Rateseeker Property News Round-up October – 2023

As we head towards a hot Aussie summer, the property market has been heating up as well, Aussie homeowners are not shy of getting a better deal. Refinancing has surged to new heights, with borrowers seeking to capitalise on lower interest rates and better loan terms. Recent data from the Australian Bureau of Statistics (ABS) revealed that refinancing exceeded $20 billion, a testament to the financial savvy of property owners in these dynamic times.

Over the past 18 months, interest rates have been on a rollercoaster ride, with fluctuations that have not been seen in years. Understanding the trajectory of interest rates is pivotal for anyone considering a property investment or mortgage refinancing.

The government has rolled out various initiatives to assist first-time buyers in their quest to enter the property market. These measures aim to make the dream of homeownership more attainable and affordable for many Australians.

As the end of the financial year approaches, property owners need to be aware of important tax considerations. Ensuring that you are well-prepared for upcoming deadlines can help you optimise your financial situation.

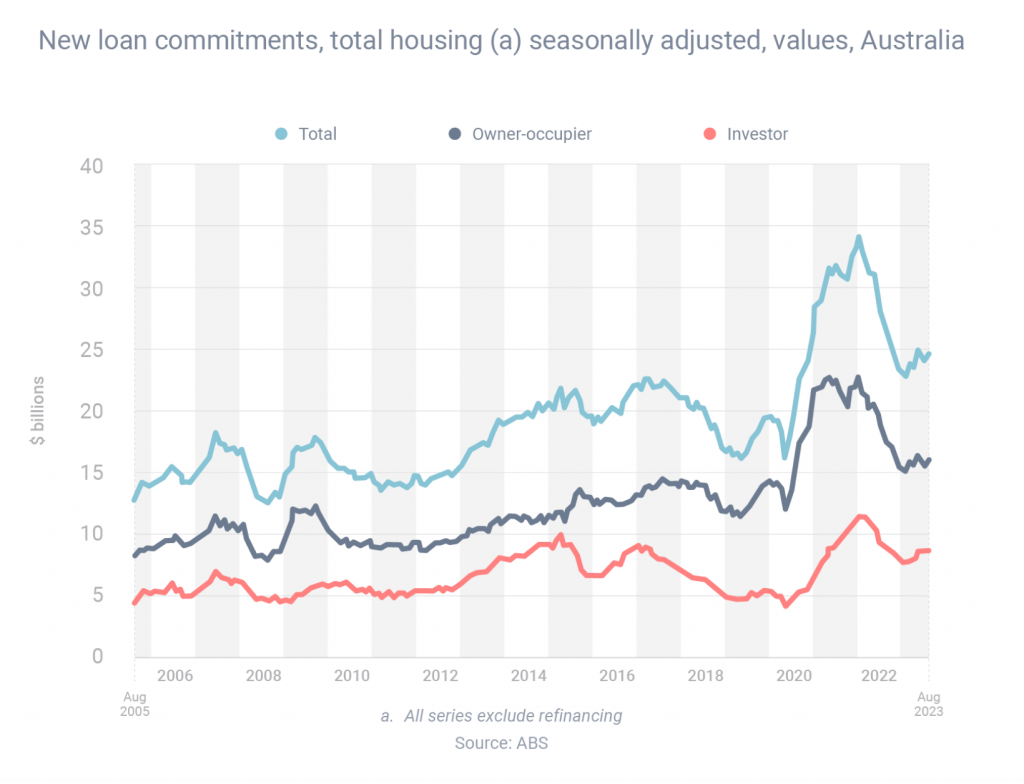

Aussies refinance more than $20 Billion of loans

With a substantial number of individuals transitioning from fixed-rate mortgages at the present moment, it comes as no surprise that a considerable surge in refinancing activities is underway, as borrowers seek to capitalise on lower interest rates.

According to the most recent data from the Australian Bureau of Statistics (ABS), the refinancing volume in August amounted to $20.60 billion. While this figure represented a 3.9% decrease compared to the previous month, it reflected a noteworthy increase of 12.4% when compared to the same month in the previous year.

In the same period, the ABS also reported that the total value of newly committed home loans in August reached $24.82 billion, indicating a 2.2% uptick from the previous month’s numbers.

Breaking down the data, owner-occupier borrowing experienced a 2.6% boost, reaching $16.07 billion, while investor borrowing showed a 1.6% increase, amounting to $8.75 billion.

However, it is important to note that there has been a decline in home loan activity when examining year-on-year trends:

- Total borrowing has decreased by 9.4%.

- Owner-occupier borrowing has declined by 12.5%.

- Investor borrowing has seen a 3.0% decrease.

These trends underscore the evolving landscape of the Australian property and finance market, as borrowers actively navigate their mortgage options to optimise their financial positions amidst changing interest rate dynamics.

The recent shifts in the interest rate landscape have ushered in a wave of change in the mortgage market. As a result, competition among lenders has become incredibly fierce. This heightened competition has paved the way for a multitude of attractive refinancing opportunities, some of which are offered by smaller, lesser-known lenders.

While the larger, more familiar banks have traditionally dominated the mortgage market, these quality smaller lenders have started to emerge as formidable contenders. Their competitive offers can be especially appealing to borrowers seeking to refinance their mortgages, as they often come with favorable terms and competitive interest rates.

Exploring these lesser-known lenders can open up a world of possibilities for those in search of refinancing deals that best suit their financial goals. So, if you’re considering refinancing, it’s worthwhile to look beyond the familiar names in the industry and explore what these smaller, quality lenders have to offer. You might just find the perfect refinancing deal to optimise your financial situation and secure your property’s future.

