Rateseeker July 2022 Business News Round-up

This month our top stories uncover just how resilient the Australian economy is, along with a tip on legal advice for vendors selling their property. If you’re still getting to your tax, beware of expense claims and income reporting, ATO further warns. And the new wave of staff shortages hitting businesses with a force.

Missed the latest news? Here are the four biggest stories below.

Moody’s lauds Australia’s resilience and financial system

Australia officially has one of the strongest economies in the world.

That’s after Moody’s affirmed Australia’s AAA credit rating, making Australia one of only nine countries in the world to have a AAA credit rating with the three major ratings agencies.

“Australia’s economy continues to demonstrate resilience, underpinned by its scale, diversity and high incomes, as well as its highly flexible labour, product and capital markets, well-regulated financial system and floating exchange rate,”

Moody’s said in its report.

Moody believes these features allowed the economy to recuperate quickly in the aftermath of the covid pandemic, geared with proactive and effective monetary and fiscal policy support which essentially limited any impact on employment.

Moody’s also noted signs that Australia is making “productivity enhancing reforms”, such as “lifting women’s participation in the workforce through support for childcare and gender pay equity, a large-scale infrastructure program focused on improving transport systems, support for innovation and the response to climate change”.

Australia’s economy grew 3.3% in the year to March, according to the latest data from the Australian Bureau of Statistics.

Selling an office building? Here’s why you need legal advice.

Every business knows the importance of ‘buyer beware’ when purchasing a commercial property. But it’s also vital to meet certain legal obligations when you’re the vendor.

Otherwise, the buyer might have grounds to cancel the deal or take legal action, a situation most vendors will want to avoid.

The vendor is required to disclose all material facts to the buyer. This is a subjective standard, which is why it’s important to get expert advice from a commercial property lawyer.

Rules vary from state to state, but you might need to disclose whether the property:

- Has any unregistered easements (e.g. overhead power lines)

- Is contaminated or contains asbestos

- Has structural problems

- Is subject to any authority notices

- Is prone to flooding or is in a bushfire zone

- Contains any mining tenements or graves

You might also need to disclose whether:

- Other parties are allowed to use the land (e.g. telecoms or government agencies)

- The tenant has first right of refusal to buy the property whenever it gets listed for sale

Finally, you might need to disclose the property’s zoning status.

Over-claiming and underreporting income? The ATO is watching.

The Australian Taxation Office has warned small businesses it will focus on three main areas when assessing 2021-22 tax returns.

The first area the ATO plans to examine closely is over-claiming on expenses and claiming deductions for private expenses that are unrelated to business income.

The second area is not telling the ATO about certain income streams, such as revenue from new business ventures or the sharing economy.

Finally, the ATO will hold businesses accountable for their record-keeping, including insufficient or non-existent records that are needed to substantiate claims. So make sure your records are up to date!

ATO assistant commissioner Andrew Watson said if businesses are feeling overwhelmed or are behind with their tax, they should inform the ATO as soon as possible so the two parties can work together to find a solution.

“No matter what your situation is, it’s never too late to ask for help. Tax time is also a great time to discuss ATO debts with your registered tax professional or the ATO – and set up a payment plan if you need one,” he said.

For more information, refer to the ATO’s tax toolkit for small businesses.

If you’re looking to invest or purchase a home and need expert financial advice from experienced brokers, get in touch with Rateseeker today. We can help guide you through the process and secure the sharpest rates.

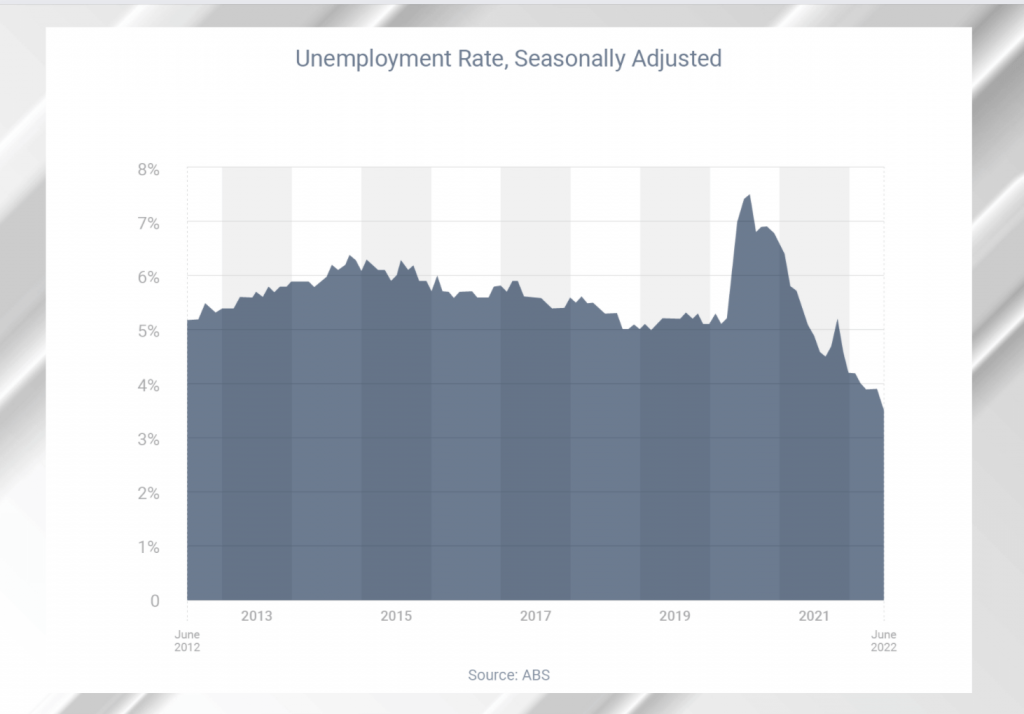

Staff shortages hit businesses as unemployment keeps falling

An Australian Bureau of Statistics survey of about 2,000 businesses in June found 31% were having difficulty finding suitable staff.

The most common reasons given by businesses were:

- Lack of job applicants (79%)

- Applicants not having relevant experience (59%)

- Pay conditions (26%)

- Uncertain economic conditions (24%)

- Job location (24%)

Businesses plan to respond to this staffing challenge in a range of ways, the most common being to:

- Increase wages (30%)

- Increase staff numbers (27%)

- Retrain existing staff (23%)

- Rearrange job roles and responsibilities (21%)

- Increase staff hours (19%)

The Australian Bureau of Statistics’ most recent labour data reveals why employers are finding it so hard to attract and retain staff right now.

Australia’s unemployment rate fell from 3.9% in May to just 3.5% in June, the lowest since 1974.

As a result, there is now just 1.0 unemployed person per job vacancy, compared to 3.1 before the pandemic.

** General Advice Warning

The information provided on this website is general in nature only and it does not take into account your personal needs or circumstances into consideration. Before acting on any advice, you should consider whether the information is appropriate to your needs and where appropriate, seek professional advice in relation to legal, financial, taxation, mortgage or other advice.