA’s latest Financial Stability Review paints a pretty reassuring picture for borrowers. About 97 per cent of mortgage holders are still managing repayments without falling behind, and most have built up equity in their homes. Even if prices took a hit, the majority would still be in a strong position.

For investors, though, the landscape has become a bit more challenging. Around two-thirds are now negatively geared, meaning their rental income isn’t covering rising loan costs. It’s not unexpected given the rate environment, but it does highlight the importance of good planning and the need to stay on top of cash flow.

On the construction side, there’s finally some relief. Building cost growth slowed to its lowest level in 15 years during the March quarter. That’s welcome news for anyone thinking about building, although costs are still much higher than they were a few years ago. Labour shortages and supply constraints remain a hurdle, but with nearly 500 cranes still up across the country, there’s clearly a lot of building still underway.

In this month’s update, we’re unpacking all of this, from borrowing and inflation to investing and construction. Whether you’re looking to buy, build, or just stay informed, this will help you make decisions with a clearer view of the market.

Most Aussie Borrowers Are Well-Placed to Weather Economic Storms, Says RBA

In a reassuring update for homeowners and potential buyers, the Reserve Bank of Australia (RBA) has confirmed that most home loan customers are financially resilient, even in economic headwinds.

According to the RBA’s latest Financial Stability Review, most borrowers remain in a strong position, capable of meeting their mortgage repayments under various economic scenarios. In fact, around 97% of borrowers are currently cash flow positive, meaning they not only meet their regular loan commitments but may even be getting ahead on their mortgages.

Another promising insight is that less than 1% of borrowers are in negative equity, a substantial improvement compared to pre-pandemic levels. Negative equity occurs when the value of a property falls below the outstanding loan balance, so this drop indicates a healthier, more stable property market overall.

The RBA noted that households have built up significant buffers in both liquidity and equity, allowing them to ride out unexpected rises in interest rates, inflation, or even a sharp down in the job market.

Perhaps most striking, the RBA’s stress testing suggests that nine out of ten borrowers would still maintain positive equity even in a severe scenario where property values drop by 30%. While selling a home under stress is far from ideal, this equity provides a critical safety net for homeowners facing financial hardship.

Of course, no two financial situations are the same. If you’re finding it challenging to stay on top of your mortgage, talking to a mortgage broker or your lender early can make all the difference. A trusted professional can help you explore your options and potentially avoid long-term financial strain.

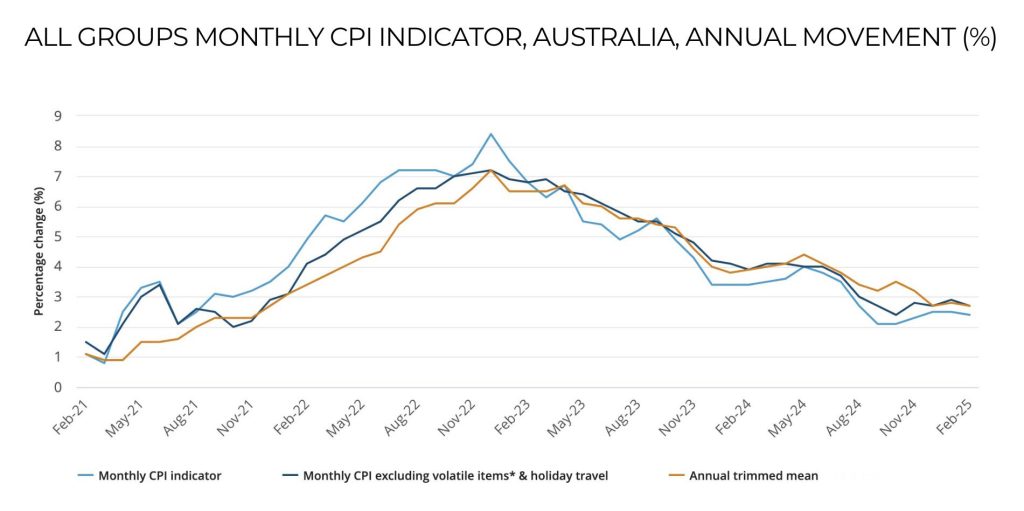

Inflation Stays Within RBA’s Target: Could a Rate Cut Be on the Horizon?

