Rateseeker Round-Up: December Property News

As we end the year, there’s a lot to unpack in the property market right now. Rising interest rates have had a big impact, slashing borrowing capacity by 40% since 2022 and making it tougher for buyers to secure loans.

At the same time, more homebuyers are turning to mortgage brokers, with nearly 75% of new loans now coming through brokers rather than banks—because they offer more options and better opportunities to save, especially when refinancing.

There’s also some exciting news for low- and middle-income earners with the introduction of the Help to Buy scheme, which lets eligible Australians purchase property with as little as a 2% deposit. And if you’ve been waiting to jump into the market, recent data shows that 2025 could be your year, as buyers are gaining more negotiating power while sellers face increasing pressure to adjust prices.

With so much happening, staying informed is key. Explore all the insights and tips you need to confidently navigate today’s property market.

Why 2025 Could Be Your Year to Enter the Property Market

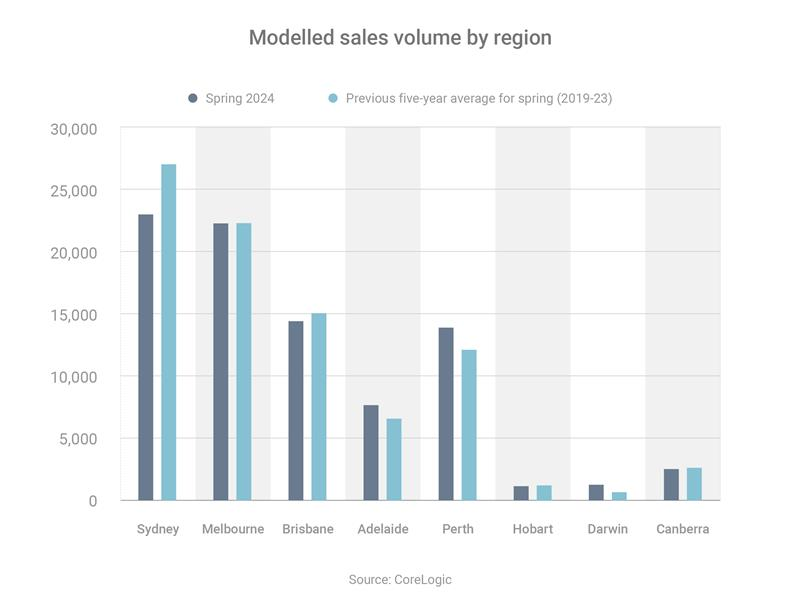

The Australian property market is beginning to tilt in favour of buyers, with recent data signalling promising conditions for those looking to purchase in early 2025. According to CoreLogic, the 2024 spring selling season saw sales volumes drop 4% below the spring average from 2019 to 2023. Additionally, the median time to sell a home has increased from 28 to 32 days between the August and November quarters.

This shift suggests a growing challenge for sellers, who now face more competition to secure buyers. With properties sitting on the market longer, there is increasing pressure on vendors to reduce asking prices to close deals. For buyers, this translates into stronger negotiating power and potential price reductions as we approach 2025.

What’s Driving These Buyer-Friendly Conditions?

1. Decreased Sales Activity

The drop in spring sales volumes highlights a cooling market. While demand remains steady, higher interest rates and affordability challenges have tempered buyer activity, giving existing buyers more leverage.

2. Longer Selling Times

The increase in days on the market suggests that properties are not selling as quickly as before. This could be due to higher vendor expectations clashing with buyers constrained by borrowing capacity in a high-interest-rate environment.

3. Competitive Vendor Dynamics

With more sellers vying for a smaller pool of buyers, vendors are more likely to adjust their prices or offer incentives to attract attention. For buyers, this creates opportunities to negotiate better deals, particularly in markets where supply is higher than demand.

How to Prepare for Buying in 2025

If you’re thinking about taking advantage of these conditions, preparation is key. Here’s how to position yourself for success:

- Boost Your Savings: Increasing your deposit not only enhances your borrowing capacity but also helps you avoid lenders’ mortgage insurance (LMI). Use automated savings apps or review your monthly expenses to free up funds.

- Don’t Spend Big: Big-ticket expenses, such as a car or luxury items, can impact your credit score and reduce your ability to secure a favourable loan. Hold off until after your property purchase.

- Improve Your Credit Score: Your credit score plays a significant role in loan approval and interest rates. Pay all bills on time, reduce outstanding debt, and check your credit report for errors.

- Maintain Employment Stability: Lenders typically prefer applicants who have been in the same role for at least six months. Staying put in your current position can strengthen your application.

- Secure Pre-Approval: Knowing your borrowing capacity is critical. At Rateseeker, our priority is to help you find a loan that works for your circumstances. We can help get you pre-approved for a home loan, giving you clarity and confidence when negotiating.

According to CoreLogic, metropolitan areas like Sydney and Melbourne are still experiencing higher-than-average property prices, but regions such as Brisbane and Perth offer more affordable entry points for buyers. Additionally, as interest rates stabilise or potentially decline in 2025, borrowing capacity may increase, encouraging more buyers to enter the market.

For prospective buyers, 2025 presents an exciting opportunity to secure property in a market that increasingly favours negotiation. By preparing your finances, understanding market dynamics, and staying informed, you can take full advantage of these favourable conditions.

If you’re ready to take the next step, contact us at Rateseeker for personalised advice and home loan pre-approval. Let’s make 2025 your year to achieve your property goals!