The evolution of interest rates over the last 18 months

The Reserve Bank of Australia (RBA) has recently released data that sheds light on the impact of its cash rate hikes on the Australian mortgage market.

To assess this impact, a key metric is to compare the average interest rates for all outstanding loans in April 2022, which represents the month just before the first cash rate increase, with August 2023, the most recent month for which comprehensive data is available.

During this period, the RBA implemented a series of cash rate hikes, resulting in a cumulative increase of 4.00 percentage points. However, it’s noteworthy that the average interest rates for outstanding loans did not rise by the full extent of these cash rate adjustments. This divergence is partly attributed to the presence of fixed-rate loans with lower rates that remained unchanged.

For owner-occupied loans, the average interest rates experienced the following increases:

- A 2.82 percentage point rise for principal-and-interest loans.

- A 3.31 percentage point increase for interest-only loans.

This data illustrates that while the RBA’s cash rate hikes have certainly influenced the mortgage market, the actual impact on borrowers varied depending on their loan type and specific terms. These findings underline the importance of understanding the nuances of the mortgage market and choosing the right loan structure to navigate evolving interest rate conditions effectively.

When examining investment loans, the data reveals the following rate increases:

- A 2.83 percentage point upturn for principal-and-interest loans.

- A 2.73 percentage point uptick for interest-only loans.

It’s crucial for investors to take note of these changes, as well as the broader economic indicators, in their decision-making process. The potential for future interest rate hikes looms on the horizon, driven by external factors such as the ongoing conflict in the Middle East. This geopolitical situation has the potential to trigger higher oil prices, subsequently leading to increased petrol costs and elevated inflation levels.

The recent statement from the Reserve Bank of Australia (RBA) highlights their vigilant stance. In their most recent cash rate meeting, the RBA board members acknowledged that “some further tightening of policy [i.e. rate rises] may be required should inflation prove more persistent than expected,” as indicated in the meeting minutes.

This statement underscores the RBA’s readiness to respond to changing economic conditions and its commitment to keeping inflation in check. As such, investors should remain vigilant and consider the potential impact of future rate increases when managing their investment loans and financial portfolios. Staying informed and adapting to evolving market dynamics is essential in making sound financial decisions.

How the federal government is backing first home buyers

A recent report by Housing Australia has shed light on the significant impact of the federal government’s Housing Guarantee Scheme (HGS) and its associated assistance programs in the 2022-23 financial year.

This initiative has played a crucial role in facilitating homeownership for many first-time buyers across the country.

Here’s a snapshot of what the typical participants in these programs looked like, as outlined by Housing Australia:

- First Home Guarantee:

- Median participant age: 30-34 years.

- Household income: $76,000.

- Property purchase price: $459,000.

- Regional First Home Buyer Guarantee:

- Median participant age: 25-29 years.

- Household income: $71,000.

- Property purchase price: $389,000.

- Family Home Guarantee (for single parents):

- Median participant age: 35-39 years.

- Household income: $70,000.

- Property purchase price: $422,000.

These statistics offer valuable insights into the demographics and financial profiles of those benefiting from the HGS and its associated programs. They reflect the diversity of participants and underscore the government’s commitment to providing pathways to homeownership for a broad range of individuals and families.

It’s worth noting that Housing Australia has taken the reins from the National Housing Finance and Investment Corporation, inheriting its responsibilities, including the oversight of the HGS. Moreover, Housing Australia has also assumed control of the National Housing Infrastructure Facility, a crucial entity that plays a pivotal role in providing loans and grants for essential infrastructure development, ultimately unlocking and accelerating new housing supply.

This comprehensive approach reflects the government’s commitment to addressing the multifaceted challenges within the housing market and fostering sustainable homeownership opportunities for Australians.

If you’re looking to take the next step and buy your first home, get in touch with us at Rateseeker, we can help guide you through the process and ensure you’re getting the sharpest rates available.

DIY tax? The deadline is getting close.

The Australian Taxation Office (ATO) has issued a timely reminder to taxpayers about the impending October 31 deadline for lodging their tax returns. Filing your taxes on time is crucial to avoid late lodgement penalties. To streamline the process, the ATO suggests two key approaches:

- Lodging Online via myGov: If your tax affairs are relatively straightforward, you can easily complete your tax return online, often in under 30 minutes, through the myGov portal. Most of your information will be pre-filled, so you only need to review and ensure its accuracy. Additionally, you can include any additional income and claim legal deductions to maximise your potential refund.

- Accuracy in Work-Related Expense Claims: The ATO emphasises the importance of accuracy when claiming work-related expenses. It’s essential to avoid the practice of simply copying and pasting previous year’s claims, as each tax year may have unique circumstances that should be accurately reflected in your return.

Rob Thomson, Assistant Commissioner at the ATO, underlines the need for precise claims, stating, “We want people to get their deductions right on the first go and claim what they are entitled to – nothing more, nothing less. We have a series of 40 occupation and industry-specific guides which you should have a look at.”

Thomson also cautions against the temptation to inflate deductions or omit income to boost your tax refund. The ATO utilises advanced data analytics to detect returns that appear suspicious, emphasising the importance of honesty and integrity in tax filings.

So, as the tax deadline approaches, it’s essential to ensure that you file your taxes accurately and on time to avoid penalties and to maintain the integrity of the tax system. Need help? Get in touch with a registered tax agent and get your tax sorted without a penalty.

** General Advice Warning

The information provided on this website is general in nature only and it does not take into account your personal needs or circumstances into consideration. Before acting on any advice, you should consider whether the information is appropriate to your needs and where appropriate, seek professional advice in relation to legal, financial, taxation, mortgage or other advice.