Australia’s inflation outlook just took another encouraging step forward, at least for now.

According to the latest data from the Australian Bureau of Statistics (ABS), headline inflation eased slightly in February, dropping to 2.4 per cent from 2.5 per cent the month before. That makes it the seventh straight month that inflation has remained within the Reserve Bank of Australia’s (RBA) target band of 2 to 3 per cent, a significant signal that price pressures may finally be cooling.

Notably, the trimmed mean inflation rate, which the RBA relies on more heavily due to its ability to filter out volatile price movements, also ticked down from 2.8 per cent to 2.7 per cent. That marks the third month it has sat comfortably within target.

So, what does this mean for interest rates?

After three years of maintaining relatively high interest rates to curb spending and tame inflation, the RBA might now be warming up to the idea of a rate cut. If the central bank feels confident that inflation is firmly under control, it could move to lower the cash rate at its upcoming monetary policy meeting in May. This decision would likely encourage lenders to reduce mortgage rates in turn.

But here’s the twist: global uncertainty may throw a wrench in those plans.

The inflation figures were recorded before the United States announced a new round of tariffs, which could inject instability into the global economy and raise inflationary risks. With that in mind, the RBA may tread cautiously, weighing both domestic progress and international threats before making any significant moves.

Whether you are a current homeowner or prospective buyer, staying informed and prepared is more important than ever. Speak to your mortgage broker to understand how a potential rate cut or ongoing rate stability could affect your borrowing strategy in the months ahead.

Two-thirds of Property Investors Are Negatively Geared

Property investment continues to be a powerful strategy for building long-term wealth, but it is not without its challenges. One of the most common early hurdles? Negative gearing.

Recent research from the Property Investment Professionals of Australia (PIPA) has revealed that 65 per cent of property investors were negatively geared in 2024, a notable increase from 57 per cent in 2023. That means two out of every three investors spend more on property expenses, including loan interest, than they earn from rental income.

PIPA chair Nicola McDougall noted that these results highlight the dual nature of property investment.

Interest rates remain significantly higher than they were a few years ago, and while rents have risen, they are a drop in the ocean compared to higher lending costs, she said.

So, what does this mean if you are already investing or thinking of starting?

Negative gearing is common, especially when owning an investment property early. While tax benefits and long-term capital growth can offset it, it also requires strong financial planning. Here are five smart ways to manage your position:

- Build a cash buffer to help cover periods of negative cash flow

- Budget for the possibility of future rate increases

- Partner with a qualified accountant to maximise your tax deductions

- Review your loan regularly to make sure it remains competitive

- Talk to a mortgage broker about refinancing or restructuring options

Whether you want to purchase your first investment or ensure your current loan structure works for you, now is a great time to seek expert guidance. Reach out to discuss your options and get personalised support for your financial goals at Rateseeker.

Homebuilding Cost Growth Slows to Lowest Level in 15 Years

There is some welcome news for aspiring homeowners and builders alike. The pace of residential construction cost increases has slowed to its lowest level in over a decade.

According to the Cordell Construction Cost Index, construction costs rose by just 0.4 per cent in the March quarter of 2025. This marks the smallest quarterly increase since 2010. As a result, annual cost growth has eased from 4.0 per cent in the December quarter to 3.4 per cent in March.

While this moderation is encouraging, it is essential to keep things in perspective. Building costs have surged by a staggering 31.3 per cent since the onset of the pandemic in March 2020. In that context, today’s slower growth starts from a very high base.

Challenges in the construction sector remain. Builders face elevated supply costs and an ongoing shortage of skilled tradespeople. Even so, homebuilding activity remains strong across the country.

Multinational construction consultancy RLB reported that 487 residential construction cranes were active during the first quarter of 2025. That figure is 9.8 per cent lower than the 540 cranes counted a year earlier, but it still represents a historically high activity level.

If you’re thinking about building a home, now could be a good time to explore your options.

Need more advice? Contact us at Rateseeker. We can help you secure a pre-approval for a construction loan so you can confidently plan your budget.

** General Advice Warning

The information provided on this website is general in nature only and it does not take into account your personal needs or circumstances into consideration. Before acting on any advice, you should consider whether the information is appropriate to your needs and where appropriate, seek professional advice in relation to legal, financial, taxation, mortgage or other advice.