Help to Buy: A New Path to Homeownership for Low- and Middle-Income Australians

For Australians struggling to break into the property market, a new initiative is set to provide a game-changing opportunity. The federal parliament has passed legislation for Help to Buy, a scheme designed to make homeownership more accessible for lower- and middle-income earners.

Here’s how it works:

- Eligibility: Individual buyers earning less than $90,000 per year or joint buyers with a combined income of less than $120,000 qualify.

- How It Works: Buyers partner with the government, which takes an equity stake in the property—up to 30% for established homes or 40% for new builds. This stake reduces the buyer’s required financial contribution.

- Property Price Caps: These vary by location, from $450,000 in regional areas of WA, SA, and Tasmania to $950,000 in Sydney.

- Minimal Deposit: Buyers will need only a 2% deposit, and they’ll avoid paying lenders’ mortgage insurance (LMI).

- Conditions: Buyers must be Australian citizens, not own any other property, and intend to live in the home.

When the property is sold, the government recoups its proportional share of the sale price based on its equity stake.

What’s the Catch?

While Help to Buy has been approved at the federal level, participation by states remains pending. Each state must pass its own supporting legislation to join the program. Currently, the scheme applies to the ACT and Northern Territory, with other states ideally joining by 2025, depending on their timelines.

What This New Scheme Means for Buyers

Help to Buy offers a practical way for eligible Australians to enter the property market sooner, with reduced financial barriers. However, the scheme’s price caps mean buyers must carefully research properties within their local limits. It’s also important to consider the implications of the government’s equity stake, especially if property values rise significantly over time.

This program could be a golden ticket to homeownership for those eligible—stay informed as your state’s participation evolves!

How Rising Interest Rates and APRA’s Buffer Impact Borrowing Power

Rising interest rates are making it increasingly difficult for Australians to qualify for larger loans—or even secure loans at all. According to PropTrack senior economist Paul Ryan, every 0.50 percentage point increase in interest rates reduces the average person’s borrowing capacity by about 5%. Since 2022, the Reserve Bank of Australia has raised official interest rates by 4.25 percentage points, leading to a staggering 40% reduction in borrowing capacity for the average borrower.

Could Borrowing Power Improve?

If the RBA begins cutting rates in the future, borrowing capacities will naturally rise. But there’s another way this could happen even sooner: through changes to the mortgage serviceability buffer.

This buffer, mandated by the Australian Prudential Regulation Authority (APRA), requires lenders to assess borrowers’ ability to repay loans at a rate of 3 percentage points higher than their actual loan interest rate. For example, if you apply for a loan with an interest rate of 6.20%, the lender evaluates your capacity to repay it as if it were 9.20%.

If APRA were to reduce the buffer to 2.5% or 2%, it would increase borrowers’ purchasing power, as lenders would apply a lower assessment rate. This change could provide some relief to homebuyers struggling with high rates.

APRA Holds Steady at 3%

Despite speculation that APRA might lower the buffer, the regulator recently confirmed that it would remain at 3 percentage points. APRA cited several reasons for maintaining this stance:

- High Household Debt: Many Aussies are already carrying significant debt loads.

- Cost-of-Living Pressures: Persistent inflation is straining household budgets.

- Weakening Jobs Market: Rising unemployment could impact borrowers’ ability to make repayments.

- Geopolitical Risks: Global uncertainty adds another layer of caution for the financial system.

What This Means for Borrowers

In the current environment, borrowing power remains constrained, and potential homebuyers need to plan carefully. While future RBA rate cuts could provide some relief, borrowers should focus on:

- Be Financially Ready: Strengthen your savings and credit profile to maximise your loan eligibility.

- Exploring options with lenders: Some may offer flexibility or competitive terms to offset higher rates.

- Considering timing: Waiting for improved market conditions could be a strategic move if your borrowing capacity is significantly limited.

For now, understanding the factors shaping your borrowing power is essential. Stay informed and get in touch with our experienced loan strategists at Rateseeker, and we can help you navigate the landscape of interest rates in 2025.

Record Number Of Aussies Turning To Mortage Brokers Home Loans

Did you know that nearly 75% of homebuyers now use mortgage brokers to secure their home loans? According to the latest data from Comparator, brokers originated a record-high 74.6% of all new home loans in the September quarter, leaving banks at a record-low 25.4%.

So, why are so many people choosing brokers? It comes down to choice. Brokers compare home loan products from a variety of lenders, tailoring recommendations to your needs. Banks, on the other hand, only promote their own products. This flexibility makes brokers a top choice for both new buyers and homeowners looking to refinance.

Refinancing Could Save You Thousands In The Long Term

Refinancing every few years is a smart strategy, as lenders often reserve their best deals for new customers. In fact, the Australian Competition & Consumer Commission (ACCC) found that borrowers with loans three to five years old paid, on average, 0.58 percentage points more in interest than those with newer loans.

That may not sound like much, but switching to a comparable product with a lower interest rate over the life of your loan could save you tens of thousands of dollars.

Is It Time to Refinance?

If you’ve been in your current home loan for a few years, it’s worth exploring your options. At Rateseeker, we can help crunch the numbers to see how much you could save by switching loans. Whether it’s lowering your repayments or shortening your loan term, refinancing could make a big difference. Contact us today.

** General Advice Warning

The information provided on this website is general in nature only and it does not take into account your personal needs or circumstances into consideration. Before acting on any advice, you should consider whether the information is appropriate to your needs and where appropriate, seek professional advice in relation to legal, financial, taxation, mortgage or other advice.